The Weekly Bottom Line

Our summary of recent economic events and what to expect in the weeks ahead.

Date Published: August 7, 2026

- Category:

- Canada

Canadian Highlights

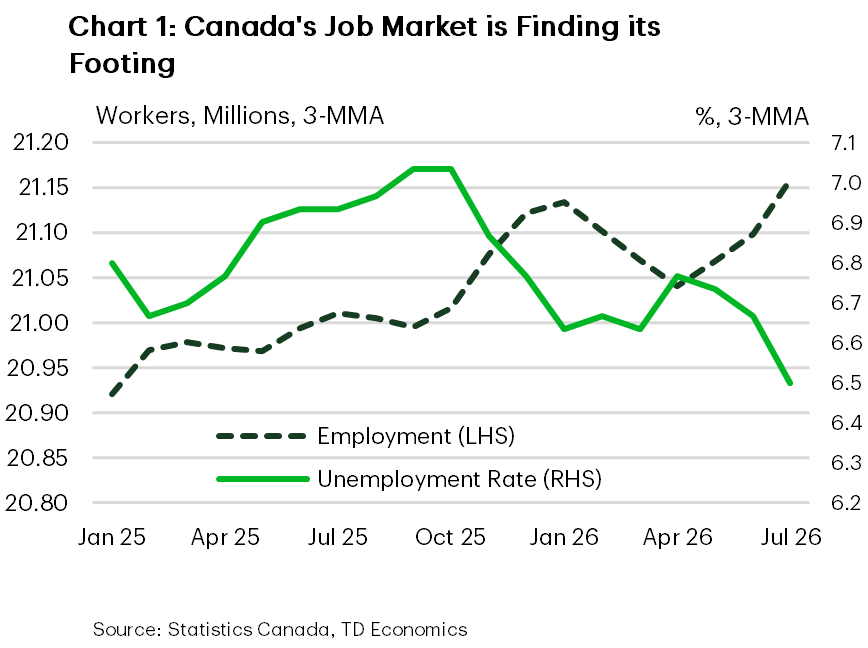

- Canadian employment jumped 75k in July, with broad-based gains across industries, pushing the unemployment rate down to 6.4% and reinforcing signs of economic resilience despite ongoing trade uncertainty.

- Strong labour market and international trade data alongside improving housing activity, suggests the economy got off to a good start to Q3, following what was likely a robust Q2.

- Policymakers are still likely to remain on hold in September given contained inflation and lingering tariff risks.

U.S. Highlights

- Stocks reached fresh all-time highs to start August as oil prices retreated on the back of reports of a potential deal to restart transit through the Strait of Hormuz.

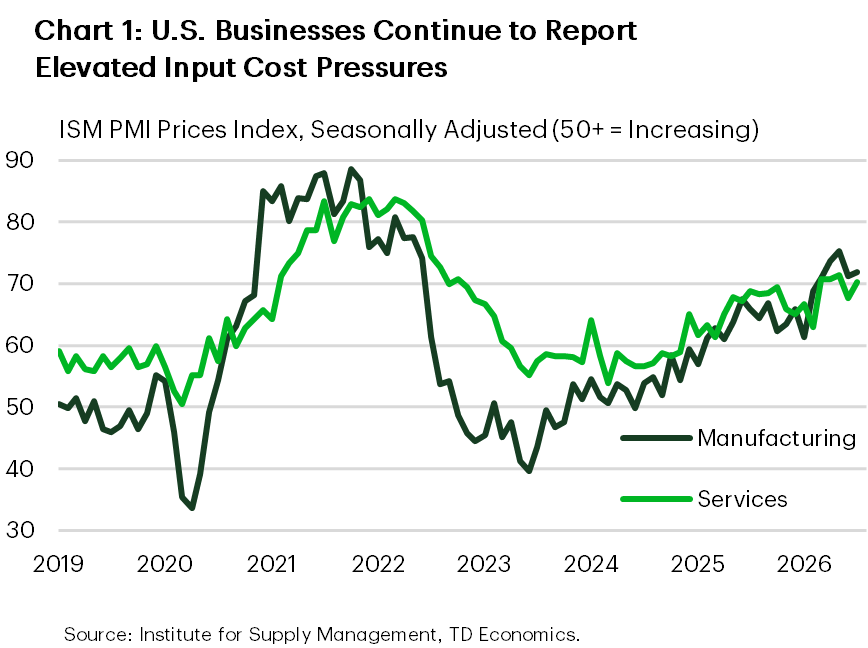

- ISM surveys indicated that manufacturing and services activity continued to expand in July, but elevated input costs point to lingering inflation pressures.

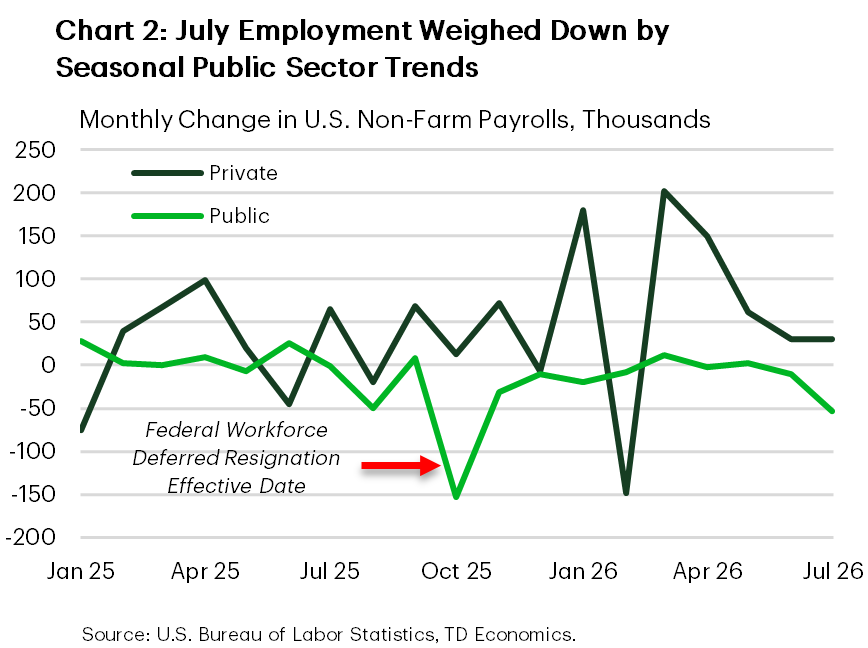

- The labor market lost 23k jobs in July, but this was driven by an outsized decline in local government educational services, likely related to residual seasonality.

Markets were taken for a late-week ride amid a duo of key July jobs reports in Canada and the U.S. For Canadian bond yields, the latter held sway as surprisingly soft hiring in America downwardly pressured interest rates in both countries. The benchmark Canadian 10-year yield sat at around 3.65% in the wake of both reports and remains near its high for the year. The soggy U.S. jobs report was also bad news for the U.S. dollar, which upwardly pressured the loonie, among other major currencies. For its part, oil slid this week on headlines that a U.S./Iran deal could soon be in the offing.

Unlike its U.S. counterpart, the Canadian jobs report was a near picture of wall-to-wall strength (Chart 1). Hiring surged by 75k positions in July, bolstered by the private sector and both full- and part-time positions. What’s more, hiring gains were relatively broad-based across industries. Even the beleaguered manufacturing sector managed to add positions last month, although employment is still down about 2-3% since the start of the U.S./Canada trade conflict. Meanwhile the unemployment rate dipped 0.1 percentage points to 6.4% - its lowest level since 2024 - despite a rise in both the labour force and the participation rate. Hours worked advanced a firm 0.6% month-on-month, offering a solid signal for monthly GDP. One fly in the ointment from a growth perspective was that wage growth decelerated in the month.

Canada’s healthy July employment gains joined preliminary housing data from local boards released this week in painting an optimistic economic growth picture at the start of Q3. Indeed, the housing data suggests that another sales gain took place last month, which would mark the 4th straight increase. These gains may have been sparked by improved affordability in Ontario.

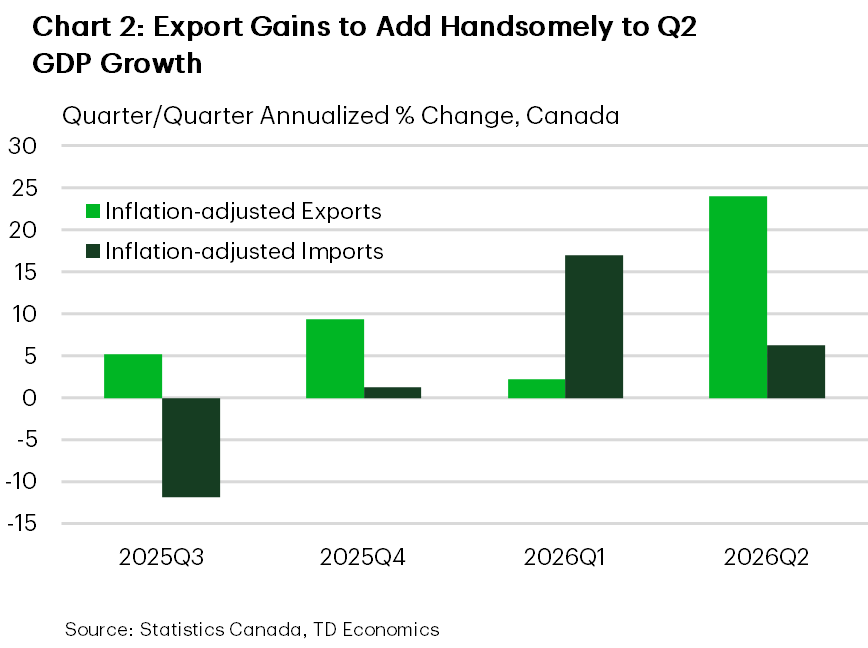

The Bank of Canada’s (BoC) expectation was that economic growth would advance 1.5% annualized in the third quarter, roughly in line with our own. However, this follows what looks to be a very strong outturn in Q2. And this week’s trade report offered fresh evidence of this. Canada’s merchandise trade surplus widened for the fourth straight month in June, supported by a rise in exports that continued the string of sturdy gains over the past few months. Stripping away inflation impacts, export trade volumes rose by 1% month-on-month (m/m) in June, while imports slid 1.5% m/m. For Q2 overall, goods exports were up over 20% annualized, with imports up a lesser 6% (Chart 2), implying a notable contribution to GDP from net trade.

For the BoC, the jobs report was the highlight of the week, Policymakers will no doubt be encouraged by the healthy jobs print, especially considering their recent uncertainty about the durability of Canadian growth after Q2. However, for the upcoming September 2nd meeting, we still see policymakers holding the line on rates. The economy is still facing notable trade-related headwinds (especially the threat of 50% tariffs on 5% of U.S.-bound shipments on the horizon). Also, core inflation remains well-behaved and the jobs market, while improving, isn’t out of the woods just yet.

The first week of August kicked off with stocks hitting fresh all-time highs as oil prices retreated on news of a potential near-term deal to restart transit through the Strait of Hormuz. The deal is reportedly being negotiated between Oman and Iran, but a formal agreement between all parties has yet to be announced as of the time of writing. The S&P 500 rose 3.5% on the week as oil prices fell by 10% and the U.S. 10-year Treasury yield ended the week roughly 10 basis points lower.

Higher oil prices have contributed to stronger nominal manufacturing activity in 2026, while also helping to push the ISM Manufacturing PMI to a four-year high in July. However, there are reasons to view the survey’s strength with some caution. The ISM Prices Paid Index remains near a four-year high (Chart 1), indicating elevated input cost pressures across the manufacturing sector. At the same time, a portion of the improvement in the headline PMI reflects slower supplier deliveries, which the survey interprets as a sign of stronger demand, but can also be consistent with supply-chain constraints. Taken together, the survey continues to point to an expansion in manufacturing activity, though likely at a more moderate pace than implied by the headline reading.

The larger services sector also continued to expand in July according to the ISM report, with new orders and business activity both picking up. However, the report was more concerning for the Federal Reserve, as the employment index slipped back into contraction territory and the prices paid index remained elevated.

This concern was somewhat enhanced by the headline report for July employment, which showed a loss of 23k jobs. However, looking into the details, the decline was entirely driven by an outsized loss in local government educational services. This is likely driven by unaccounted for seasonality coinciding with the summer break for schools. The private sector added 30k jobs during the month, on par with the prior month trend (Chart 2). In addition, the unemployment rate ticked lower to 4.1%, consistent with a labor market that is steady overall.

This concern was somewhat enhanced by the headline report for July employment, which showed a loss of 23k jobs. However, looking into the details, the decline was entirely driven by an outsized loss in local government educational services. This is likely driven by unaccounted for seasonality coinciding with the summer break for schools. The private sector added 30k jobs during the month, on par with the prior month trend (Chart 2). In addition, the unemployment rate ticked lower to 4.1%, consistent with a labor market that is steady overall.

Taken together, the Federal Reserve is faced with an economy that has a stable labor market, but persistent excess inflationary pressures. Among the three voting members of the FOMC that we heard from this week, Minneapolis Fed President Kashkari was the most vocal in support of policy tightening, noting he dissented in favor of a rate hike at the July meeting. Philadelphia Fed President Paulson and Governor Lisa Cook were more measured but noted that persistent inflation could require higher rates. After the employment report, odds of rate hike in September fell from roughly 50/50 to 60% odds for no hike.

With elevated uncertainty over what policy decision will be made by the Federal Reserve at their next meeting, next week’s CPI print for July is likely to be closely monitored. Consensus expectations are for an acceleration in total inflation to 3.5% year-on-year, consistent with the uptick in energy prices during the month. Currently we don’t expect a rate hike in September, but if current inflation trends prove persistent, then policy action may be required.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: