Revisiting Adjustable-Rate Mortgages (ARMs): A Potential Leg Up in Today’s High-Rate U.S. Housing Market

Admir Kolaj, Economist | 416-944-6318

Date Published: April 14, 2026

- Category:

- U.S.

- Real Estate

Highlights

- Policy measures may eventually lend a hand to housing affordability, but buyers should also weigh financing choices carefully as these can provide more immediate relief. For the right borrower, adjustable-rate mortgages (ARMs) can offer a practical way to lower monthly payments in today’s elevated rate environment.

- ARMs carry a muddy reputation, but today’s ARMs are structurally more robust than their pre-housing-crash predecessors, featuring tighter underwriting standards, generally longer initial fixed rate periods and explicit interest rate caps.

- The ARM discount peaked in late 2022 but remains meaningful even today. ARMs – including those with longer fixed rate periods – continue to provide notable savings over the fixed-rate portion versus the traditional 30-year fixed, offering a viable affordability lever.

- Most borrowers still opt for a 30-year fixed mortgage, but the typical loan is held for far less time (about 7–10 years). In this vein, ARMs with longer fixed-term portions – such as the 7/6 ARM – may better match borrower behavior and offer an attractive risk-reward trade-off.

After easing earlier in the year, mortgage rates have climbed again recently alongside a rapid rise in long-term bond yields. The typical 30-year mortgage rate is up about 40 basis points since late February to 6.4%. For a buyer purchasing the typical home, that increase adds roughly $90 to the monthly mortgage payment, undoing part of the progress in housing affordability made over the past year.

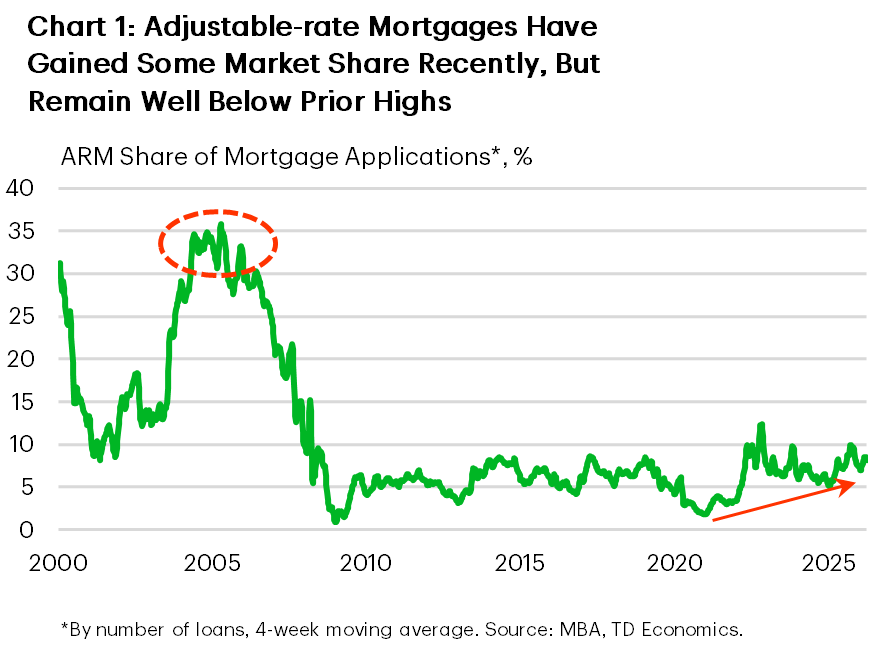

Policymakers continue to explore ways to support housing affordability; we covered many of these initiatives in our report here: Assessing the Impact of U.S. Housing Affordability Proposals. But, looking beyond what may eventually come from policy changes, a practical source of relief – often overlooked due to its troubled history – may be an adjustable-rate mortgage (ARM). Long blamed for being at the root of the last housing crash, ARMs retain a stigma that no longer fully reflects how these products are structured or regulated today (Chart 1). These mortgage products deserve a second look given the potential to offer the benefit of a meaningful rate discount combined with palatable risk for a subset of buyers.

Understanding Adjustable-Rate Mortgages (ARMs) and Recent Changes

Adjustable-rate mortgages (ARMs) are typically described using two numbers (e.g., 5/1 or 7/1 ARM). The first number indicates how long in years the rate is fixed at origination, while the second number indicates how often the rate resets thereafter. For example, a 5/1 ARM has a fixed rate for five years, after which the interest rate adjusts once per year based on a benchmark rate plus a fixed margin.

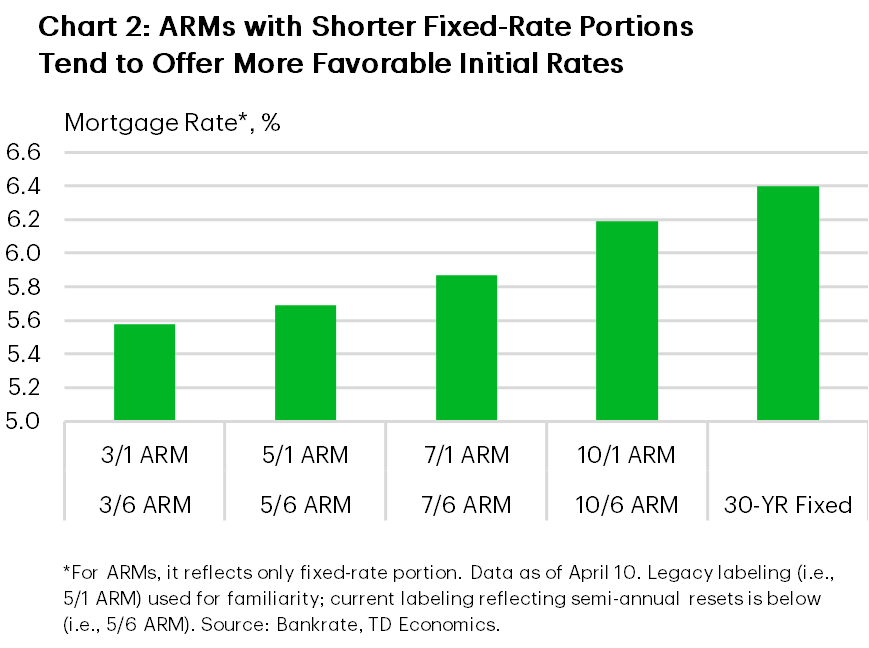

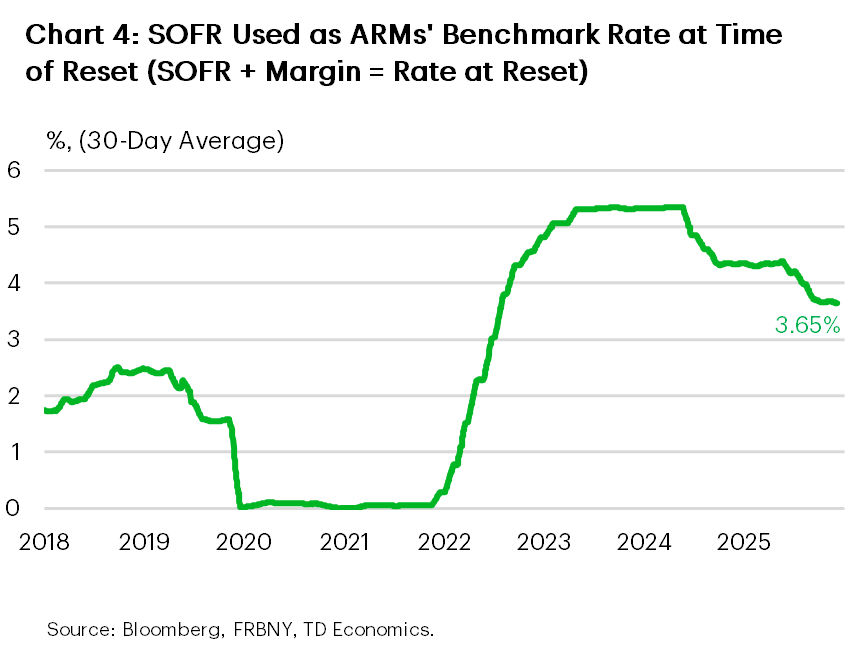

Historically, ARMs were commonly indexed to LIBOR (London Interbank Offered Rate) and reset annually. Following the global transition away from LIBOR in 2023, U.S. mortgage markets have largely shifted to using SOFR (the Secured Overnight Financing Rate).1 Most adjustable-rate mortgages now are SOFR-based hybrid ARMs, which differ primarily in their reset frequency. Rather than annual adjustments, most newly originated ARMs now reset semiannually following the initial fixed-rate period. As a result, legacy terms such as 5/1 or 7/1 ARM are increasingly being replaced by products labeled 5/6 and 7/6 ARM, where the second number reflects a six-month (semiannual) reset schedule. Note, however, that despite the shift to semi-annual resets, many consumer-facing platforms continue to use legacy labels like “5/1” or “7/1” for familiarity, even when the underlying products now follow a 5/6 or 7/6 structure (Chart 2).

A Discount Hiding in Plain Sight

Adjustable-rate mortgages typically offer lower initial interest rates than a traditional 30-year fixed mortgage. The lower initial payments can improve affordability at the margin, allowing some households to either reduce monthly costs, enter the market sooner, or qualify for a larger loan and purchase a higher quality home than would otherwise be possible. This is particularly relevant in expensive coastal and urban markets, where the absolute dollar savings from a lower starting rate can be substantial.

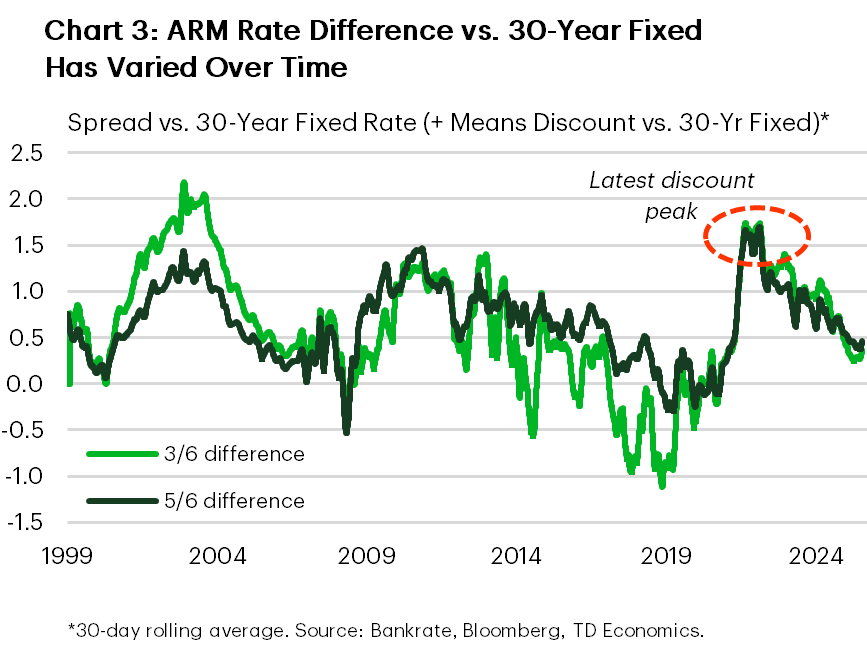

In general, shorter fixed-term ARMs (e.g., 3/6) offer larger discounts, while longer fixed-term options (e.g., 7/6) tend to offer smaller – though still meaningful – discounts (Chart 2). That said, the rate benefit of choosing ARMs has varied over time. The ARM discount improved substantially in 2022 as the Fed began to raise rates rapidly, peaking later that year, and generally trending lower since then. Even so, it has remained meaningful (Chart 3).

Once bitten, twice shy: Why ARMs Carry a Bad Reputation and How Today’s ARMs Are Somewhat Different

Reluctance toward adjustable-rate mortgages is understandable given their role in the mid-2000s housing boom and bust. Many pre-crisis ARMs featured short teaser rates, frequent resets, and weak underwriting, leaving borrowers exposed to sharp payment increases and contributing to delinquencies and foreclosures.

However, today’s ARMs are somewhat different. Most come with substantially longer initial fixed-rate periods, less frequent adjustments, and explicit caps that limit both periodic and lifetime rate increases. Post-crisis rules, including Ability-to-Repay requirements under Dodd-Frank Act – have further tightened underwriting by requiring lenders to assess affordability at higher potential reset rates.2 In this vein, it is worth noting that despite generally offering a lower rate, ARMs may be marginally harder to qualify for than the typical 30-year fixed as lenders assess the borrower’s ability to make higher payments on future rate adjustments. Additionally, minimum down payment requirements are generally slightly higher at about 5% for ARMs vs. 3% for 30-year fixed mortgages.

The post-housing crash regulation effectively outlawed many of the most problematic types of loans, such as those with low teaser rates or those that lacked income, employment, or asset verification. Modern ARMs function less like speculative instruments and more like medium-term fixed-rate mortgages with built-in flexibility, and their usage today is concentrated among higher-income, higher-credit-quality borrowers.

Concerns around prepayment penalties have also diminished. These fees are now uncommon and tightly regulated, limited to the first three years of a loan and prohibited altogether for government-insured mortgages. For most conventional borrowers, the option to refinance remains intact – an important consideration for ARM users who expect to exit the loan before the initial fixed period expires – though it typically requires requalification.

Beyond lowering initial payments, ARMs can also act as a conditional stabilizer over the interest rate cycle. When short-term rates decline, borrowers benefit automatically after the fixed period expires, without needing to refinance – supporting household cash flow during economic slowdowns. When rates rise, however, ARMs do expose borrowers to higher payments, underscoring the importance of interest rate caps, borrower income buffers, and aligning the fixed-rate period with expected loan tenure.

Interest Rate Caps: A Structural Backstop

A larger initial rate discount makes ARMs more attractive versus a 30-year fixed, but borrowers assume rate risk once the fixed period ends. In practice, many borrowers refinance or exit the loan around that time.

At reset, ARM rates typically move to a combination of the prevailing SOFR rate plus a margin set by the lender (often 2.25%-2.75%, generally not exceeding 3%). This means that with a current SOFR rate of 3.65%, someone experiencing a reset could see their rate rise to between 5.9% and 6.4% (Chart 4). However, there is an important caveat in place that may limit that increase: interest rate caps.

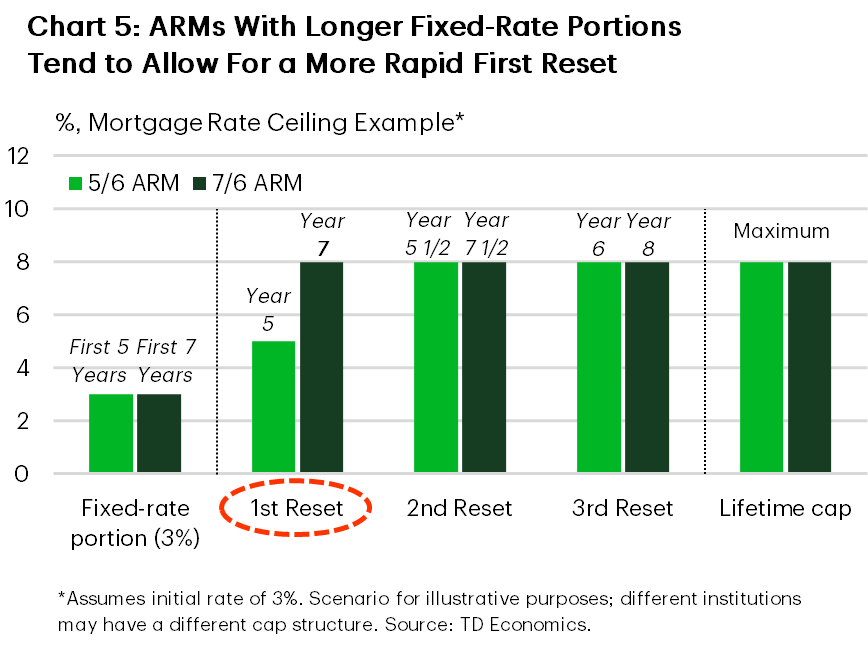

ARM interest rate caps place firm limits on how much a borrower’s rate—and therefore monthly payment – can increase over time. These caps are typically expressed in a three-part format: initial, periodic, and lifetime. For example, a common 2/1/5 cap structure – standard on many ARMs with a shorter-term fixed portion, such as below 5 years – means the interest rate can rise by no more than 2 percentage points (p.p.) at the first adjustment, 1 p.p. at each subsequent reset (typically every six months), and no more than 5 p.p. over the life of the loan. This means that a borrower who started out with 3% – a rate that was not uncommon early in the pandemic – and is now facing a reset, may not see their rate exceed 5% at the first reset. The rate would creep higher at subsequent six‑month resets by 1 p.p., but could never rise above 8%, regardless of market conditions. Importantly, these ceilings are anchored to the starting rate. With today’s ARM rates starting in the mid‑to‑high 5% range rather than near 3%, the permitted lifetime ceiling would be much higher. This is a key consideration for borrowers who specifically expect to hold an ARM well into the readjustment phase. Moreover, this may be more relevant for ARMs with longer initial fixed‑rate periods, such as the 7/6 or 10/6, which often carry a 5/1/5 cap structure, allowing a larger initial adjustment of up to 5 p.p. while preserving the same lifetime cap as the 2/1/5 structure.

Caps provide important consumer protection by limiting how much an ARM’s interest rate – and therefore monthly payments – can rise over time (Chart 5). That said, it is important to note that downside adjustments are also constrained. Most modern ARMs include a rate floor, typically set equal to the lender’s margin, which limits how far the mortgage rate can fall at reset dates, even if the benchmark rate declines sharply.

ARM Use Has Increased Slightly, Led by High-Priced Regions

Adjustable-rate mortgage (ARM) use has ticked up from its pandemic-era lows and is now hovering in the high single digits as a share of new loans. ARMs make up roughly 8% of recent originations, up from only about 2% at the market trough in 2020. This remains a far cry from the mid-2000s housing boom, when nearly one in three mortgages had an adjustable rate. Importantly, today’s ARM resurgence is highly region-specific, concentrated in high-cost coastal markets where affordability is most stretched. For example, approximately 31% of all mortgages in California last year carried an adjustable rate – the highest share in the nation – while similarly elevated usage was recorded in the Washington, D.C. area (around 28%) and Massachusetts (24%). Other East Coast states with elevated ARM exposure include Connecticut and North Carolina. By contrast, in lower-cost regions of the Midwest and parts of the South, ARM usage remains much smaller and 30-year fixed loans continue to dominate.

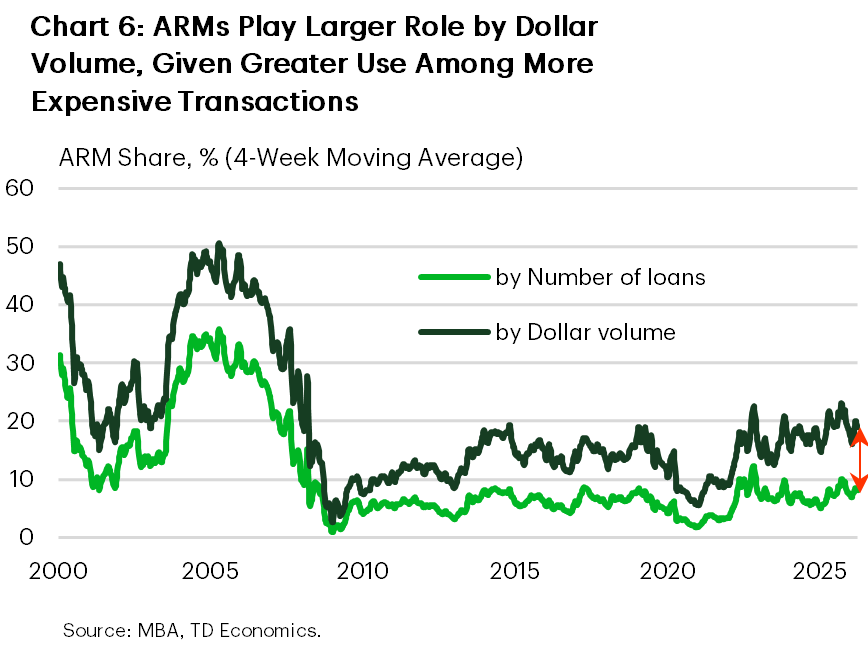

ARM usage is also pronounced in the luxury and high-end housing sectors. According to a recent Cotality report, by the end of 2025, nearly half of all mortgage originations exceeding $1 million were ARMs. This pattern is also evident when comparing ARM loan counts with the associated dollar volumes, the latter being disproportionately higher (Chart 6).

This geographic and price-tier skew reflects the reality that in very expensive markets, borrowers are more likely to leverage ARMs’ lower initial rates to qualify for a loan or to reduce monthly payments.

Text Box: A Note on ARM Product Variation Across Institutions

This report focuses on the modern hybrid ARM products that dominate new ARM originations today. The discussion of hybrid ARMs here reflects broad trends. In practice, ARM structures can differ a bit more from one institution to another relative to the typical 30-year fixed, reflecting differences in funding models and risk management. For example, lenders may offer different cap structures, margins, or reset conventions. Some institutions – particularly portfolio lenders – may also offer niche ARM options, such as jumbo loans or, in limited cases, interest-only structures, which are still subject to Ability-to-Repay requirements. These differences help explain in part why ARM pricing – or discounts vis-à-vis the 30-year fixed – can show a bit more variation across lenders.

When the stars align: ARMs with Longer Fixed-rate Terms Can Deliver Certainty When It Matters Most – Along with a Moderate Rate Discount

One of the strongest arguments for reconsidering ARMs lies in the mismatch between how mortgages are structured and how homeowners actually behave. For borrowers that don’t plan to stay in their homes over the long term, or comfortable with refinancing relatively soon, ARMs with shorter-term fixed portions (e.g., 3/6 or 5/6) may be a good fit, aligning with their expected tenure or refinancing plans and generally offering a strong discount. However, for the typical buyer planning a longer-term stay, these sorts of mortgages could run the risk of exposing them to some interest-rate risk in later years, in the readjustment phase. Still, ARMs with longer fixed-term portions would help reduce that risk further.

It is important to note that while most new owners today continue to select a 30-year fixed mortgage term, the reality is that most borrowers do not keep the same loan – or even the same home – for anywhere near that long. Estimates suggest the typical U.S. homeowner tends to end their original mortgage loan within 7 to 10 years.3 Meanwhile, the typical homeowner tends to stay in their home for slightly longer, at around 12 years.4 Both are well below the typical 30-year mortgage contractual term. Regarding these timelines, note that people tend to move for all sorts of reasons – such as moving to a larger home to accommodate a growing family, upgrading to a better-quality home, downsizing later in life, or moving due to other life reasons (i.e., divorce, new job, etc.) – generally ending their existing mortgage when doing so. Additionally, refinancing, either to lower their monthly payment when interest rates fall, or to pull equity out of the home, is another major reason why some loans are terminated long before maturity.

In this context, for the buyer planning a longer-term stay, ARMs with a longer fixed-rate portion, such as a 7/6 or 10/6 SOFR ARM, may often align more closely with expected lifecycle of the loan than the standard 30-year fixed. Thus, choosing an ARM with a longer fixed-rate portion would provide payment certainty during the period borrowers are most likely to hold the mortgage, while still enjoying the benefit of a rate discount.

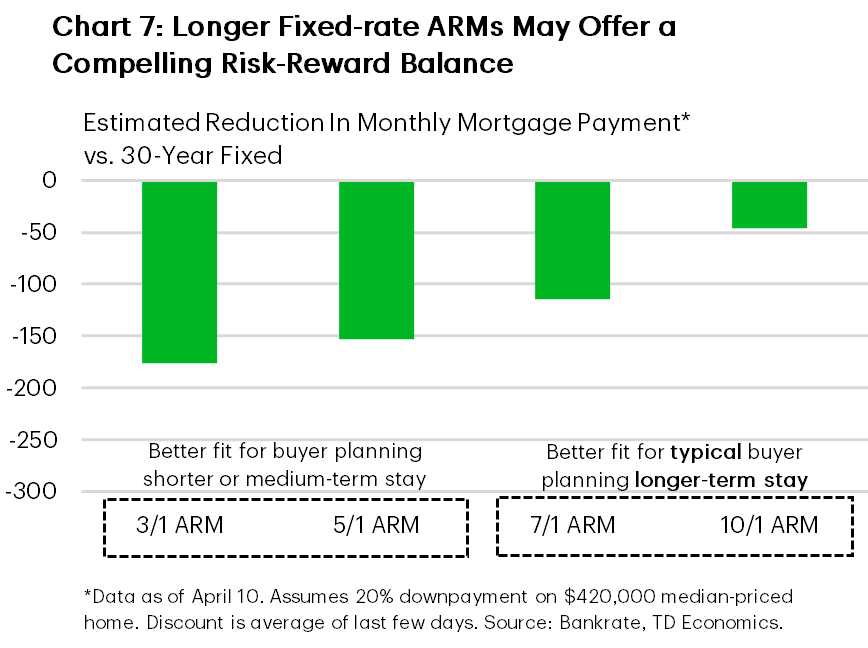

At present, the discount offered by the 10/6 ARM over the typical 30-year fixed is rather small, potentially limiting its appeal, but the discount offered by the 7/6 ARM is estimated at around 50 bps. For the typical home priced in the low $400,000s, this would help lower the monthly mortgage payment by about $115 dollars (Chart 7). For the average buyer who will only keep the mortgage for 7-10 years anyway, the 7/6 ARM may offer a compelling risk-reward balance.

The Bottom Line

Elevated mortgage rates continue to weigh heavily on housing affordability, and while policy responses may eventually lend a hand, practical financing choices can also provide some relief at the margin. In this context, adjustable-rate mortgages may warrant a closer look. Though they carry a tarnished reputation rooted in their role in the last housing crash, today’s ARMs reflect stronger underwriting, longer fixed-rate periods, and explicit guardrails that can help limit payment shock.

The discount that ARMs offer tends to vary over time. In today’s mortgage rate backdrop, most ARMs still offer a decent discount compared to the typical 30-year fixed mortgage. The case strengthens further once borrower behavior is taken into account. Buyers who plan to move or refinance within a few years may find ARMs with shorter fixed periods a good fit. But today’s ARMs have the potential to yield benefits even for those planning for the long haul. The truth is that while most borrowers select a 30-year mortgage, most don’t hold these loans for anywhere that long, with the typical loan lifecycle clustering in the 7-to-10-year range. For this cohort, ARMs with longer initial fixed periods – such as a 7/6 – can align more closely with the expected life of the loan, delivering interest-rate certainty in the period when it likely matters most, while still offering a meaningful discount.

Ultimately, ARMs can serve as a valuable affordability tool in today’s elevated rate environment, but they make a better fit for informed buyers who understand the terms, benefits, and trade-offs.

End Notes

- SOFR is a benchmark interest rate that measures the cost of borrowing cash overnight, secured by U.S. Treasury securities.

- Ability-to-repay rule requires mortgage lenders to make a reasonable, good-faith determination that a borrower has the ability to repay a loan before extending credit.

- The average mortgage duration is generally considered to be 7-10 years (see https://www.fanniemae.com/research-and-insights/publications/housing-insights/rate-30-year-mortgage). The prevalence of low-rate loans obtained during the pandemic, and the clear benefit for existing owners to hold on to them, is likely contributing to lengthening the typical lifecycle of a loan at the margin.

- For homeowner tenure, see https://www.redfin.com/news/homeowner-tenure-12-years/

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: