Risk Assets One Year Later:

A Rising Tide Lifts All Boats

James Orlando, CFA, Senior Economist | 416-413-3180

Date Published: March 24, 2021

- Category:

- U.S.

- Financial Markets

Highlights

- Risk assets have soared over the last year. This has been led by equity markets, but quickly spread to a wide range of assets.

- This includes popular investable assets like housing, but also digital assets, like Bitcoin and non-fungible tokens.

- Looking forward, financial conditions will likely remain supportive of risk assets. That said, there are growing headwinds in the form of increasing interest rates, an eventual change in government fiscal supports, and the rising odds of a stricter regulatory environment.

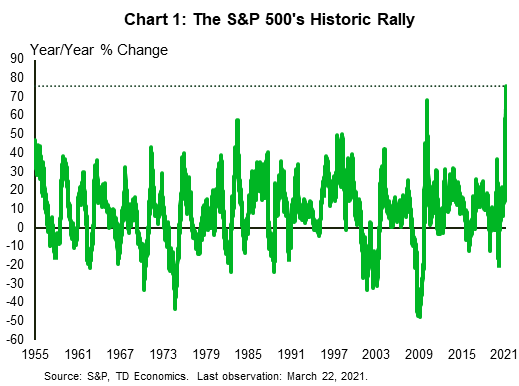

It has been one year since equity markets began rebounding from the pandemic-induced market sell-off. Since then, the S&P 500 Index and the Dow Jones Industrial Average have each increased a whopping 76% (Chart 1)! This has been the largest percentage increase over a 52-week period in since the Great Depression. Though equity markets get a lot of attention, investor optimism has pushed-up the value of an array of risk assets, including housing and digital assets (Table 1). Given the strong asset price appreciation, we decided to take stock -- no pun intended -- of just how far we have come over the last 12 months.

“The Everything Rally” in full swing

The start of the pandemic and subsequent restrictions caused a massive decline in economic activity that severely dented the profits of corporations. Thankfully, governments and central banks stepped in quickly and aggressively to support the economy. The existence of the safety net prevented a worst-case economic scenario and put a floor under risk assets. Market participants have gained confidence in these fiscal and monetary supports, and with millions of vaccines being deployed daily, the S&P 500 Index is now up around 16% from the pre-pandemic peak.

As we mentioned above, it isn’t just equities that have captured investors’ attention. The current bull market has been called the “Everything Rally”. This label highlights the fact that we have seen strong price appreciation in a wide range of assets. The notable exception to this trend has been longer maturity US Treasury bonds, which have seen negative returns as a consequence of the rising yield environment.

With the global recovery being driven by demand for physical goods, the surge in manufacturing has pushed commodity prices higher. The prices of raw materials, such as copper, lumber, and crude oil have all increased significantly. This has benefitted the currencies of commodity exporting countries and resulted in a broad sell-off of the US dollar.

The nature of the recovery has also put housing back in the spotlight. With demand well outpacing supply, U.S. house prices have increased by double digits over the last 12 months, with single-family homes seeing the largest year-over-year increase since the peak of the housing bubble in 2005. Part of this increase is the fact that mortgage rates hit record lows. The other part is that the pandemic incentivized people to dedicate more of their spending on improving their living situations. The consequence has been more buyers either upgrading or entering the marker earlier than they had planned.

We have also seen strong demand for alternative assets during this cycle. Whether it be demand for art, wine, or now digital assets, the price appreciation has been astonishing. The price of Bitcoin is a clear example, with the value increasing more the 10-fold from the low of 2020. This demand for cryptographic assets has even spawned an entirely new type of asset, called non-fungible tokens. These digital assets have garnered world-wide attention with the recent multimillion-dollar auction sales of digital art. Though we can’t assess the valuation of the art, the point to be made here is that there is a lot of money in the financial system and it is pushing up the prices of an increasing selection of assets.

Table 1: Asset Price Returns

| Asset Types | 1-Year Return* | Return (Avg. 2015-2019) | Return (Avg. 2010-2014) |

| S&P 500 Index | 76.1% | 11.7% | 15.5% |

| Global Dow Jones Index (ex-US) | 72.3% | 3.2% | 2.3% |

| US House Price Index (FHFA)** | 11.4% | 5.9% | 2.2% |

| US Median Sale Price (all existing homes)** | 15.8% | 5.7% | 0.0% |

| US Treasury Bill - 3 Month | 0.1% | 1.0% | 0.1% |

| US Treasury Note - 5-Year | -2.0% | 1.8% | 2.4% |

| US Treasury Note - 10-Year | -7.7% | 2.7% | 5.4% |

| US Inflation Index Treasury Note - 10-Year | 5.4% | 1.1% | 2.1% |

| Oil (WTI) | 216.0% | 0.2% | -4.4% |

| US Dollar vs Advanced Economy Currencies*** | -7.9% | 1.9% | 2.7% |

| US Dollar vs Emerging Economy Currencies*** | -4.3% | 3.5% | 1.1% |

| Bitcoin (in USD) | 770.2% | 86.3% | N/A |

Where to from here?

After this historic rise in valuations, what can markets possibly do for an encore? While macro-economic conditions will likely remain supportive, we are poised to see a transition whereby central banks and governments gradually reduce their supports, allowing the economy to stand on its own two feet again. We are already starting to see a glimpse of that future, with Treasury yields rising substantially. This has pushed up mortgage rates by about 50 basis point in the last couple of months. Over the next 12-18 months, the Fed is likely to stop increasing its balance sheet through its QE program, which has been injecting a ton of liquidity into the financial system. Rising yields and less liquidity growth may slow some of the insatiable investor demand. Other potential headwinds could also emerge on the tax and regulatory side, including new macro-prudential policies to address housing froth as well as higher corporate, wealth, or property taxes.

The debate will continue to rage about where markets head from here. What appears a safe assumption is that the year ahead will look different than the last one. We would expect that risk assets continue to record positive gains, but at a pace that is more sustainable.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share this: