Cryptocurrency Crisis:

Containment, not Contagion

Vikram Rai, Senior Economist | (416)-923-1692

Date Published: January 5, 2023

- Category:

- US

- Financial Markets

The world of cryptocurrencies has been top of mind for many investors since the collapse of FTX in November, previously one of the largest platforms to exist in the space. Following its bankruptcy, questions have arisen about whether the ongoing crypto devaluation is a risk is to the economy. We have collected some of the common questions and made our best attempt at answering them here.

- Q1. November's FTX collapse fueled fears of a more generalized financial crisis. Why have these fears not been borne out?

- Q2. Why did so many companies in the crypto world fail in 2022?

- Q3. Even if cryptocurrency losses are contained, aren't the losses bad for the economy?

- Q4. How can we know if another crypto platform will end up like FTX?

- Q5. Is this the end for cryptocurrencies?

Questions

Q1. November's FTX collapse fueled fears of a more generalized financial crisis. Why have these fears not been borne out?

FTX's bankruptcy had knock-on effects across the class of digital assets and companies operating in the space, but the fallout seems to have been contained within the sector.

The last time the collapse of a financial institution had economy-wide effects was in 2008 when Lehman Brothers collapsed. At that time, Lehman Brothers was both so large and so entangled with the entire financial system that its collapse had a large impact on overall financial activity.

These two conditions are absent in the case of FTX. While its peak market capitalization of $US 32 billion is not small, it is orders of magnitude smaller than the $US 600 billion balance sheet of Lehman Brothers in early 2008. Similarly, the closed-loop nature of digital asset financing has helped contain the fallout. FTX's largest unsecured creditors – those who can take a total loss if the company fails – are all identified in its bankruptcy filings as "customers," which is to say they are account holders. While undoubtedly painful for FTX's customers, these losses are unlikely to impair the functioning of the financial system as a whole.

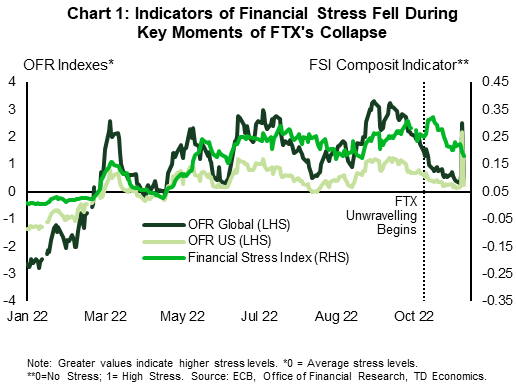

Chart 1 shows that following the run on FTX beginning in early November, indicators of stress in financial markets declined. In fact, there were greater signs of stress in early December when the EU oil embargo and OPEC meeting were top of mind in financial markets.

The SEC's complaint against FTX also identifies FTX's investors – primarily private equity and venture capital funds – as taking losses due to FTX's activities. These funds are accustomed to making riskier investments and so it is not surprising that their losses, even on this large a scale, were not destabilizing to the financial system.

Q2. November's FTX collapse fueled fears of a more generalized financial crisis. Why have these fears not been borne out?

One reason is that there was a domino effect from FTX's bankruptcy. The company had obligations to a number of companies, which its bankruptcy means it could not honor. For example, FTX was set to assume control of BlockFi, a crypto platform which failed earlier in the year, and make their customers whole after it was on the edge of bankruptcy. FTX was no longer able to do so after itself declaring bankruptcy, leading BlockFi to file for bankruptcy in November.

But another, more general factor is that the collapse in value of the Terra/Luna ecosystem earlier in 2022 diminished confidence in the asset class in general, posing funding challenges for all crypto issuers and exchanges. The platforms and issuers that failed throughout 2022 tended to have losses related to the collapse of Terra/Luna. FTX is the latest and largest such company, for now.

The year also saw most asset classes fall in value, as interest rates increased, and it is against this backdrop that cryptocurrencies fell in value1. As interest rates have marched higher, retail and institutional investors alike have reduced their risk appetite, and this has driven some of the correction in both the asset value of digital assets, and the value of companies issuing or trading them.

Q3. Even if cryptocurrency losses are contained, aren't the losses bad for the economy?

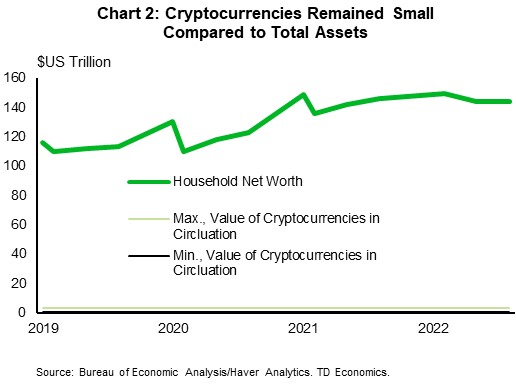

Losses last year are undoubtedly painful for those who had deposits with affected companies, and the companies that failed were valued in the billions. But even these large figures pale in comparison to global assets. Chart 2 shows that over the last several years, even the highest market value achieved by all digital assets in aggregate is just a fraction of the net worth of US households and non-profits.

Additionally, the exposure seems to be manageable at the individual level for most holders of cryptocurrency. Among those who hold cryptocurrency, the median holdings are less than one week of income across the income spectrum.2 There is also evidence that investors in cryptocurrency tend to be higher-income and wealthier, meaning that they have some cushion for to absorb losses.3 We would therefore expect any hit to household consumption from this loss of wealth to be fairly small.

Q4. How can we know if another crypto platform will end up like FTX?

The short answer to this question is that we cannot. Six months ago, FTX appeared to outsiders to be on firm footing and a leader in the industry. But like FTX, similar platforms today largely raise funds in private markets and from depositors, do not make meaningful financial disclosures, and are opaque about what is on their balance sheet and how they manage risks. At a minimum, the lack of transparency makes it impossible to know whether other exchanges would be able to handle a similar run on deposits or sudden withdrawal of funding.

One consequence of FTX's fallout is that there are now greater pressures for exchanges to offer proof of reserves, and to increase their transparency generally. There may also be more activity from regulators to avoid a repeat of this episode. If protective measures grow, through the proliferation of best practices and through regulation, it will become easier for investors to have confidence that they are not simply waiting for another shoe to drop.

Q5. Is this the end for cryptocurrencies?

The so-called "crypto winter" of 2022 may be the end of the regime that we grew familiar with over the past few years, one in which new cryptocurrencies, platforms, and exchanges sprung up, grew exponentially and then just as quickly disappeared.

But investor interest in the industry seems to have some durable motives. Investors with high risk tolerance have an interest in pursuing the potential high upside from innovative technology. And there will likely always be some interest in decentralized assets and payment mechanisms not controlled by governments. Today's weaker valuations and funding conditions may give the largest remaining exchanges opportunities for consolidation and diversification of their funding sources, and to position themselves for future innovations.

We anticipate that there will continue to be interest in the industry, but the use cases which attract the most attention are likely to evolve over time. The near-term outlook may be a case of consolidation and stabilization, while looking further out the industry's future hinges on what innovations lie ahead.

Footnotes

- See Cryptocurrency, Not a Safe Haven in 2022.

- https://www.jpmorganchase.com/institute/research/financial-markets/dynamics-demographics-us-household-crypto-asset-cryptocurrency-use

- https://www.philadelphiafed.org/consumer-finance/consumer-credit/cryptocurrency-ownership-insights-from-the-cfi-covid-19-survey-of-consumers

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: