Market Insight:

Greenback Exceptionalism

Beata Caranci, SVP & Chief Economist | 416-982-8067

James Orlando, CFA, Director & Senior Economist | 416-413-3180

Date Published: May 2, 2024

- Category:

- US

- Financial Markets

Highlights

- We have shifted our Federal Reserve call to only one rate-cut this year due to the recent back-up of inflation that does not meet the Fed’s “confidence” threshold to return inflation to 2% in a timely manner.

- With markets punting out Fed cuts but not doing the same for other countries, the U.S. dollar’s strength has no challenger until a pivot occurs in economic dynamics between countries or a geopolitical shift takes hold.

- An escalation of geopolitical risks is likely to add to the greenback’s strength, and even the outcome of the U.S. election could give it another leg up.

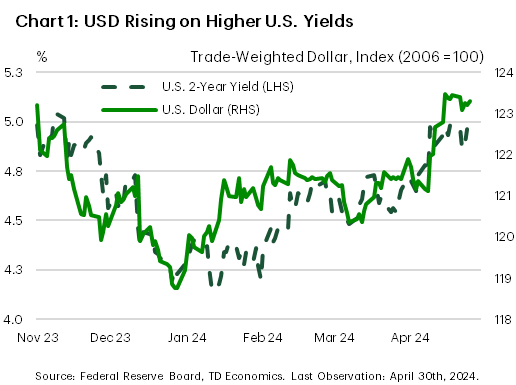

The U.S. dollar is flying high. Since last July, the broad trade-weighted dollar has appreciated nearly 5%, with much of that occurring over the first four months of 2024. Expectations for Fed rate cuts this year have nearly disappeared from the futures market, lifting U.S. Treasury yields and the greenback’s attractiveness (Chart 1). At the same time, a further intensification in geopolitical risks could result in another leg higher in the U.S. dollar.

U.S. exceptionalism and the dollar

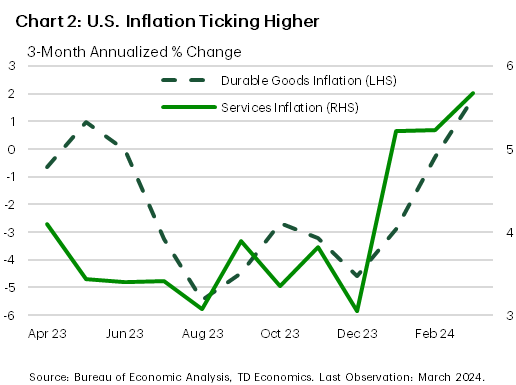

In February, we wrote about U.S. exceptionalism with economic growth and productivity unparalleled by peer countries. However, the ability for high productivity to continue to counter the forces of strong domestic demand on inflation was an open question that is now revealing an answer. Since the start of 2024, core inflation has turned higher in part due to strong spending on health care, recreation activities, and travel. Services inflation is back above 5% on a three-month basis (from 3% in December). To make matters worse, the deflationary impulse from durable goods evaporated in March – with prices now up 1.8% on a three-month basis compared to -4.6% in December (Chart 2).

In terms of the Fed’s preferred core PCE inflation measure, it is holding at a reasonable 2.8% year-on-year (y/y). But developments within the CPI metric foreshadow what’s to come. We expect core PCE to edge back towards 3% y/y in the coming months. This speaks to the staying power of inflation in the absence of a “growth sacrifice” within an economy holding in excess demand territory. From our perspective, consumer spending must ease for inflation to return, and be sustained, on a 2% path. There is only limited evidence of this, and certainly not enough to cause a sudden capitulation in underlying inflation dynamics. It’s not surprising, then, that markets moved quickly to reprice from 150 basis points in cuts at the start of the year, all the way to a total of 38 bps by year-end. Although we never sided with the magnitude of the market’s initial pricing over the January to March period, we agree with right-sizing the rate cuts to recent data developments. We have penciled in just one cut in December, aligning to when we forecast the 3- and 6-month trends in core PCE inflation will provide the central bank sufficient comfort of reaching its 2% target by mid-to-late 2025.

The story of America’s growth surge and inflation strength is, uniquely, American. Peer economies have weakened under the weight of their past interest rate hikes. The Euro Area and the UK produced negative GDP prints to close out 2023, while a country that typically benefits from U.S. exceptionalism – Canada – has posted a streak of negative GDP per capita over the last year. Poor economic performances have lent more confidence to these central banks that inflation can be tamed back to the 2% target in a timelier manner. Expectations for rate cuts have subsequently remained anchored around the summer time period, with an ongoing easing path priced thereafter ranging from 50 to 75 basis points by year-end. This would follow the Swiss National Bank and a handful of other central banks in the developing markets that have already cut interest rates.

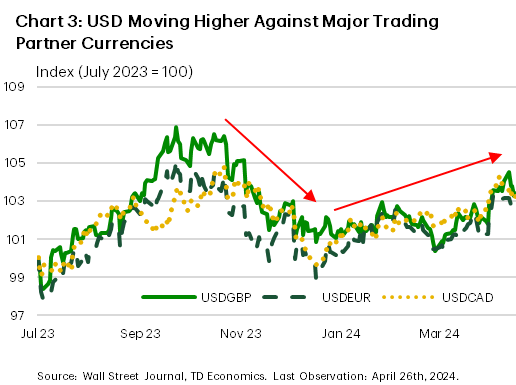

Expectations favoring widening monetary policy divergence has caused international government yields to diverge from U.S. Treasuries. While the U.S. 2-year is flirting with a cycle high at 5%, peer-equivalent yields have failed to keep up. Likewise, this has pressured currencies. The pound, euro and loonie are down between 4% to 5% in the last nine months (Chart 3). But given the 50 to 100 basis point central bank policy divergence expected by markets relative to the Federal Reserve, we think the next significant move in the U.S. dollar would require a new or larger catalyst.

Global risks picking up

It makes sense that the greenback typically appreciates when the U.S. economy is doing well. But the greenback also appreciates when geopolitical risks threaten the economy. This historical pattern is known as the ‘USD smile’. The latter is due to the USD’s safe haven appeal. When risks abound, investors seek the shelter of U.S. dollar assets. At this juncture, the global economy has plenty of risks to worry about. Russia has made more advances into Ukraine and tensions have deepened between Israel and Iran. Commodity markets are capturing this with the price of oil up nearly 10% in four months.

As our readers know too well, disruptions to energy supply can lead to economic instability. Just look at Europe’s energy insecurity since Russia invaded Ukraine. It is also more common for countries outside of North America to experience the negative economic impacts from higher oil prices due to less energy independence. A good comparison is the 1994 to 2000 period. During that time, the U.S. economy was leading the globe on the back of the technology revolution. And even though oil prices were rising throughout that period, the USD kept appreciating. It was an island unto its own.

What matters most in causing a depreciation of the U.S. dollar are homegrown risks, like the failure of LTCM, the bursting of the tech bubble, and the global financial crisis where the U.S. mortgage market marked the epicenter. None of these conditions are present today. The U.S. economy is on stronger footing than its peers when it comes to economic and financial risks, as well as being a net energy exporter.

That means it’s still possible for the U.S. dollar to have another leg up relative to peer currencies, it would likely require a “next-level” escalation in geopolitical events. This is entirely possible but difficult to predict, but some currencies are already showing significant vulnerability. The Turkish lira has depreciated about 9% to start the year, and some central banks are now intervening to defend their currencies. The Bank of Indonesia imposed a rate hike (rupiah down ~5%), and the Bank of Japan buying yen assets to backstop the currency (yen down ~10%).

And what about the upcoming U.S. election? Will this help or hinder the valuation of the greenback? Hard to say. Should a new administration enact harsh and broad tariffs on other countries, it could boost the USD. During the Trump administration, an escalation in U.S./China trade tensions saw an 11% appreciation in the greenback between 2018 and 2019. At the same time, policies that cause a rapid escalation in sovereign debt dynamics could move the currency in the other direction due to a market confidence shock. As yet, markets have not taken a side on either of these risks. Major currencies like the euro and loonie haven’t broken below their current resistance levels, even though yield differentials have been growing increasingly unfavorable. This supports the notion that the USD would require a fairly significant event to trigger risk-off sentiment to push against recent thresholds.

Bottom Line

The story of the U.S. dollar’s appreciation is one that intersects Fed policy and geopolitics. On the former, U.S. economic exceptionalism has pushed back the start of rate cuts towards December, widening the interest rate gap with other economies. This has been the driver of the first leg of the USD’s appreciation. While Fed policy might push the greenback a little higher over the coming months, a bigger leg-up would require a further intensification of geopolitical risks. And with the U.S. election quickly approaching, there are a significant number of events that could likewise cause the greenback to reach new highs, but also work against the currency if financial markets don’t like what they see on the domestic debt dynamics. At this stage, financial markets have not taken a strong conviction on either side of the risk. Investors are in wait-and-see mode.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.