Tracking Bank Stress Contagion

James Orlando, CFA, Director | 416-413-3180

Brett Saldarelli, Economist | 416-542-0072

Date Published: March 28, 2023

- Category:

- US

- Financial Markets

Highlights

- Recent events in the banking sector have put financial conditions in sharp focus. The cost and availability of credit is an important driver of the economic outlook, substituting for tighter monetary policy in slowing economic activity.

- So far, the Federal Reserve’s swift intervention appears to have been successful in quelling volatility in financial markets. Bond yields have fallen sharply as market participants have moved up their expectations for rate cuts. Equity markets have also dropped, though the decline has been relatively tame, with most global stock indexes remaining in positive territory for the year.

- Overall financial conditions have tightened, but less than past experiences and contagion appears limited. Given its importance to the economic outlook we will continue to closely monitor financial conditions for signs of deterioration or improvement, adjusting our views accordingly.

The recent failure of Silicon Valley Bank (SVB), takeover of Credit Suisse, and trouble at other banks has raised concerns around financial stability. Increased financial stress is an important source of downside risk to the economic outlook. Should it persist or worsen, it is likely to translate into meaningfully weaker spending and investment in an economy that was already expected to slow under the weight of high interest rates.

The good news is that across most measures, the current episode looks fairly well contained. Equity markets are still up from levels at the start of the year and volatility has remained well below past crisis-era levels. Credit spreads have widened, but this has been offset by falling bond yields, mitigating the impact on corporate borrowing costs. We are still not out of the woods and a close monitoring of financial conditions and credit availability will remain an important element to the economic outlook.

Table 1: Equity Markets

| Country | 2023 YTD Return | Current Drawdown 2023 | Max Drawdown Over 2022 | Drawdown During Global Pandemic | Drawdown During Global Financial Crisis | Drawdown During European Debt Crisis | Drawdown During Oil Price Shock 2015 |

| US: S&P 500 | 3.6 | -4.8 | -25.4 | -33.9 | -56.8 | -19.4 | -14.2 |

| Canada: S&P/TSX Composite Index | 1.2 | -5.5 | -17.6 | -37.4 | -49.8 | -21.7 | -24.4 |

| UK: FTSE 100 | 0.3 | -6.8 | -11.0 | -34.9 | -47.8 | -18.8 | -22.1 |

| Euro Area: Euro STOXX Price Index | 7.8 | -4.5 | -26.2 | -37.9 | -61.8 | -32.3 | -27.4 |

| Australia: S&P/ASX 300 Index | -1.2 | -8.1 | -15.6 | -36.8 | -54.6 | -22.5 | -19.1 |

| Japan: Nikkei 225 Average | 5.3 | -4.0 | -15.7 | -31.3 | -61.4 | -28.0 | -28.3 |

| China: Shanghai-Shenzhen 300 Index | 3.6 | -4.5 | -29.0 | -16.1 | -72.3 | -41.0 | -46.7 |

| Hong Kong: Hang Seng Index | -1.1 | -13.8 | -41.2 | -25.3 | -65.2 | -34.9 | -35.6 |

| Korea: KOSPI Index | 7.7 | -3.0 | -27.9 | -35.7 | -54.5 | -25.9 | -15.8 |

| Taiwan Stock Market | 12.0 | -0.5 | -31.6 | -28.7 | -58.3 | -27.5 | -25.7 |

| Singapore: Straits Times Index | -0.4 | -4.6 | -13.8 | -31.9 | -62.4 | -23.7 | -28.5 |

| India: Nifty 50 Index | -6.2 | -6.8 | -16.5 | -38.4 | -59.9 | -28.0 | -22.5 |

Equity Markets

- The equity market decline has been muted relative to historical episodes of financial market stress, including the Global Financial Crisis (GFC), and more recently, the Russia-Ukraine conflict (Table 1). While the S&P 500 has fallen 5% from its peak in early February, it remains in the black for the year, registering a 4% gain. That said, the equity market decline has primarily been concentrated in the financial sector, with the S&P 500 Regional Bank Index falling over 40% from its 2023 peak.

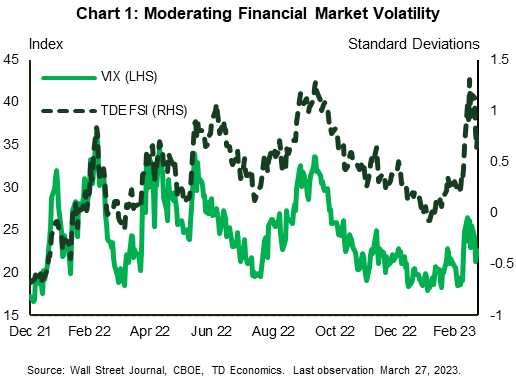

- The S&P 500 Volatility Index (VIX) reflects the lack of contagion in the broader market. Its peak intraday high of 29.6 was lower than past stress periods, and it has since fallen to a current level of 21. This is echoed in our Financial Stress Index, which has fallen notably over the past week and is hovering just above what we consider to be normal levels (Chart 1).

- With the takeover of Credit Suisse, the story in Europe parallels that of North America. The Euro STOXX Index has gained 7.8% for the year despite falling 4.5% from its 2023 peak. Other gauges of volatility in the Euro Area, including the Euro STOXX 50 Volatility Index and the European Central Banks Composite Indicator of Systemic Stress, have increased but remain well below their 2022 highs and the levels reached during the European Sovereign Debt Crisis.

Treasury Market

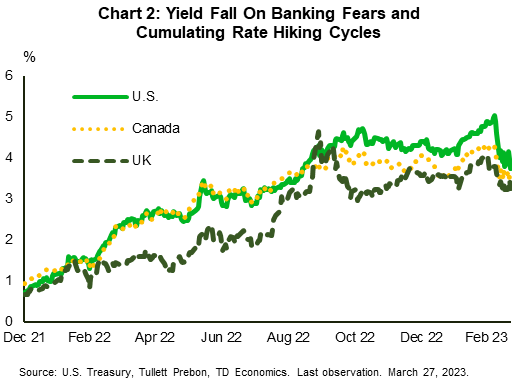

- While volatility in equity markets has moderated, the same cannot be said for government bond markets. In the U.S., uncertainty surrounding the banking sector has had investors betting that the Federal Reserve is nearing the end of its rate hiking cycle. This is reflected in the 2-year Treasury yield falling over 100 basis points (bps) since reaching a 15-year high in early-March (Chart 2).

- Real yields have also declined as inflation expectations (2-year TIPS) have dropped less than nominal yields – by 76 bps from their 2023 peak. Declining yields have already started to filter through to consumer borrowing rates, with the U.S. 30-year conventional mortgage rate falling close to 70 bps from its November high. Even in Germany and the UK, where both the ECB and BoE need to keep raising their policy rates, government yields have followed U.S. Treasuries lower, with the 2-year yields in both countries losing more than 80 bps.

Credit Spreads

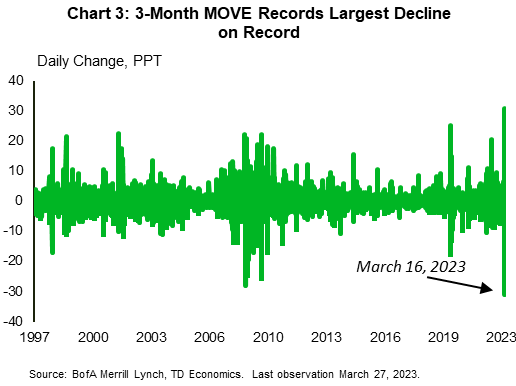

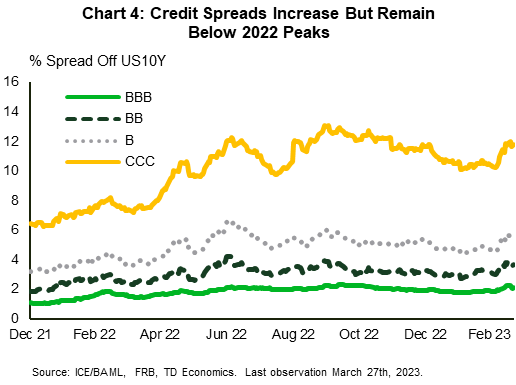

- The turmoil in the banking sector has also been evident in corporate credit markets. The CCC spread has increased by 158 bps since March 6th, while the single-B spread has risen by 100 bps. In the investment grade space, increases have been more benign with the BBB spread rising by a modest 22 bps. While spreads have increased, the total cost of borrowing has dropped for many corporate borrowers as a result of falling bond yields (Chart 3). This should offset some of the impact from tighter credit conditions coming down the pipe.

- Credit conditions have also tightened across the pond as European credit default swaps (CDS) have increased above their average over the past decade. That said, CDS remain below their 2022 highs, the levels experienced during the European Sovereign Debt Crisis, and the Global Pandemic.

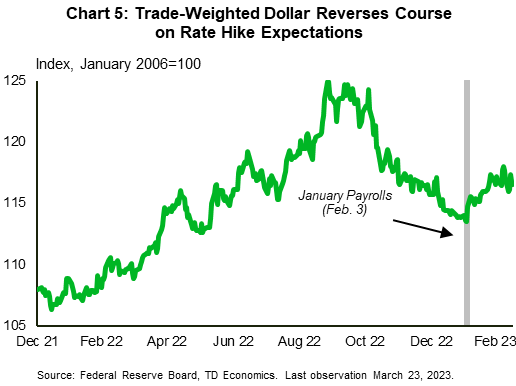

Foreign Exchange

- The trade weighted U.S. dollar captured headlines over 2022, appreciating 11% through October before falling close to 8% as financial markets recalibrated their view of the path of the fed funds rate (Chart 4). While the greenback has regained some of its lost ground, the story differs across currencies. The pound and euro have appreciated by 1.6% and 0.9%, respectively, while commodity currencies including the Canadian and Australian dollars have depreciated by 0.8% and 2.4%, as oil prices have fallen 14% since the beginning of

the year.

Short-Term Liquidity and Bank Funding

- With increased uncertainty in the banking sector, interbank lending rates should capture heightened risk, just as they did during the GFC and the pandemic. Fortunately, the 3-month LIBOR OIS spread has remained benign, reaching a high of 27 bps compared to 365 bps experienced during the GFC and 140 bps at the onset of the pandemic (Chart 5). These low rates reflect the confidence that banks have with one another, despite recent failures.

Final Take

The stress stemming from the banking system has raised fears of financial market contagion. While we have seen worries shift to new banks in both the U.S. and Europe, and spreads of the lowest rated credit have widened, the financial market reaction does not reflect a systemic loss of confidence. So far, the biggest moves have been contained to a few idiosyncratic banks, with spillovers in the regional bank index. In terms of broad market impact, the overall equity market is still in positive territory over 2023, while credit and interbank spreads are not priced for further fallout.

In a macro sense, the biggest impact has been in the bond market, where the higher for longer Federal Reserve policy narrative has been upended. Markets are now firmly priced for over 75 bps in rate cuts over the next year, causing Treasury yields to fall precipitously. While no one knows what will happen next, we will be closely monitoring the spread of the current stress, looking for signs of improvement or deterioration as key to the evolution of the economic outlook.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: