Highlights

- Despite big shifts in trade policy, U.S. business investment was remarkably strong in 2025 – expanding by nearly 6% on a Q4/Q4 basis.

- However, nearly three-quarters of that growth was driven by investments in AI, while most other areas of investment were weak.

- Sizeable 2026 capex commitments by the hyperscalers suggest AI will remain a meaningful driver of investment growth. However, supply constraints could be a limiting factor on how far companies can push planned investments.

- At the same time, the combination of tax cuts, some easing in regulation and still-favorable monetary conditions should lead to some broadening in investment activity, despite the recent volatility in energy and equity markets.

- All told, we see business investment steadying at a healthy 5-6% pace this year, but with a more equal split between AI and non-AI driven investments.

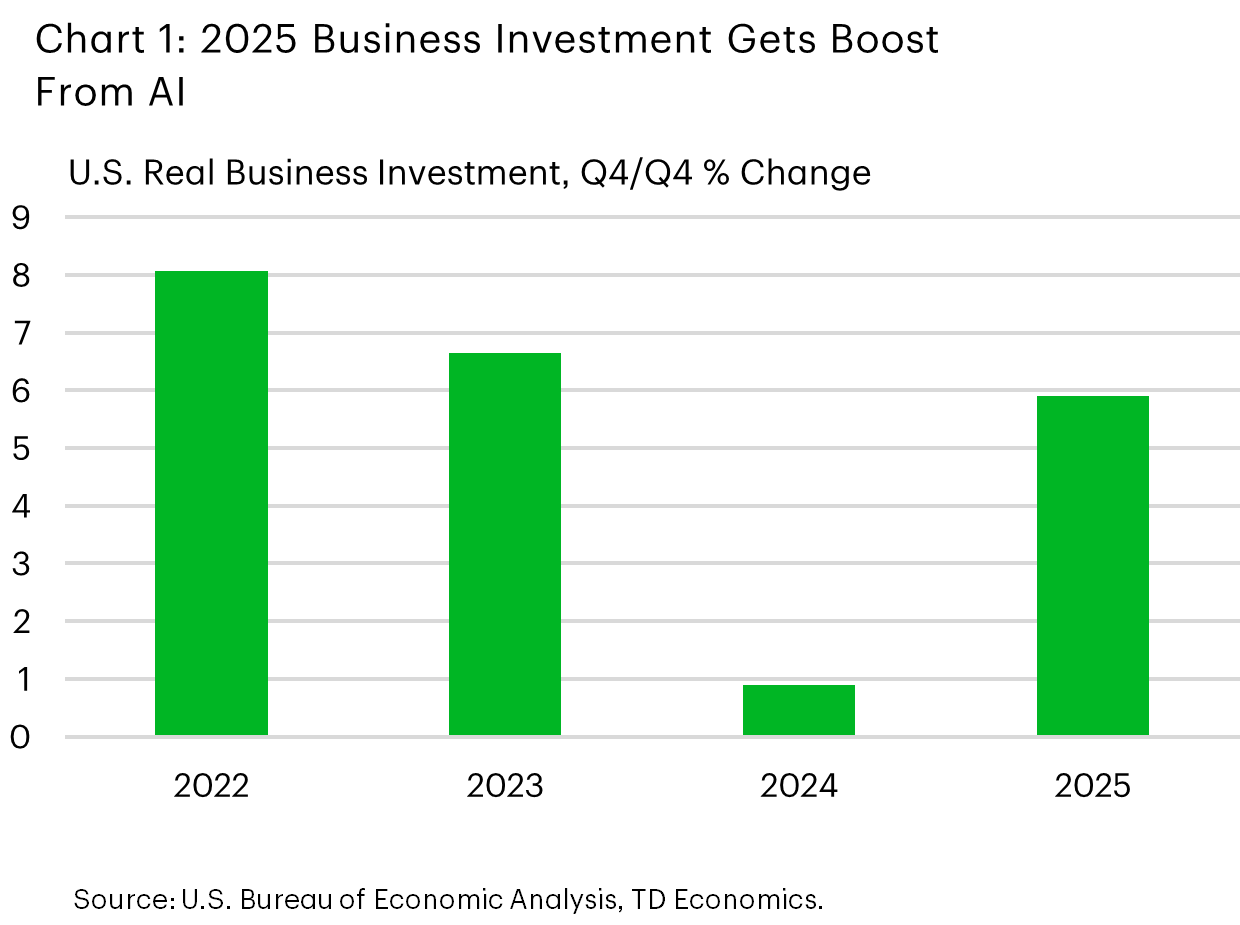

Despite all the trade uncertainty, 2025 was a remarkably solid year for U.S. business investment. Non-residential investment rose by nearly 6%, or six times faster than in 2024, measured on a Q4/Q4 basis (Chart 1). Investments in technologies related to AI were a significant driver, accounting for most of last year’s capital expenditures. Meanwhile, more traditional investment drivers remained relatively weak and narrowly concentrated, owing to both trade and other policy uncertainty and borrowing costs remaining restrictive, even with the Federal Reserve having cut its policy rate by a total of 175 basis points since September 2024.

Recent geopolitical events have injected a fresh dose of uncertainty, and has led to significant volatility in both energy and equity markets. But provided the conflict in the Middle East is short-lived, we think the backdrop for business investment remains quite constructive. While AI will continue to exert a meaningful thrust, we’re also likely to see some broadening in investment activity towards more traditional areas. Tax changes in the One Big Beautiful Bill Act (OBBBA) strengthen investment incentives, providing a key catalyst for growth. At the same time, more favorable monetary conditions and further deregulation should add to the tailwind.

AI punched above its weight in 2025

Investments in technologies related to AI materially moved the macro needle in 2025. But disentangling its exact contributions to business investment is far from straightforward. From a GDP accounting standpoint, there are at least three areas where AI investments are showing up.

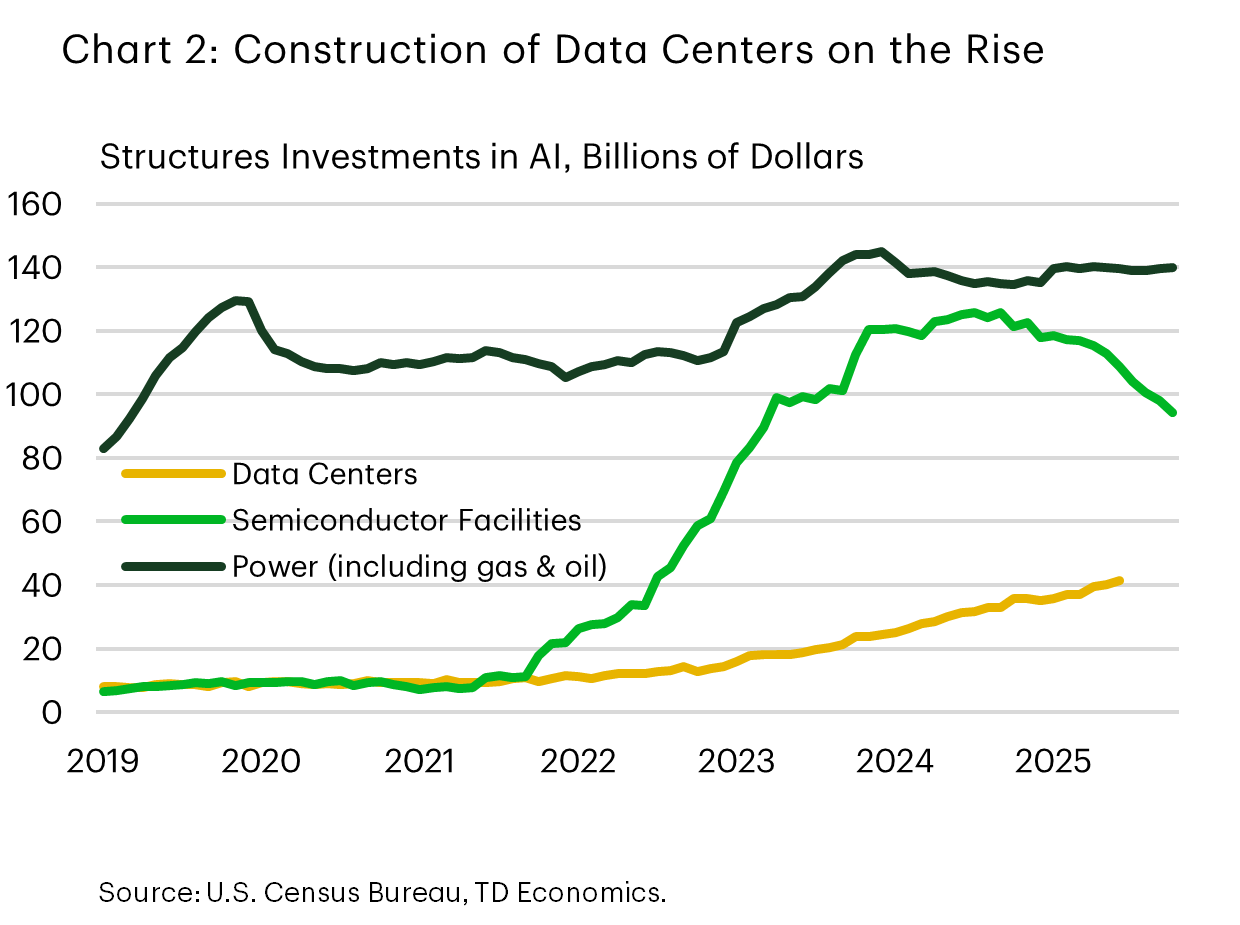

First, is spending on physical structures like data centers and semiconductor facilities. Investment in this space has exploded over the last several years and is likely to surpass $120 billion in 2025 (Chart 2).

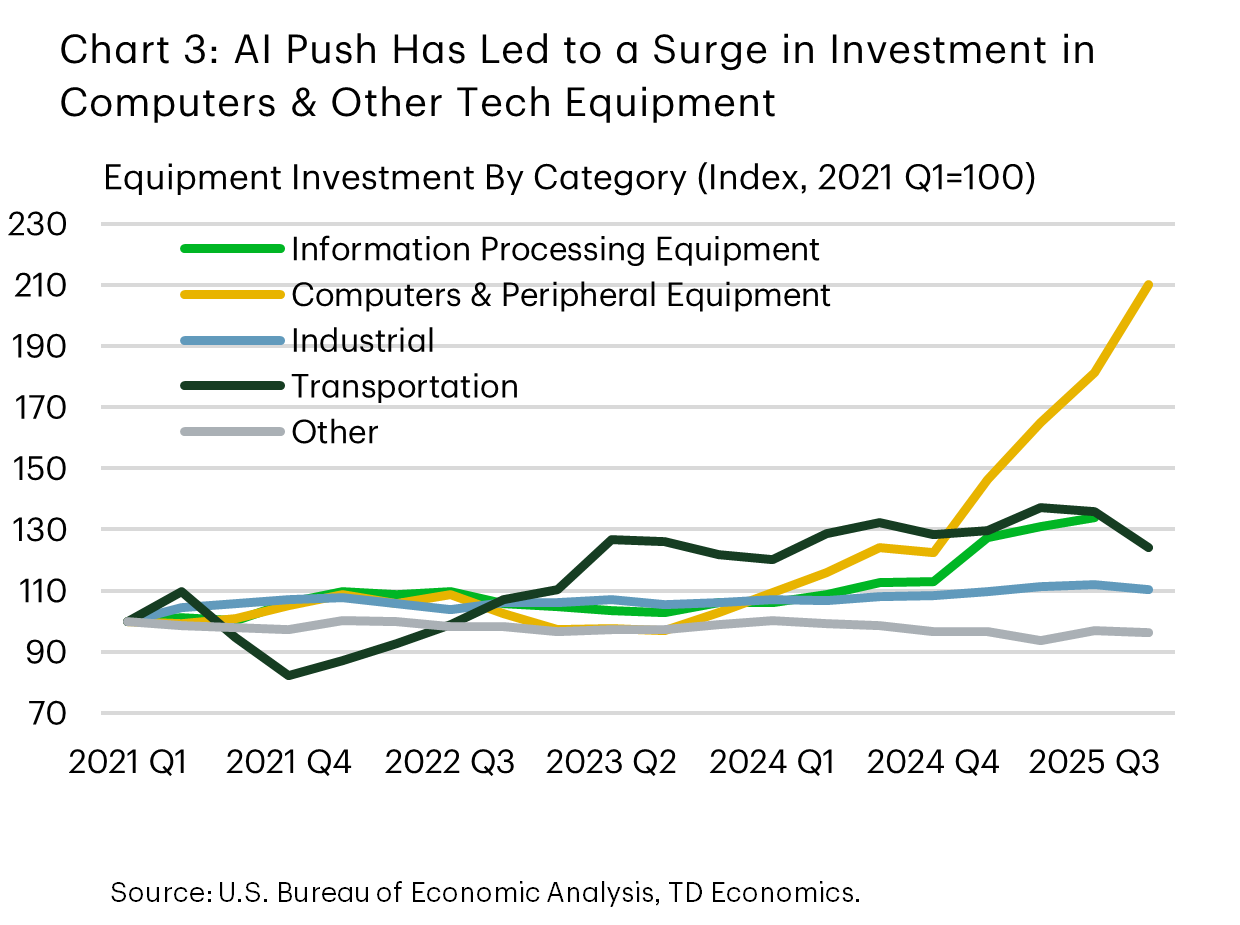

The second area is tied to the high-tech equipment used to power the data centers. This would include things like servers, accelerators, storage systems, network gear, and cooling systems. This spending is captured within computers and peripheral equipment, a sub-category of information processing equipment. Investment in this space has exploded over the last year, far outpacing all other equipment categories (Chart 3). However, not all of the growth can be attributed to AI. This category would also include traditional investments in computers and other tech equipment, where there’s long been a steady stream of investment to meet businesses day-to-day needs. In fact, between 2010-2020, capital expenditures in this category grew at an annualized rate of over 9%. If we assume a similar rate of growth in recent years, then it’s the difference between the actual series and its pre-AI boom trend that best captures AI’s contribution, which looks to have amounted to around $137 billion in 2025 on an inflation adjusted basis.

The third category includes software and research & development, and a similar analysis as above suggests AI spending was $68 billion in 2025. All told, we estimate that AI-related investments were responsible for nearly three-quarters of all the growth in business investment last year, despite only accounting for roughly 8% of total capital expenditures.

Most other investment categories have lagged

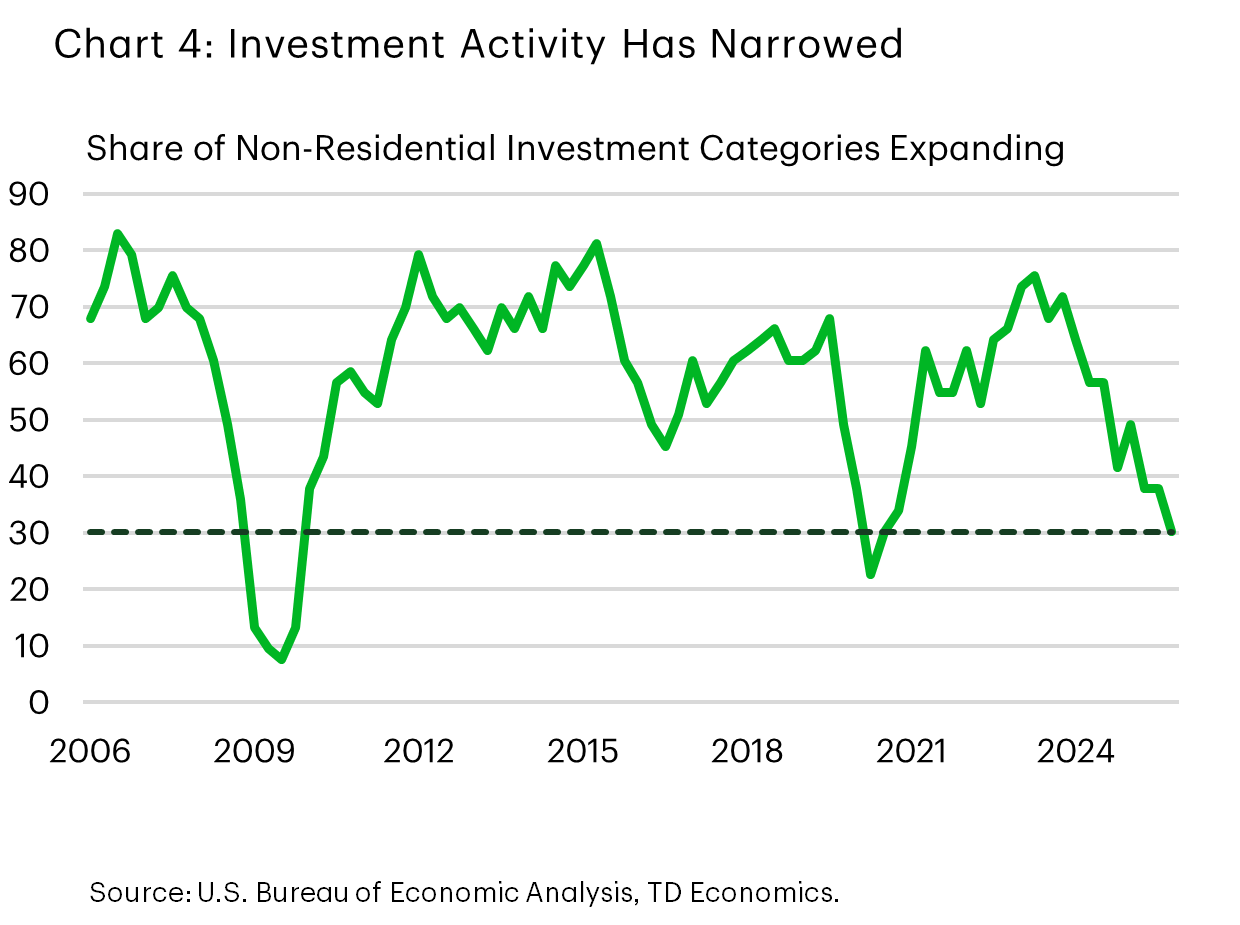

After removing the effects of AI, all other investment activity was relatively weak in 2025. Of the 50+ investment categories, less than a third experienced growth, and that would include the segments that would have benefited from increased AI spending. Putting aside the 2020 Global Pandemic, the lack of breadth in investment is something that hasn’t been seen since 2010, when the economy was still reeling from the global financial crisis (Chart 4).

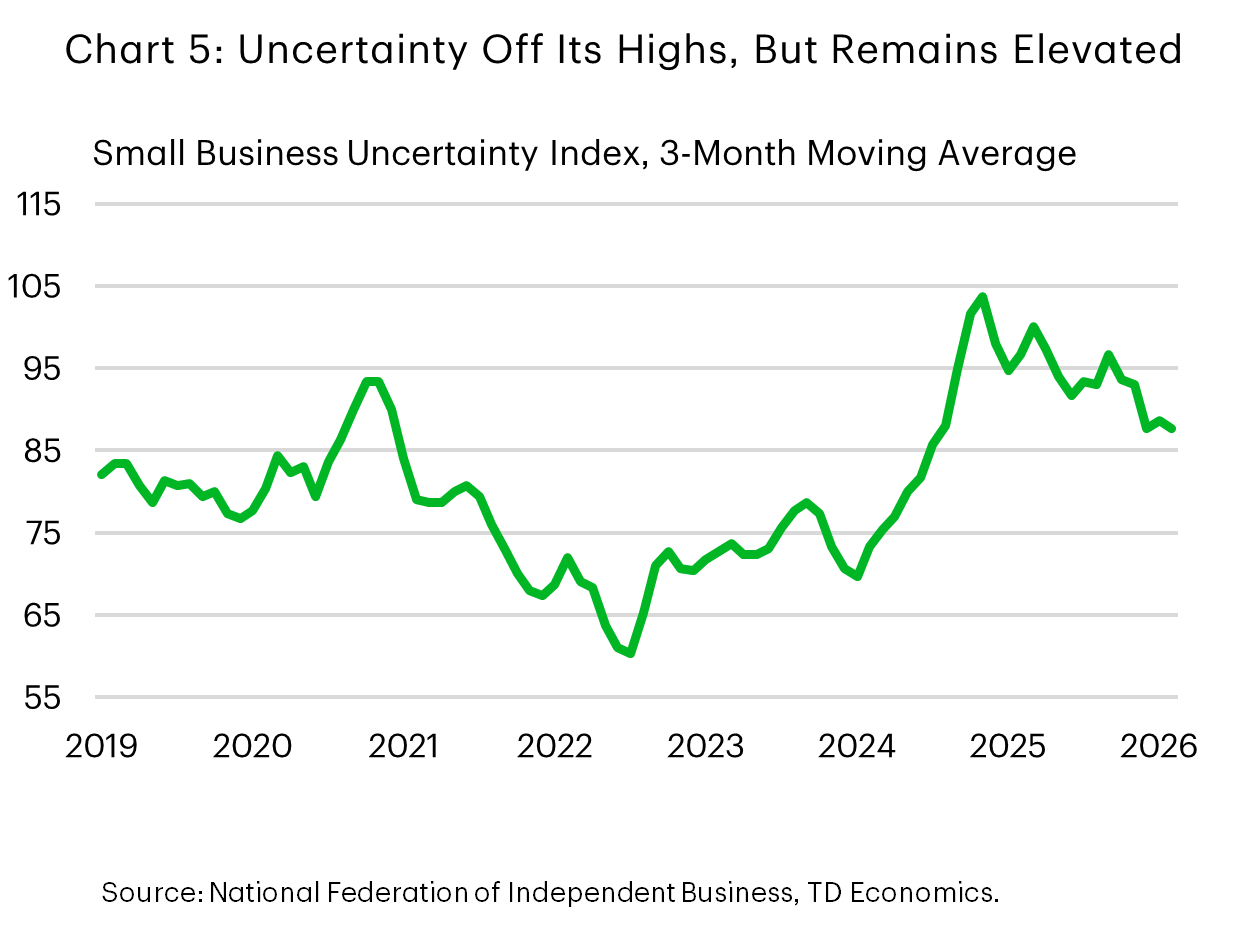

Big shifts in trade policy help to explain some of the softening in capital expenditures, but it doesn’t tell the entire story. As seen in Chart 4, investment activity started to narrow in late-2023, not long after the Fed had reached the end of its tightening cycle. At its peak of 5.5%, the fed funds rate was the highest in nearly two decades. The resulting tightening in financial conditions was likely the initial catalyst behind the slowdown, particularly in the more interest-rate sensitive categories like equipment and structures. While the Fed subsequently cut rates by a total of 100 basis points by the end of 2024, its effects were unlikely to have been felt before the new administration started to implement its trade agenda, which worked to amplify uncertainty (Chart 5).

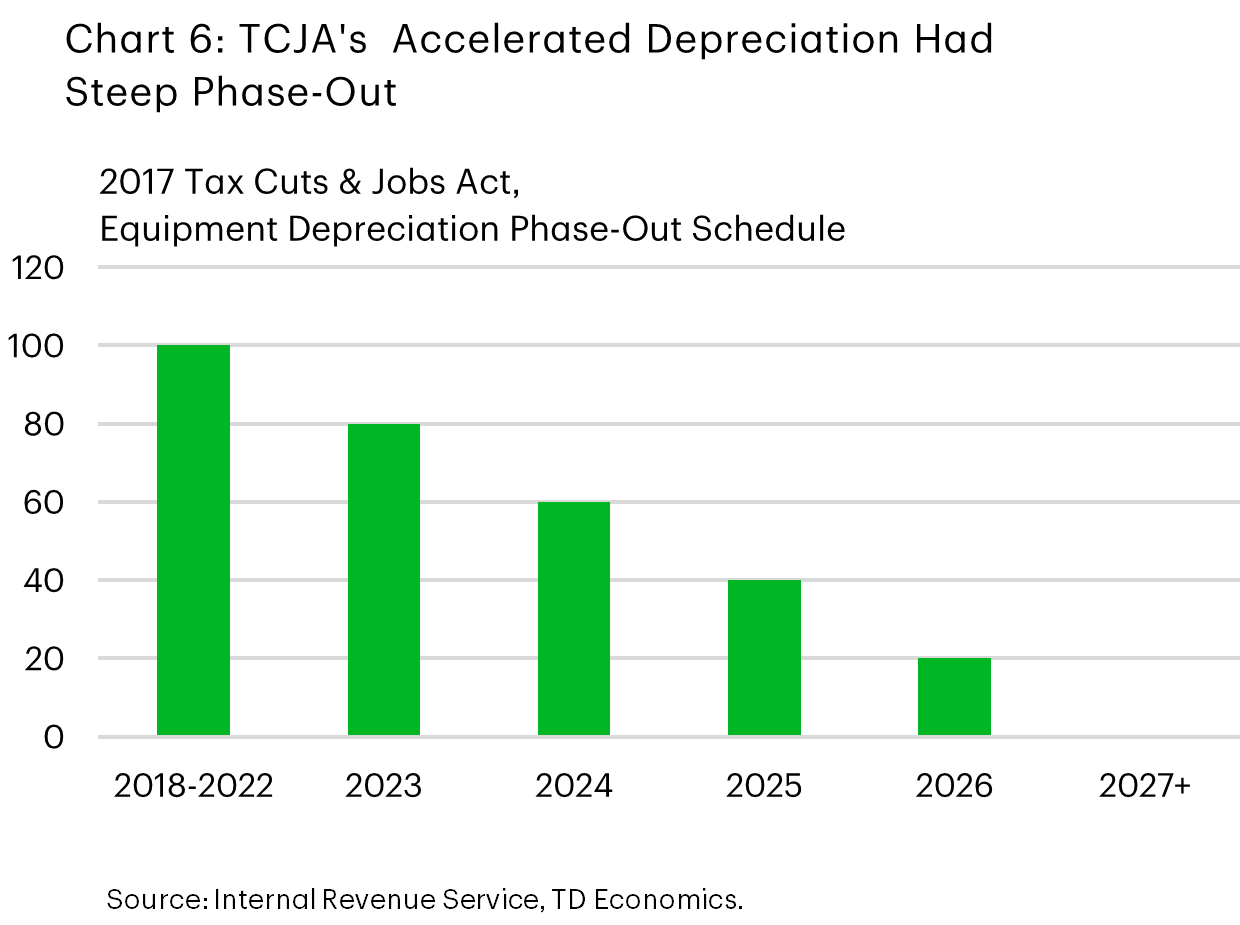

In addition, investment spending may have also been held back by companies waiting for changes in tax policy under the new administration to be finalized. With some of the lucrative deductions included in the 2017 Tax Cuts & Jobs Act (TCJA) like the 100% bonus depreciation having been well into the phase-out stage, business owners likely delayed projects in the hopes that similar programs would be reinstated (Chart 6).

2026 has ushered in new tailwinds, and a headwind

As expected, the One Big Beautiful Bill (OBBBA) introduced several new tax changes for businesses designed to lower taxes and spur investment. Perhaps the most notable changes were to tax breaks for investment spending. For starters, the OBBBA reinstated the 100% bonus depreciation and made it permanent for all qualifying property (i.e., machinery, equipment, etc.) acquired after January 19th, 2025, and extended it to research and development spending for the first time. The maximum amount a business can deduct for any piece of property was also lifted to $2.5 million (previously $1 million), with a $4 million phaseout. Business interest deductibility was also made more generous. Other changes such as making the qualified business income deduction permanent (expired in 2025 under TCJA) and introducing an employee retention tax credit are less likely to move the needle from an investment standpoint.

Exactly how much of a boost OBBBA will provide, remains to be seen. But past research on the impacts of the TCJA has suggested that the previous round of tax cuts did provide at least some boost to investment activity in the years following its enactment. One study recently published by economists at the National Bureau of Economic Research and U.S. Treasury estimated that the cumulative increase in capital stock could have been as much as 7%. However, about half of that was attributed to the permanent reduction of the corporate tax rate (from 35% to 21%), while only a quarter came from the implementation of the accelerated depreciation. This suggests the lift to investment from OBBBA could be much smaller.

Beyond the empirical studies, comparisons of consensus forecast projections versus actual investment data also suggest the TCJA had at least some impact. In early 2017, after President Trump took office and before the TCJA was introduced, consensus projected that real investment would rise 8% from Q1-2017 to Q4-2019. But the actual increase was closer to 14%.

That said, it’s unlikely that all the upside came from the TCJA. The Trump administration also eased regulation across several industries, including energy & environmental, financial, telecommunication and others by introducing a “two-for-one” regulatory policy. These measures also likely helped to create a more favorable investment climate.

While still early days, the current Trump administration has already made several moves to further ease regulation, including repealing the EPA’s endangerment finding, rolling back Biden-era emission limits and implementing sunset dates on new regulations. And we’re already seeing some of the effects playing out. M&A activity surged to near record levels in H2-2025, in part because of fewer regulatory roadblocks and some easing in consumer protection laws and antitrust enforcement. With more changes likely in the pipeline, the administration’s lighter touch on regulation is very likely to provide yet another tailwind for investment activity.

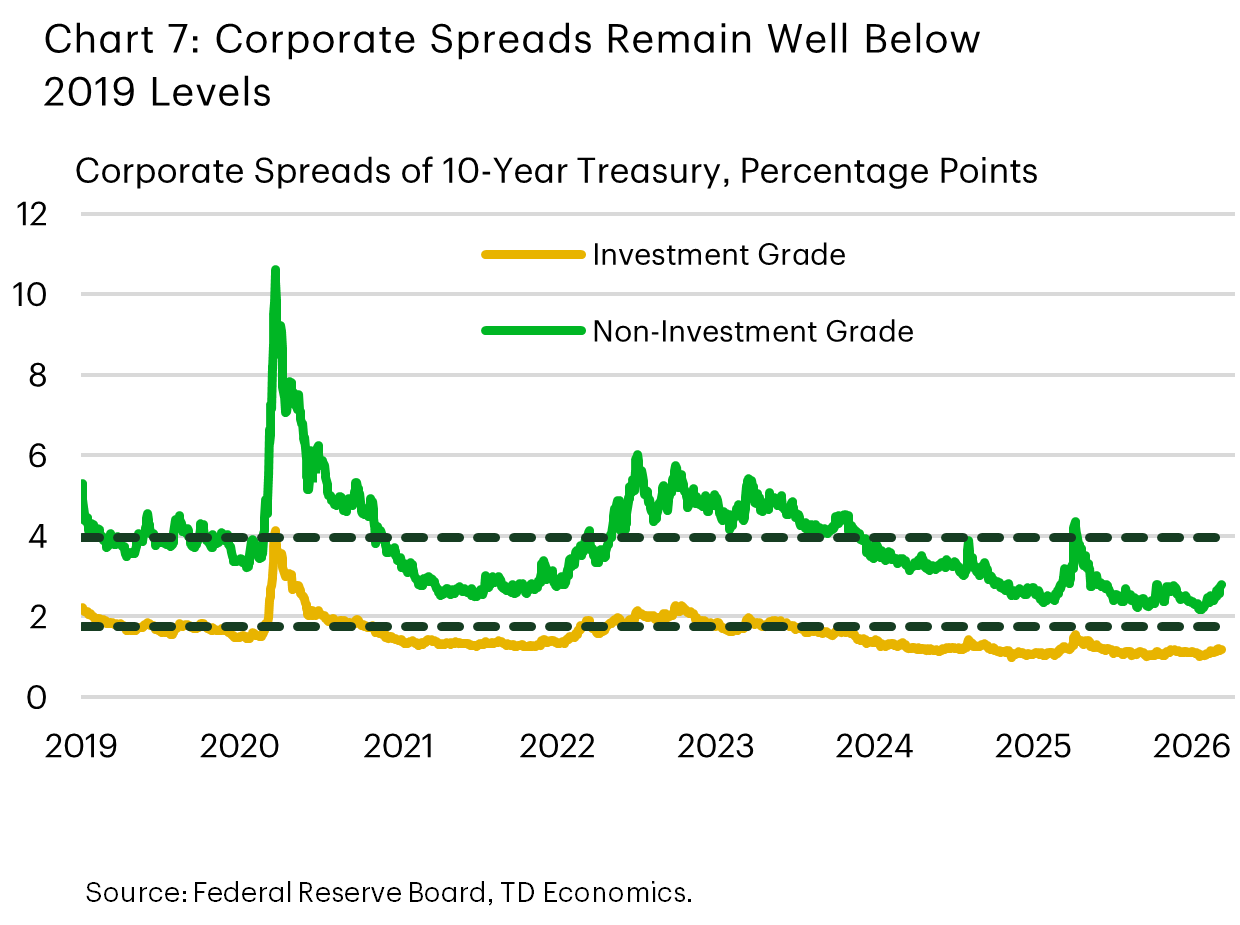

Lastly, we can’t overlook the impact of easier financial conditions. Even in the face of the recent Middle East conflict, our measure of financial stress (see report) suggests that while conditions have tightened on the margin, they remain “loose” by historical standards. Importantly, spreads on both investment and non-investment grade debt remain below 2019 levels, despite the current fed funds rate being 125 basis points higher (Chart 7). And, with the Fed expected to deliver two more rate cuts later this year, our base case is that financial conditions will remain supportive of growth.

Conditions are Aligning, Sentiment is Not

While the stars appear to be aligning for some broadening in capital expenditures, survey measures suggest business owners remain hesitant. According to the NFIB Small Business Optimism Index, only 18% of firms are planning to increase capital expenditures over the next 3 to 6 months. Outside of the pandemic, this is the lowest level since 2010. And this decline in sentiment came before oil prices started to move higher. But provided the conflict in the Middle East is short-lived, we don’t see it derailing business confidence.

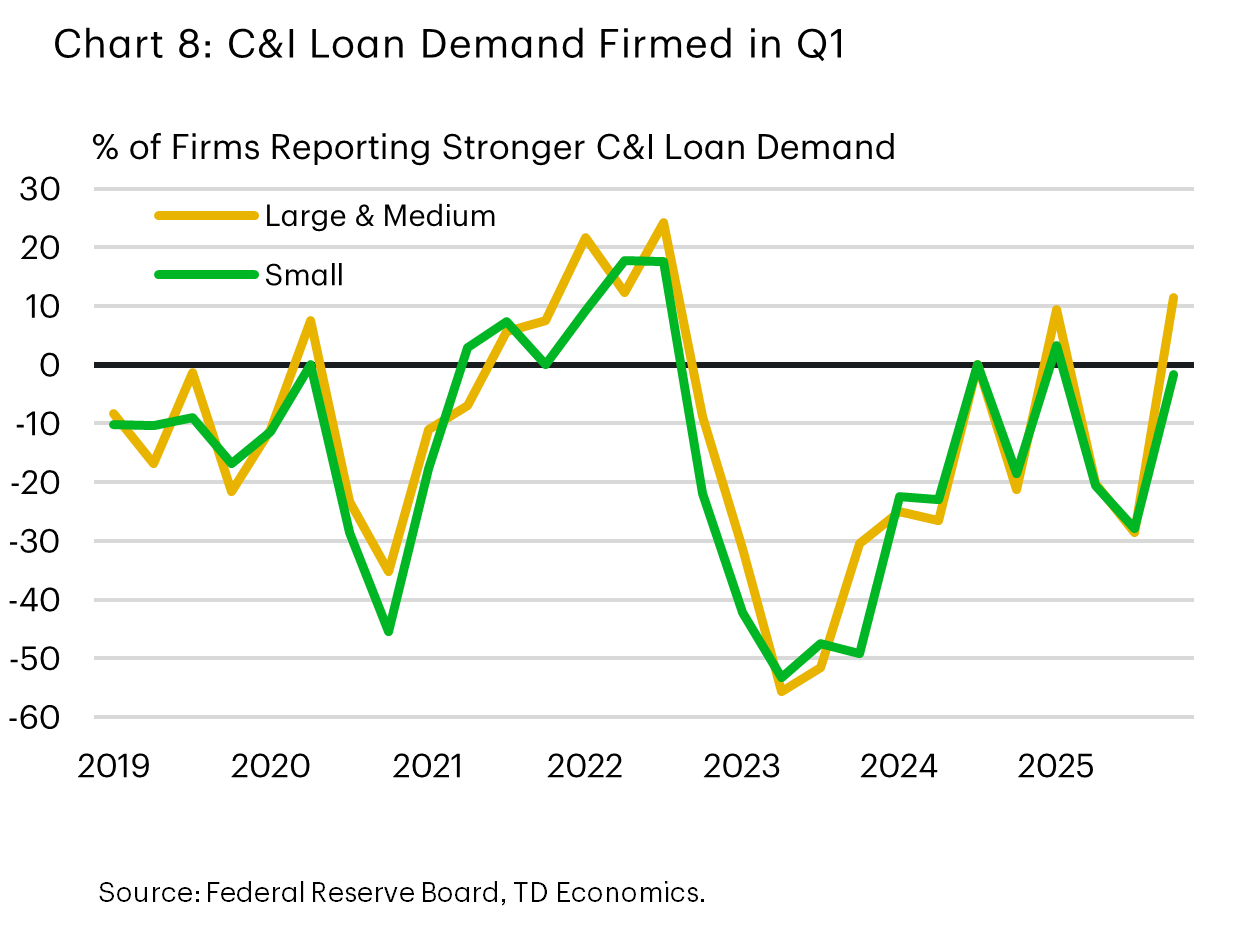

It’s also worth pointing out that sentiment measures have become a less reliable indicator post-pandemic. This is true of consumer and business confidence measures, where both have suffered from a loss in explanatory power, in part because the real economy is increasingly driven by asset prices, liquidity and financial conditions. Importantly, the Federal Reserve’s Senior Loan Officer Survey showed a meaningful pick-up in C&I loan demand for medium & large businesses in Q1 – rising to its highest share in several years (Chart 8). Loan demand from smaller businesses has also firmed. Higher frequency C&I loan volumes reported by the Federal Reserve corroborate the pick-up in early-2026, suggesting some broadening in business investment is already underway.

AI + Traditional Drivers Offer 1+2 Punch

Our forecast assumes the broader push for equipment spending is likely to coincide with another leg higher in AI investments. Planned capital expenditures by the “hyperscalers” (i.e., Amazon, Microsoft, Meta, Alphabet etc.) are expected to reach $700 billion this year, about a 60% increase from 2025. If that were to materialize, it alone could lift real non-residential investment by over 9%!

But we remain hesitant to put the full planned expenditure into our forecast. For starters, market analysts are already showing some reservations about the recent announcements on this year’s spending plans. This has been reflected in the broad selloff across the hyperscalers, despite most reporting solid earnings for Q4. If this were to persist, companies may ultimately decide to scale back 2026 investments.

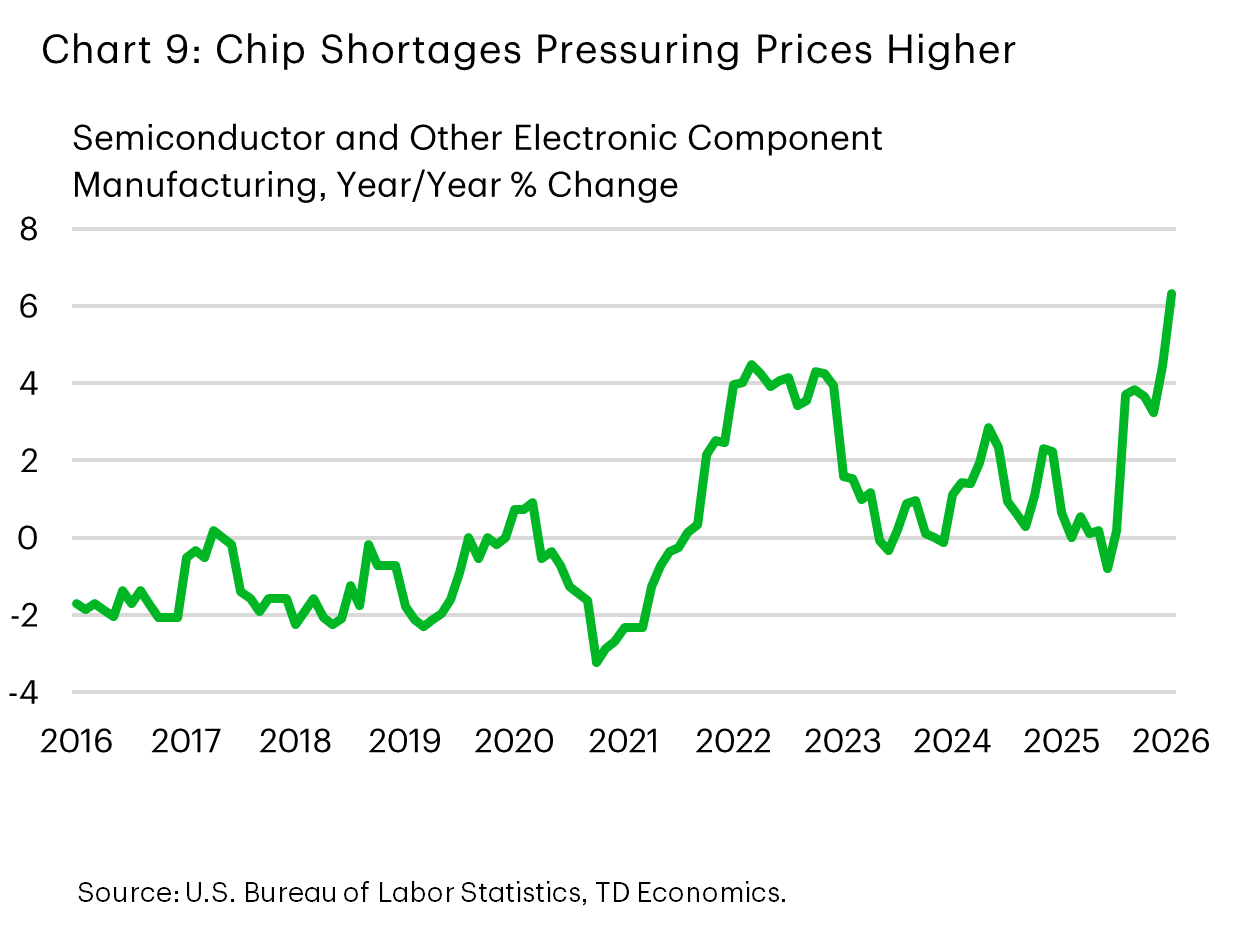

At the same time, the boom in AI data center construction is already leading to some semiconductor shortages. Semiconductor prices surged through H2-2025 and are now growing at a faster rate than in 2021-2022 – when the industry was hit with pandemic related supply chain disruptions (Chart 9). With the global supply of chips constrained, and demand growing at a parabolic rate, prices are likely to continue to push higher. We see this as a limiting factor on how far companies can push planned AI investments this year.

All told, we expect non-residential business investment to expand by a similar 5-6% pace in 2026. However, the split between AI and more traditional capital expenditures should be more balanced, with the latter benefiting from OBBBA tax cuts, less restrictive monetary conditions and more deregulation, while AI investments face capacity constraints and cost pressures. That said, risks to the outlook have risen in recent weeks following the onset of the conflict in the Middle East. This has brought big fluctuations in oil prices, but so far has only led to a modest tightening in financial conditions. A further escalation of geopolitical tensions, leading to a more material (and sustained) increase in oil prices and tighter financial conditions could delay some planned investments until next year.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: