U.S. Tariffs in Transition: An Uncertain Evolution

Andrew Foran, Economist | 416-350-8927

Date Published: June 1, 2026

- Category:

- U.S. Trade

- Government Finance & Policy

Highlights

- U.S. trade policy uncertainty has intensified in 2026 after the Supreme Court struck down IEEPA tariffs in February and the administration’s temporary alternative under Section 122 has been subject to judicial injunctions.

- The next phase of U.S. tariff policy is likely to rely more heavily on Section 301 country investigations and Section 232 product actions, leaving the scale, coverage, and durability of future tariffs uncertain.

- Even if average U.S. tariff rates do not rise materially from current levels, persistent policy uncertainty is likely to keep businesses cautious and weigh on trade and growth through 2026.

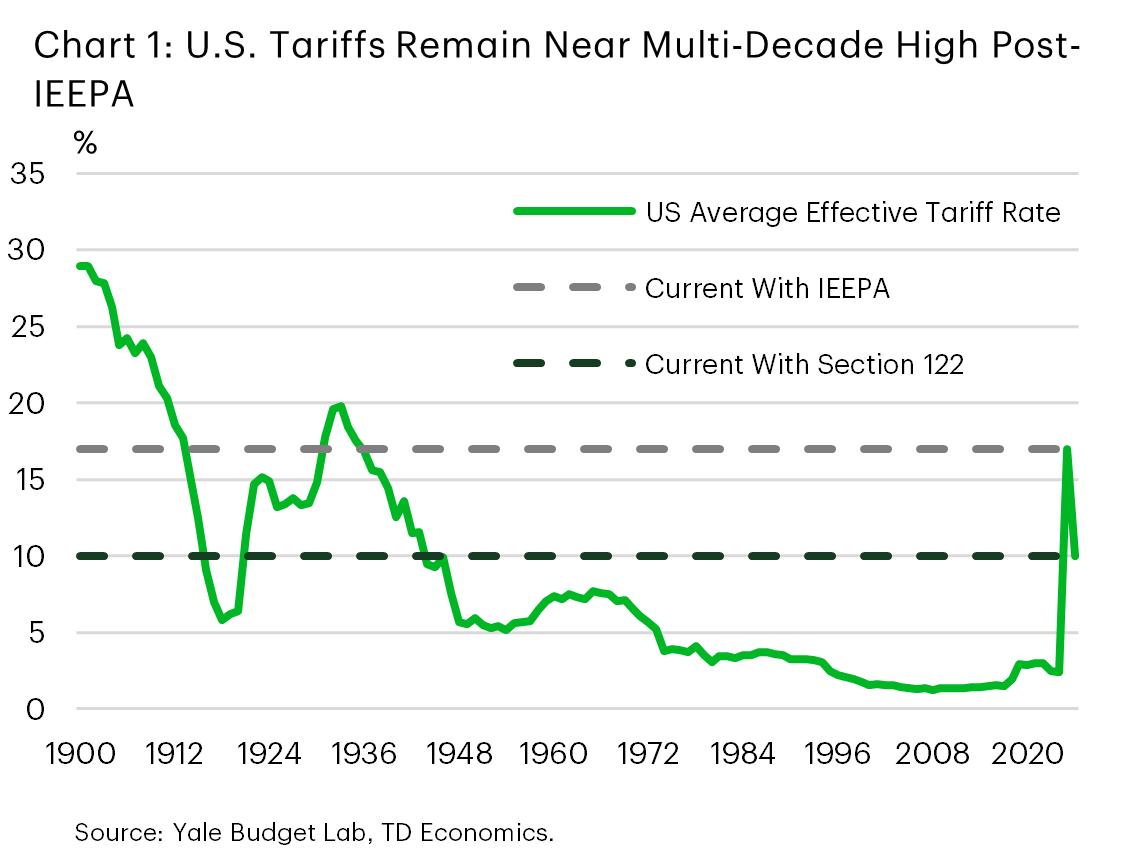

U.S. trade policy uncertainty has faded to the background in recent months amid the conflict in the Middle East but could easily reemerge as a central macroeconomic issue over the coming months. The latest development on tariffs occurred following a U.S. Supreme Court ruling that invalidated tariffs imposed under the International Emergency Economic Powers Act (IEEPA). In response, the administration quickly implemented a temporary 10 percent global tariff under Section 122 of the Trade Act of 1974, partially offsetting the immediate loss of IEEPA‑based measures. However, this alternative was also ruled against by the U.S. Court of International Trade in early May, leaving its future uncertain amid appeal proceedings. This is occurring against a backdrop of notably elevated tariff levels relative to recent history, with the effective U.S. tariff rate rising sharply from roughly 2 percent at the start of 2025 to close to 10 percent by early 2026, and remaining well above pre‑2025 norms (Chart 1).

Looking ahead, the administration has instead launched a broad set of Section 301 investigations covering more than 60 trading partners. These measures are generally regarded as establishing a foundation for a more sustainable alternative to the previous IEEPA tariff framework, although the scope and duration of any subsequent tariff system continue to be uncertain. Trade policy uncertainty is therefore likely to persist through at least the remainder of 2026, amid open questions surrounding the durability of reciprocal tariff arrangements, the scope for additional tariffs to be introduced with limited notice, the upcoming USMCA review, and the expiration of the U.S.–China trade détente in November. Taken together, these uncertainties are expected to weigh on trade decisions and economic growth through this year, even if average tariff levels do not rise materially.

Where Tariffs Stand Today

One year after the implementation of the first tariffs under the International Emergency Economic Powers Act (IEEPA), the Supreme Court ruled that IEEPA did not confer tariff authority onto the executive branch. As a result, all country-specific tariffs were eliminated including fentanyl tariffs against Canada, Mexico, and China, and the reciprocal tariffs against nearly all U.S. trading partners. These expansive tariff policies were also highly flexible, with multiple adjustments made by the administration after their initial implementation. With IEEPA no longer permitted as a tariff authority, the administration has turned to less flexible, but more conventional authorities.

Technically, Section 122 is not a conventional tariff authority, but it is notably less flexible than the administration’s use of IEEPA. The statute allows for tariffs of up to 15% for 150 days to address large and persistent balance of payments deficits and/or defend the value of the dollar. The administration’s imposition of a 10% global Section 122 tariff on February 24th was the first time the statute was used. However, a decision by the U.S. Court of International Trade on May 7th found that Section 122 did not allow the administration to impose tariffs for the reasons it sought to, notably to decrease the U.S. trade deficit.

While the court did rule against the tariffs, the injunction it granted was not universal and only applied to some of the parties involved in the lawsuit. This means the Section 122 tariffs remain in effect for now but are likely to be subject to further legal challenges. Given the lack of precedent surrounding the use of Section 122 tariffs, it is possible the case may be appealed up to the level of the Supreme Court. This would mean the actual impacts of a judicial ruling would likely occur after the 10% Section 122 tariff has expired. However, if a final judicial decision does not favor the administration’s arguments, then refunds may be ordered retroactively on the tariff revenues collected, which would be in addition to the roughly $127 billion in refunds already being provided under the since voided IEEPA tariffs.

Beyond the temporary near-term, the question remaining is what tariffs will follow the Section 122 tariffs after they expire in late July? The administration answered this question in mid-March, when it announced that it would be launching two Section 301 tariff investigations into more than 60 trading partners. These tariffs are levied against countries engaging in anti-competitive trading practices and have been used at length against China, like during the 2018 trade spat. The Biden administration left these tariffs in place and added additional tariffs on Chinese electric vehicles, semiconductors, solar panel cells, and other products. Now the Trump administration is looking to expand the use of Section 301 tariffs globally.

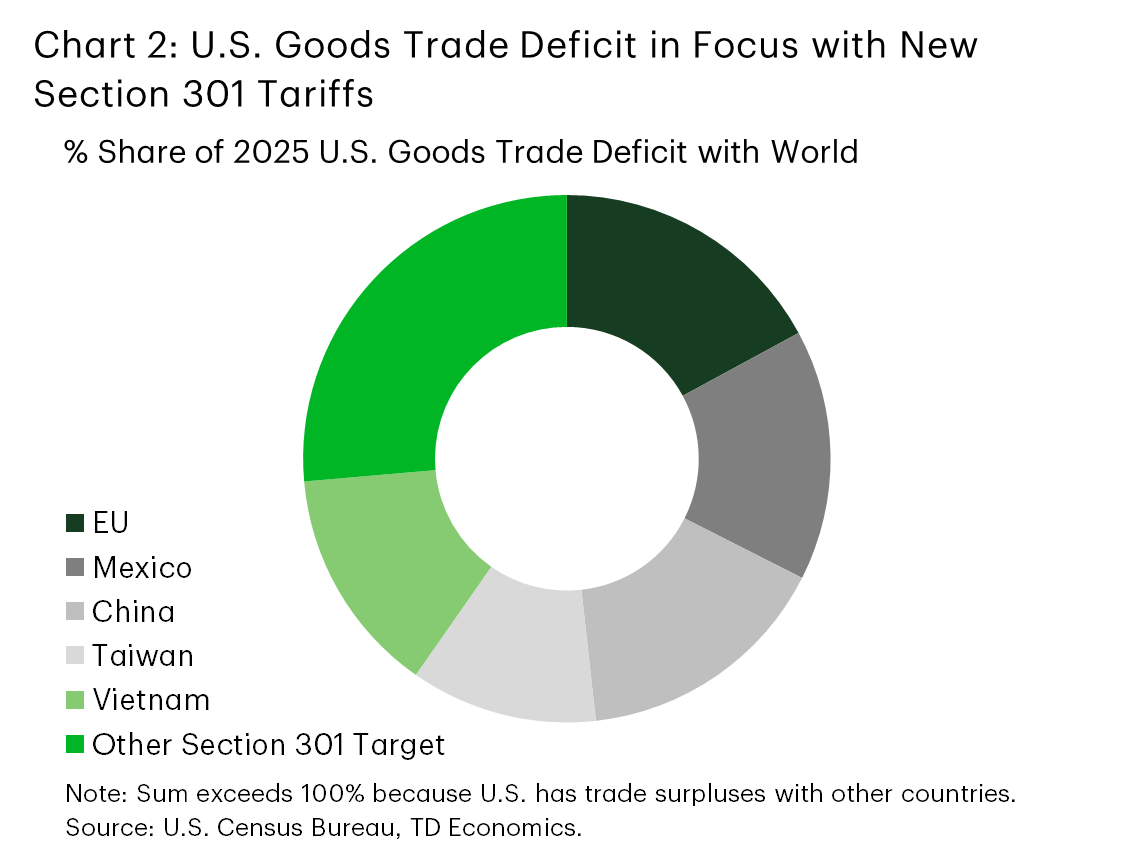

The first tariff investigation launched is related to allegations by the U.S. that certain countries are maintaining structural excess manufacturing production capacity. The administration defines structural excess capacity as “underutilized industrial production capacity that is sustained through governmental interventions or policies incentivising companies to maintain or grow their unused capacity inefficiently.” The nations targeted include China, the E.U., Singapore, Switzerland, Norway, Indonesia, Malaysia, Cambodia, Thailand, South Korea, Vietnam, Taiwan, Bangladesh, Mexico, Japan, and India. In the Federal Register notice for the tariff investigation, the Office of the U.S. Trade Representative (USTR) argued that trade surpluses were evidence of excess production capacity, meaning that these tariffs are likely to serve as the successor to the reciprocal tariffs imposed under IEEPA. This is likewise evidenced by the fact that the countries targeted account for the lion’s share of the U.S. goods trade deficit with the world (Chart 2).

The second Section 301 tariff investigation is related to allegations that other nations are failing to “impose and effectively enforce a prohibition on the importation of goods produced using forced labor”. This investigation is far broader in terms of the number of nations targeted, with 60 countries under investigation. Importantly, the Office of the USTR stated that nations such as Canada, Mexico, and the E.U. have adopted measures to prevent trade in goods produced using forced labor, but also stated that “no countries have adopted and effectively enforced a forced labor import prohibition to date”. This investigation draws parallels to the fentanyl & unlawful migration tariffs imposed under IEEPA against China, Mexico, and Canada, where trade measures were used to curtail alleged illicit activity. Similarly, the use of qualitative statements such as “effectively enforced” suggests that these tariffs could also be imposed on a discretionary basis. Importantly, Section 301 tariffs can be modified after they are imposed, meaning that in many ways, Section 301 could functionally serve as a replacement to the administration’s IEEPA tariffs as long as the action taken is tied to the trade grievance cited in the original Section 301 investigation.

Historically, Section 301 investigations have taken 12-18 months to complete, as they require an in-depth review of the issue and public consultations, but they can take as little as half a year if the investigation is prioritized. This seems to be the goal of the USTR, with public hearings completed in early May, as the administration has indicated its goal to have these tariffs in place by the time the Section 122 tariffs expire in late July. Still, these investigations are expansive in scope, which could create challenges for the USTR to finalize the implementation by that time.

In addition to the Section 301 investigations, the administration is also still reviewing further product specific Section 232 tariffs. These tariffs remain in effect on steel, aluminum, lumber, light and heavy automobiles & parts, and semiconductors. Tariff rates on these products have typically been set to 25%, though the primary metal tariffs (steel, aluminum, and copper) are higher at 50%. Patented pharmaceutical products are also expected to face a baseline tariff of 100% starting on July 31st, however these tariffs have numerous country- and firm-level adjustments which will meaningfully lower the actual tariff that comes into effect at that time. Other products being reviewed for possible Section 232 tariffs include commercial aircraft & jet engines, polysilicon (used in solar panels and semiconductors), unmanned aircraft systems, wind turbines, medical equipment, and robotics & industrial machinery. Tariffs on these products could be announced at any time, as could additional Section 232 tariff investigations on other products.

The complex web of country and product level tariffs imposed by the U.S. over the past year has been subject to considerable modification, both through executive amendments and judicial rulings. This has complicated the ability of households and businesses to adapt to the tariffs, as considerable uncertainty remains with respect to their magnitude, composition, and durability. The tariff authorities that the administration is looking to use moving forward, namely Section 232 and Section 301, have stronger judicial precedents associated with their use, although the administration is using them in an expansive manner which could still draw legal reviews. In addition, the executive branch will also maintain the ability to modify tariffs according to its trade policy goals. Taken together, this means that U.S. trade policy is likely to remain subject to higher uncertainty over the coming quarters.

Impacts of Tariffs on U.S. Trade

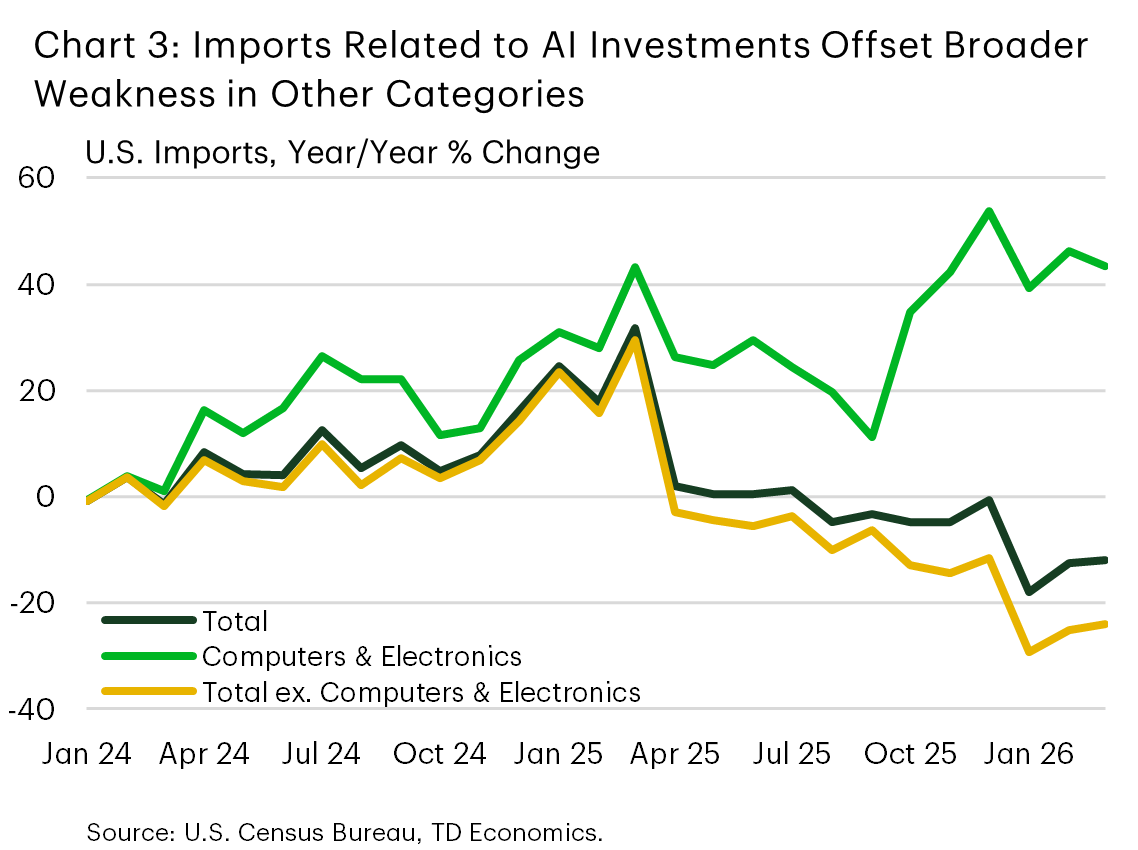

Imports to the U.S. increased by 4.6% last year, primarily stemming from the surge in imports which occurred in the first half of the year. After this initial surge, imports were held roughly constant relative to the prior year in which the new tariff policies were not in effect. However, focusing on the aggregate trends in imports obscures the underlying picture. Notably, imports of computers & electronic products increased by 30% last year, doubling the growth recorded in the year prior amid the boom in artificial intelligence investments (Chart 3). As of March 2026, the computers & electronic products category accounts for just under a third of U.S. imports – roughly doubling its share over the past two years. If you exclude computers & electronics, imports fell consistently through 2025 and ended the year down nearly 15% year-on-year. Coming into 2026, the year-on-year trends become distorted by comparisons to the early 2025 surge.

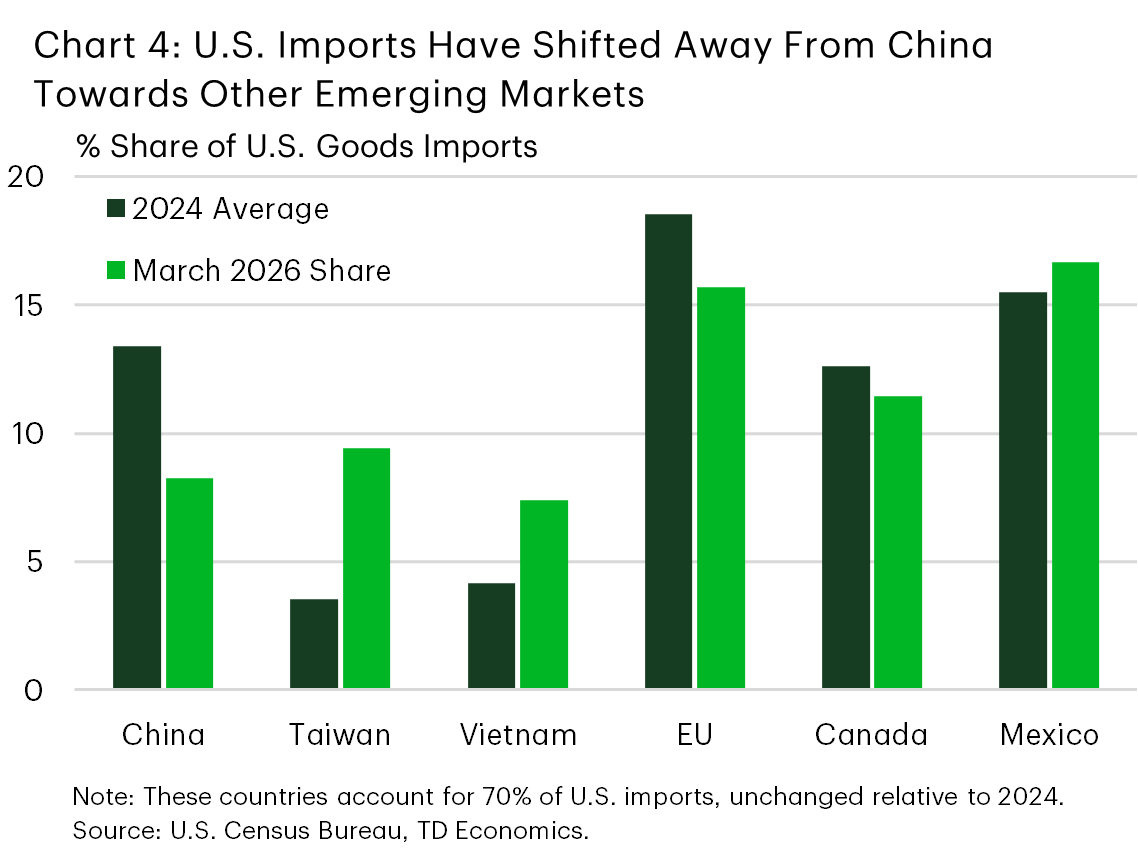

When looking at the country shares of U.S. imports, the most notable development over the past year has been the decrease in the share accounted for by China. While this has some historical precedent, with earlier roots in the initial post-pandemic period, China’s share of U.S. imports has been roughly halved relative to 2024 (Chart 4). Note that for most of last year, the U.S. maintained a threat of imposing triple digit tariffs on China until a 1-year truce was reached in November. Much of the decline in China’s share has been absorbed by southeast Asian countries, such as Vietnam, in addition to Mexico, and Taiwan, with the latter’s gain highly correlated with the trends in computer & electronics imports. Other major trading partners such as the E.U. and Canada have also seen share declines of several percentage points.

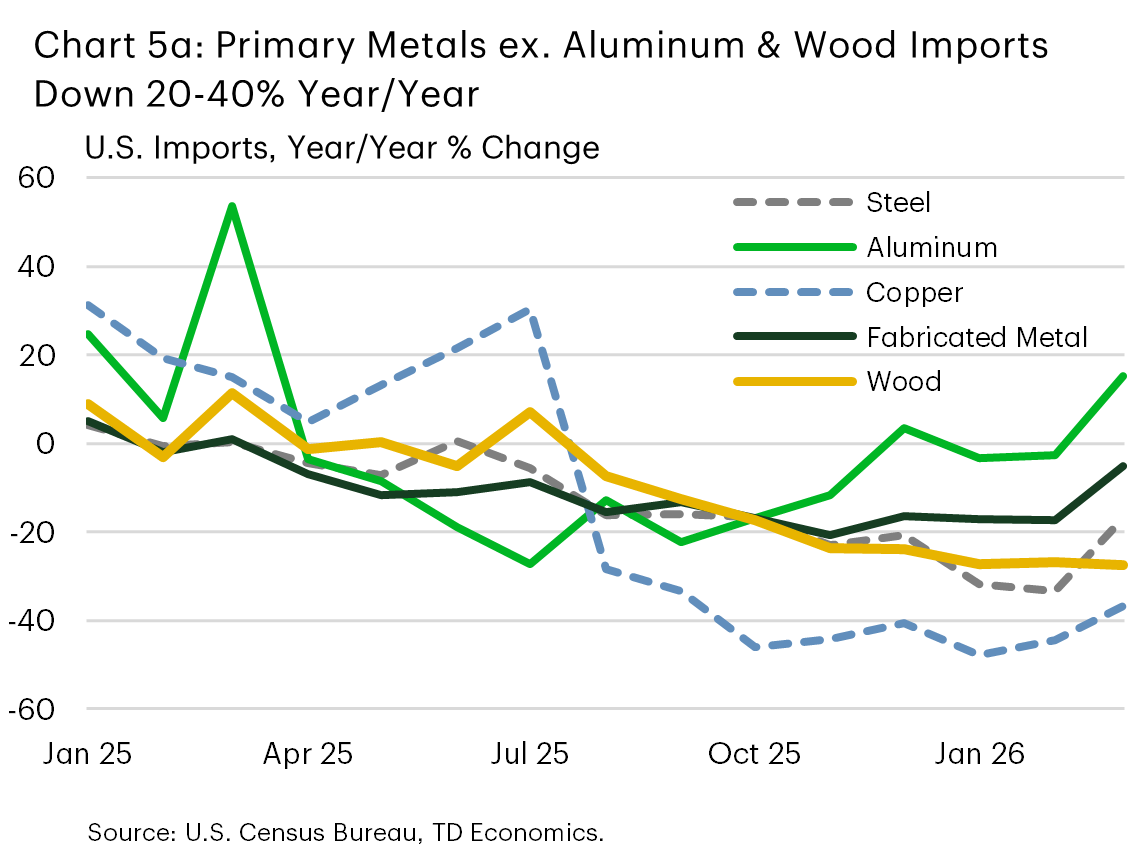

Beyond the impact of AI investments, product level developments were also heavily influenced by the implementation of Section 232 tariffs, though the exact impact was dependent on the timing and included exemptions provided for each product targeted. In the case of steel, aluminum, and copper, which faced a 25% tariff initially followed by a 50% tariff in June 2025, each faced a different trend over the past year (Chart 5a). Steel imports fell gradually through the year, now down roughly 20% year-on-year. Copper imports also fell notably, but faced a sharper decline after the 50% tariff came into effect and remain down 40% year-on-year. Aluminum was an outlier, with imports roughly flat year-on-year through the second half of last year. This could suggest that aluminum importers were less sensitive to the impact of tariffs and/or had a lack of readily available domestic alternatives. The Section 232 tariffs on lumber products resulted in a trend like that of steel.

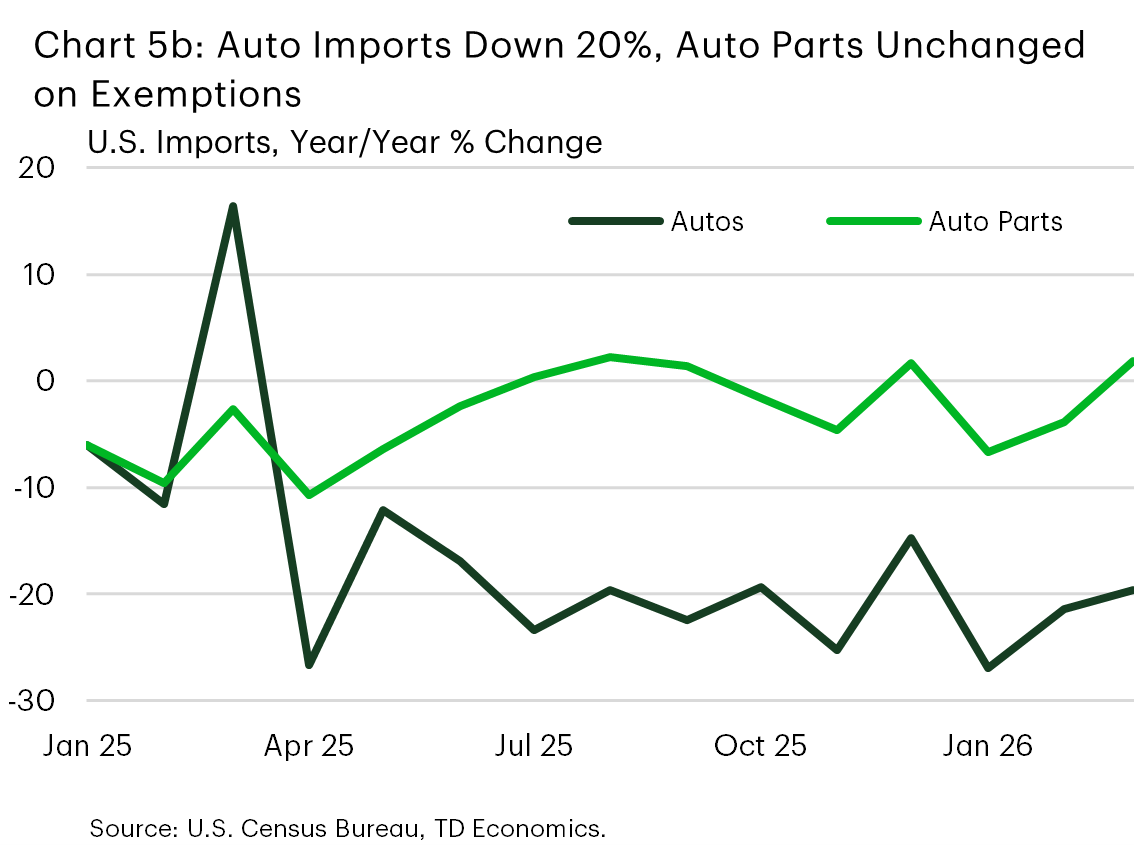

The impact on the automotive sector was similarly interesting. Imports of automobiles surged ahead of the implementation of tariffs, before falling sharply and remaining down 20% year-on-year (Chart 5b). Automotive parts faced a different trend, with imports steady over the past year. This was largely attributed to the exemptions provided for this tariff, with roughly 60% of imports covered by USMCA exemptions. The bulk of the remaining share of imports continues to be covered by offsets provided to automakers allowing for up to 15% of the content of a vehicle to be imported content. This offset was previously scheduled to be halved in 2026 and then fully eliminated in 2027, but the administration extended it through 2030 last October.

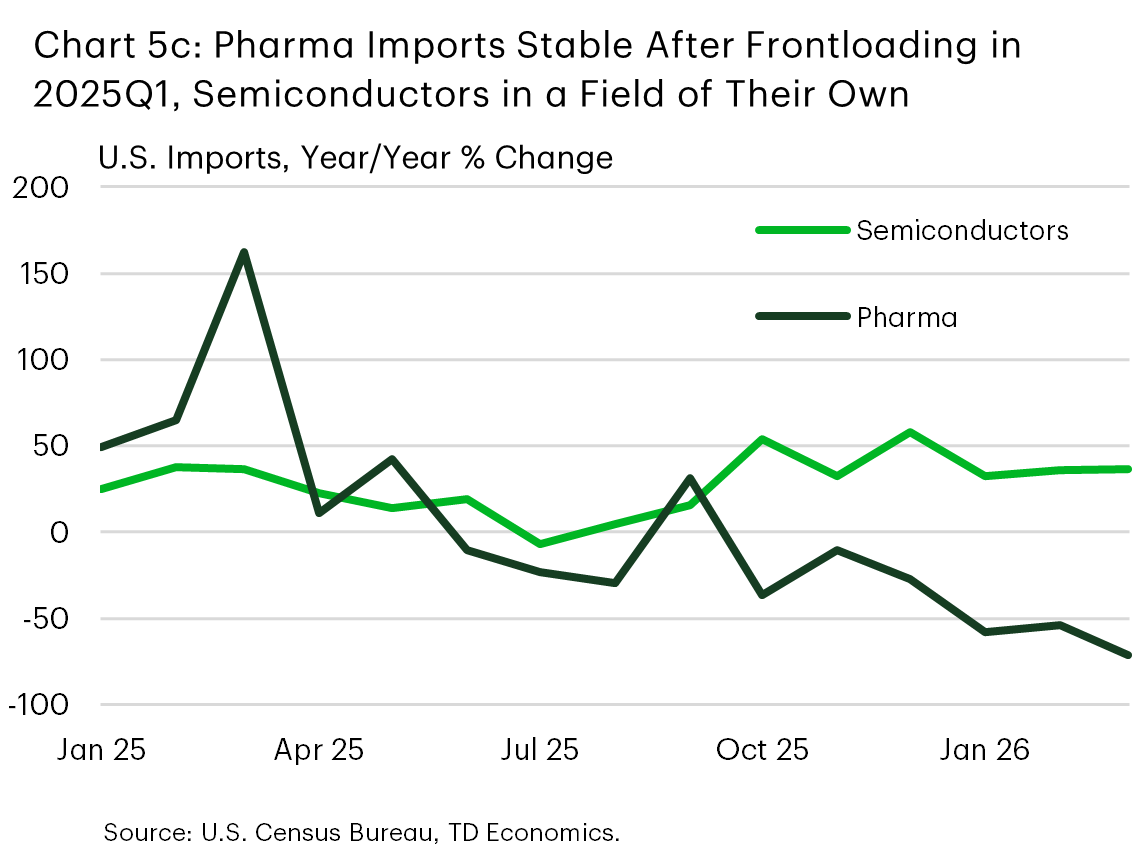

Lastly we have the most recent inclusions to the Section 232 tariffs, semiconductors and pharmaceuticals. Several caveats need to be raised here though. First, the tariffs imposed on semiconductors are heavily exempted, meaning they are unlikely to alter the strong momentum imports of this product are currently incurring from AI investment activity. Second, the pharmaceutical tariffs do not come into effect until July, but they have been actively discussed by the administration for over a year, with threats of 100% tariffs floated periodically. This was sufficient to create a surge in imports in the first half of 2025, followed by a sharp reversal (Chart 5c).

The impact of tariffs on U.S. trade has been nuanced, with imports shifting away from China while Section 232 tariffs weighed on the imports of targeted products. Moving forward, developments between the U.S. and China will continue to be watched closely, though importers have already diversified much of their exposure away from the country. The implementation of Section 301 tariffs will also be monitored over the second half of the year, as new country-specific tariffs are provided, which could lead to import substitution if they are imposed at meaningfully different levels by country.

Bottom Line

U.S. trade policy continues to have a material influence on the economy more than one year on from Liberation Day. Various modifications to tariffs by both the judicial and executive branches has heightened uncertainty for consumers and businesses which in turn has weighed on the economy. In 2026, notable trade developments are expected to sustain these trends, including the USMCA review scheduled for early July, the durability of Section 122 tariffs up to their expiration on July 24th, the implementation of Section 301 tariffs thereafter, and the expiration of the 1-year truce between the U.S. and China in November. U.S. trade policy is expected to stabilize later this year, although the possibility for structurally higher trade policy uncertainty moving forward can not be fully discounted at this time.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: