Global Financial Conditions Tighten in Face of Middle East Conflict

Date Published: March 10, 2026

- Category:

- U.S.

- Commentaries

- Financial Markets

- Financial markets have whipsawed as hope emerged for the fighting between the U.S., Israel and Iran to cease. Financial conditions had tightened since the start of U.S. and Israeli airstrikes on Iran on February 28th. The prospect of the conflict continuing to simmer, or reigniting again, risks a steeper tightening in financial conditions that, together with a large energy supply shock, could result in weaker economic growth and rising inflation – often referred to as stagflation. That is a complicated situation for central bankers, who will have to decide whether to look through any “temporary” inflation shocks or react.

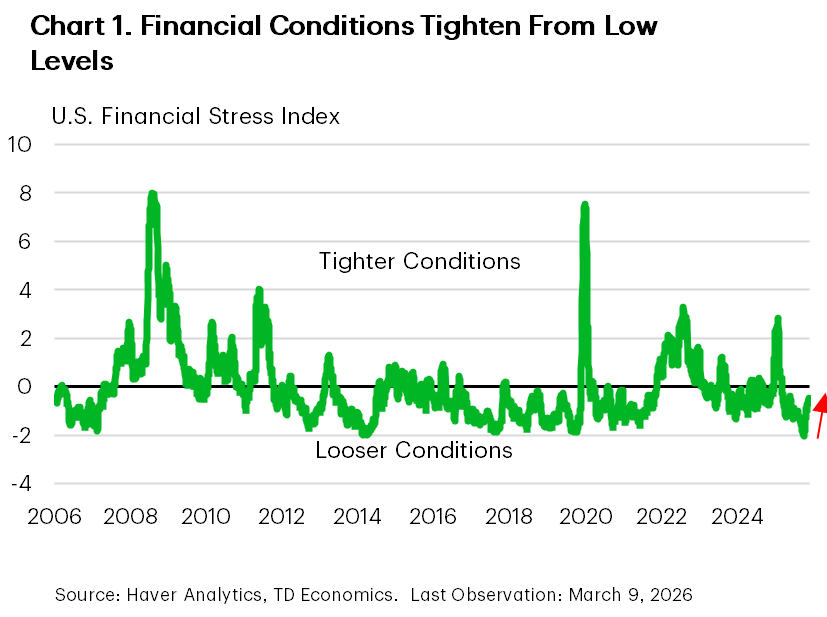

- However, even prior to Monday’s reprieve, U.S. financial conditions couldn’t yet be described as tight, likely benefitting from some flight to safety. That said, after six days of market moves, our U.S. index of financial stress had risen from notably loose levels in February (Chart 1), pushed up by volatility in bond and foreign exchange markets.

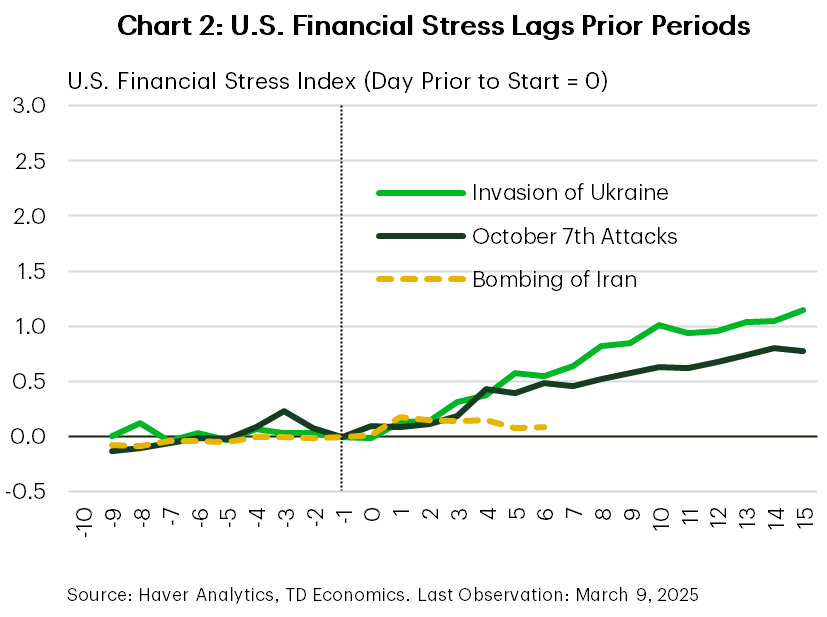

- Comparing last week’s moves in the stress index to two similar armed conflicts that disrupted energy markets (the Russian invasion of Ukraine in February 2022 and the October 7th, 2023 Hamas attacks on Israel) shows changes in U.S. financial conditions thus far fall well short of the prior episodes (Chart 2). However, it is notable that, unlike 2022, the Fed is not expected to imminently start raising interest rates.

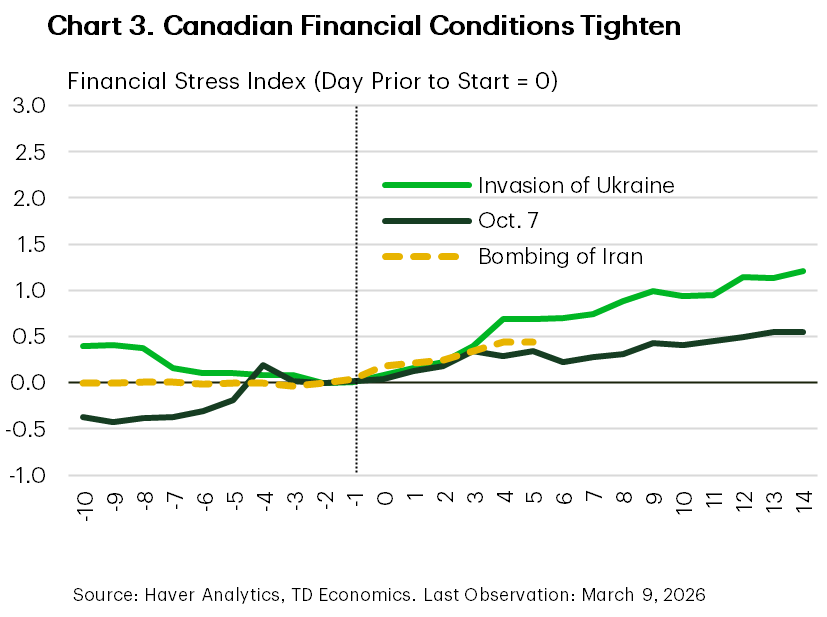

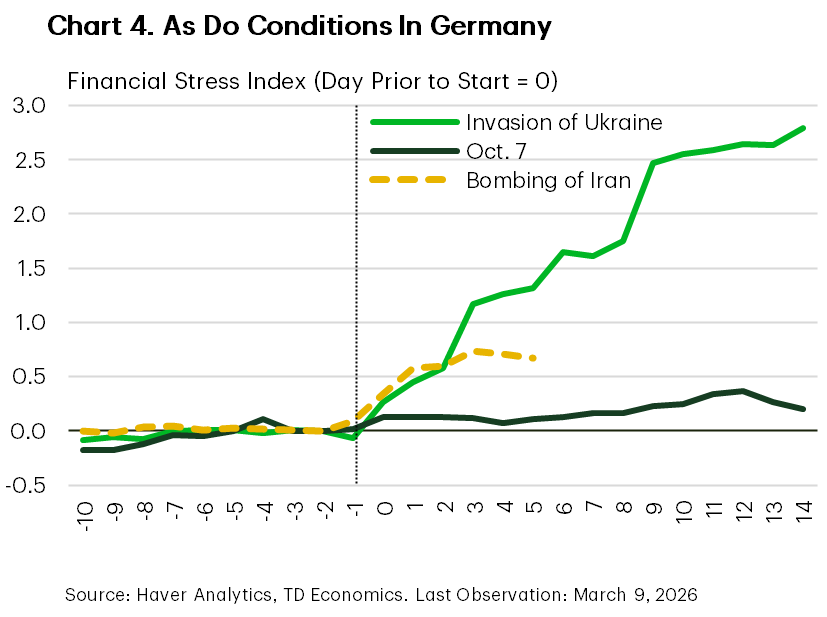

- Markets outside of the United States have generally seen a larger increase in financial stress (Chart 3 & 4). Among advanced economy markets, this is particularly the case for countries in the eurozone. Natural gas stores are low there, and there may be difficulty in replacing supply from Qatar if shipments through the Strait of Hormuz are disrupted for a prolonged period. The increase in financial stress in the eurozone is only slightly less than during the invasion of Ukraine in our tracking, but has slowed in recent days amid optimism of resolution.

- Moves in energy markets have been abrupt, but the peak prices from the Russian invasion of Ukraine haven’t yet been replicated as markets are starting from a position of excess supply. As of Monday’s close, WTI and Brent prices were still below $100 per barrel, compared to peaks of $123 and $128, respectively. However, the price increases thus far have been abrupt. Through Monday, WTI and Brent were up $27.8 (41.4%) and $26.5 (36.5%) since February 27th, compared to $15.6 (16.9%) and $13.8 (14.3%) over a similar time span in 2022. For energy markets, there are some notable differences in this episode. Europe has more diversified gas supplies than in 2022 and is not reliant on one of the conflict affected suppliers. Though it is reliant on shipments through the Strait of Hormuz, which have been disrupted by the conflict.

- Looking forward, how long the Strait is closed, and also how long the fighting in the region continues are key factors for medium-term impacts. The longer the disruptions last, the longer it is likely to take to restore supplies, leaving energy prices elevated and creating room for financial stress to accumulate.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: