I thought President Trump threw us curve balls last year, but the start of 2026 came completely out of left field. The year opened with the removal of Venezuela’s president by force, to questioning Greenland’s sovereignty. Next came threats of higher tariffs on EU countries that supported Greenland. This was another reminder that tariffs are the primary coercive tool of this administration regardless of the existence of trade agreements.

Then Canada got hit with a 100% tariff threat on all goods after the administration learned of an agreement with China to defuse its trade relationship on EVs and agriculture. But it didn’t stop there. The threat of 50% tariffs on Canadian-made aircrafts followed in response to delays on certifying Gulfstream jets. And to make sure Canada wasn’t feeling singled out, South Korea was threatened with a 10-percentage point lift in tariffs for not moving fast enough on their trade commitments with the U.S.

So that was the first 4 weeks of the year!

This presentation will cut thru the noise and review what’s new and not in the U.S. outlook. The main takeaway is that the U.S. economy has been unflappable, with the forecast materially revised up.

Let’s get going, starting with how to sort out all the tariff threats, which falls into the “not-new-camp”.

Trump’s National Security Strategy: Clear Economic Priorities

- Western Hemisphere is the priority and immigration is a major national security concern

- Economic Security “is fundamental to national security” and includes the following emphases to “strengthen the American economy”:

- Balanced trade

- Securing access to critical supply chains and materials

- Reindustrialization – strategic use of tariffs and new tech

- Reviving Our Defense Industrial Base

- Energy Dominance

- Preserving and growing financial sector dominance – leveraging free market system and our leadership in digital finance and innovation

- Emphasis on tariffs as a tool = unlikely to have tariff certainty in this administration

- Removal of past references to “rules-based international order” or “international law”.

The first point to make is that the Trump administration gave us a clear road map of their strategy… and we shouldn’t question it.

This text box captures the main points published in the National Security Strategy (NSS) late last year. One analyst called this list “less of an announcement than an explanation “. The highlighted section at the bottom calls out a couple areas that double-down on using tariffs as a strategic tool, and the abandonment of text that was related to a “rules-based order”.

In the context of game theory, when one player is significantly dominant over the other player, then breaking the rule becomes the rule. For the U.S., economic and military dominance means that tariffs and other threats won’t leave their toolkit. The administration does not perceive reputational risk as material, relative to the payoffs of coercing trade deals or inward investment into the U.S. that aligns to its economic security strategy.

But, while we shouldn’t question this playbook, we still need to interpret it.

Tariff Instability To Remain A Theme in 2026

Boundaries do exist on how far you can push the rule breaking.

Case in point, last week’s Supreme Court decision was significant in setting limitations around use of IEEPA and executive power.

Importantly, however, the judgement was met with a cautious response globally, since it doesn’t alter the overarching intent and strategy of the Trump administration. Tariffs will remain a primary tool in redefining trade relationships, evidenced by the executive order citing alternative powers with sections 122 and 301 and section 232 remains a tool.

Even before the much-awaited decision, guardrails around the application of tariffs were becoming more evident.

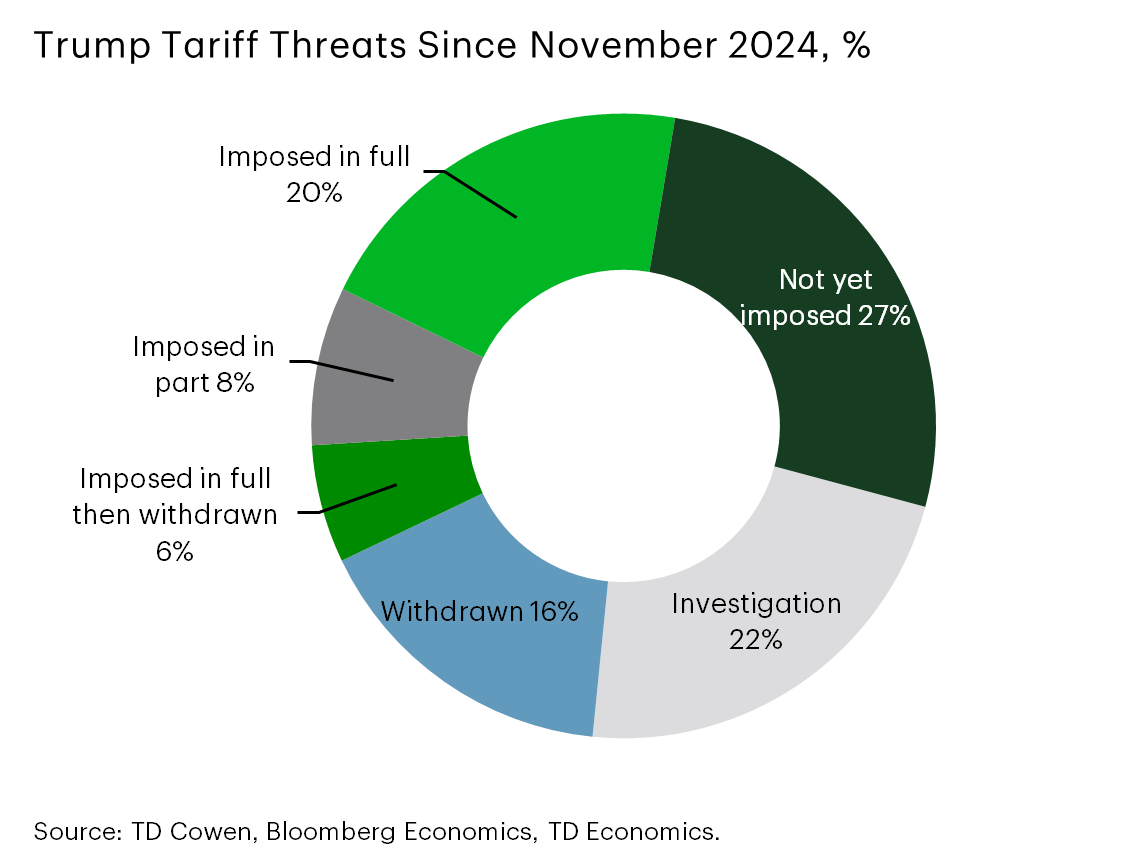

This schematic shows that only one-third of Trump’s tariff threats have turned into actual outcomes, which is captured on the left side. A key distinction of what turns a threat into a reality is the existence of an executive order, but even this isn’t a guarantee.

For instance, tariffs were scheduled to rise on wood products from 25% to 50% on January 1st of this year. This was pushed out to 2027, with the administration citing a desire to have more time to reach productive negotiations with trade partners. This explanation, however, reveals an important limitation on rule breaking. The administration is sensitive to any tariff that immediately impacts household affordability ahead of mid-term elections. In this case, wood product tariffs would directly hit prices on bathroom vanities, cabinetry and similar items.

Applying the same logic, Trump’s threat of tariffs on all Canadian goods was not realistic but was meaningful in defining the limits of a trade agreement Canada can reach with China. On the other hand, the threat of 50% tariffs on Canadian made aircraft had more credibility because it was targeted and does not immediately feed downstream to consumers.

So threats that are further upstream on manufacturers and wholesalers should be taken more seriously than on final consumer goods, at least in the near term.

- Only about 35% of Trump’s tariff threats have been imposed

- Need executive order to turn a threat into action.

- Any direct threat to household affordability becomes a policy restraint.

Trump Getting More Sensitive to Impacts on Consumers

But even this approach is not a hard-and-fast rule.

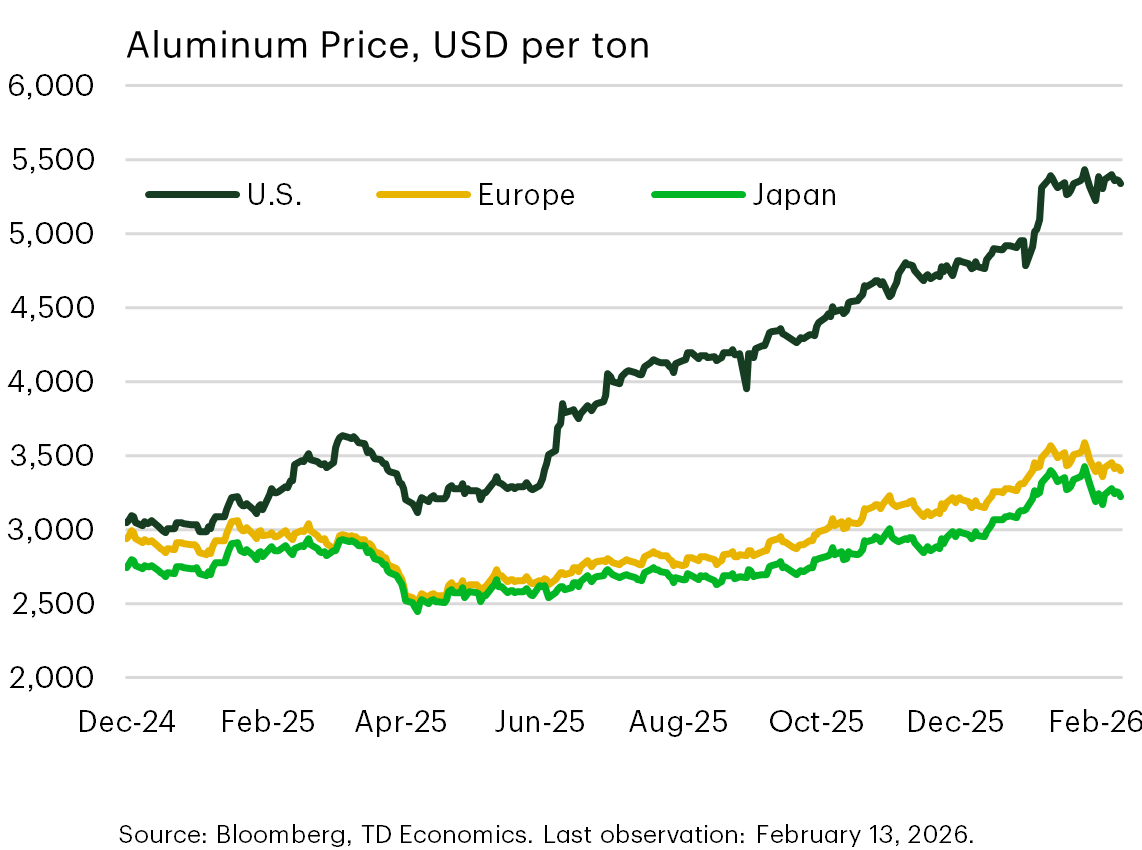

Recently, Trump commented that he was considering a reduction in tariffs on steel, aluminum and copper products. These all fall under section 232 tariffs that are as high as 50% and cover roughly 400 products due to successful lobbying efforts by domestic industry. This graph gives an example of how high raw U.S. aluminum prices are relative to international peers. This massive gap is truly anomalous because the global commodity market tends to be cohesive.

With the passage of time, it’s reasonable to expect companies to keep passing higher input costs to consumers, rather than absorb them, if they believe tariffs are part of the permanent landscape. And this is showing up in many consumer products, such as the aluminum cans in the packaging of food and drinks.

So here we have another example that rule-breaking has limits as the administration rethinks the blanket approach when consumer impacts are obvious. And this is an extension from action taken last year to remove tariffs on over 200 food products that were harming household affordability.

As an extra mention, Canadian producers and consumers stand to benefit from a rollback in U.S. policy because sourcing aluminum anywhere in North America has resulted in these high raw material prices, made worse by Canadian exporters facing another set of tariffs on the shipment of products into the U.S.

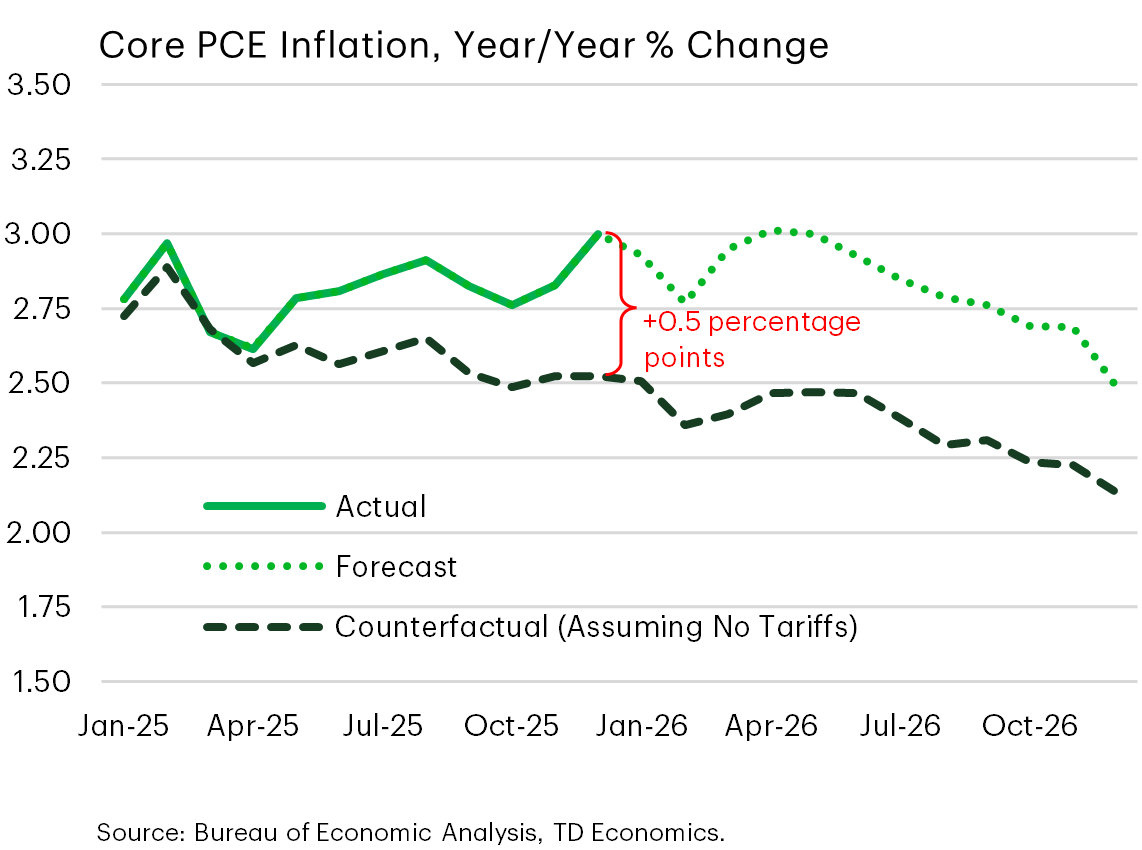

Tariff Pass-Through A Blemish on Inflation

Here’s the big picture we estimate is playing out on household prices from all the tariffs imposed.

This is the PCE deflator, which is the Fed’s focus for inflation rather than the CPI metric often cited by media. I’m demonstrating the gap in inflation between “actual” and the “counterfactual” that would exist absent tariffs. To date, passthrough has been relatively small, but is showing signs of picking up, which is partly why sensitivity is rising within the Trump administration.

January CPI data came in slightly below market expectations, causing markets to breathe a sigh of relief. But this masked the fact that prices on goods were weighed down by a single category – used vehicle prices. Removing this effect saw the price for core goods rise more than any other month in a year. This is an example that with the passage of time, the risk becomes amplified that we will see more price adjustments by retailers.

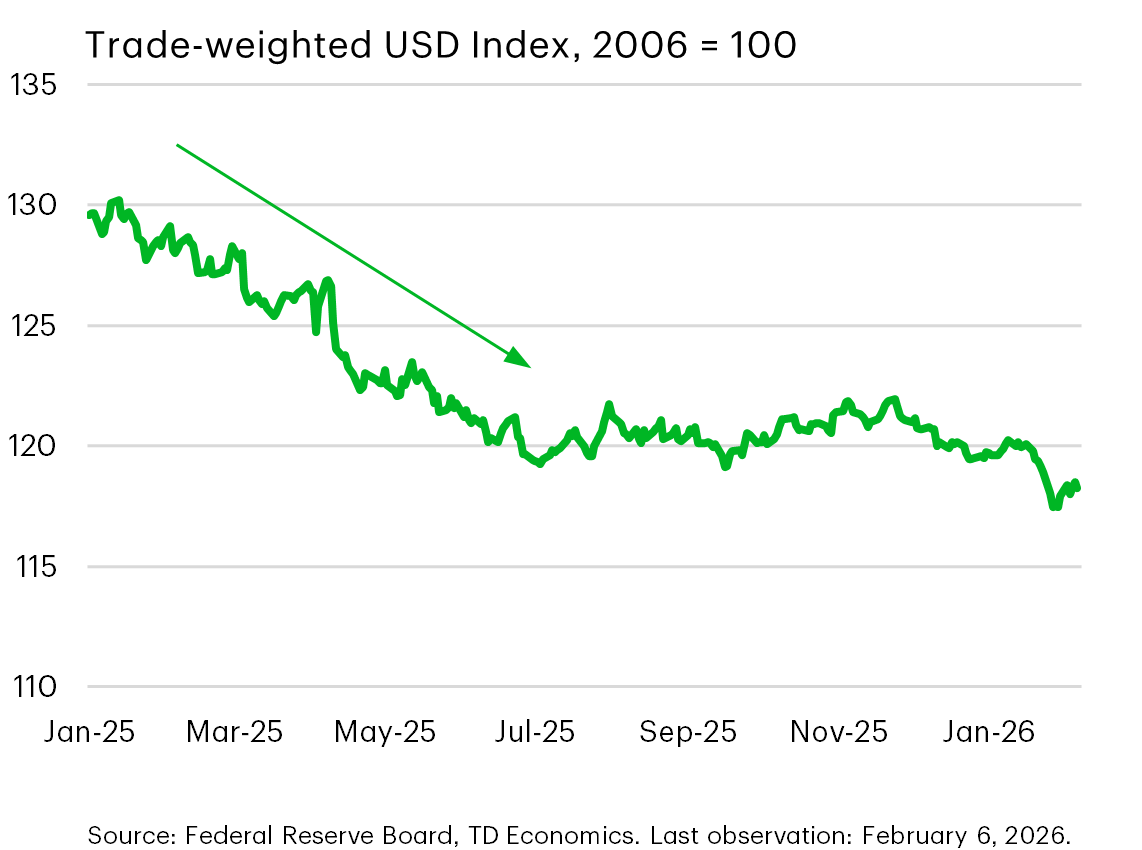

U.S. Dollar Plummets Alongside Yield Curve Repricing

The other rule-breaking restraint, and an effective one, is the market reaction to policy announcements.

One of the most asked client questions is related to understanding the decline of the U.S. dollar, and how much further it has to go. Last year, the trade weighted dollar fell 8%, followed by an additional 1 percentage point depreciation in the early days of this year.

Most of the dollar’s repricing happened in the first half of the year, related to “Liberation Day” tariffs, budget deficit concerns and worries around Fed independence. These concerns remain but are now known elements and another big leg down in the currency would likely require another set of unexpected geopolitical or domestic dynamics to materialize.

So we can bucket the market drivers into three groups:

- The first is safe-haven shifts, as investors diversifying away from the greenback. Benefactors have been the Euro, the Swiss Franc, Norwegian Krone, and gold also falls into this category.

- The second relates to “Fundamentals”, such as expectations on inflation and narrowing interest rate gaps relative to peers.

- And the third reflects other currencies boosted by the commodity cycle (especially metals), such as the Australian and South African dollars.

Significant shifts in any of these three categories would predict more aggressive repricing.

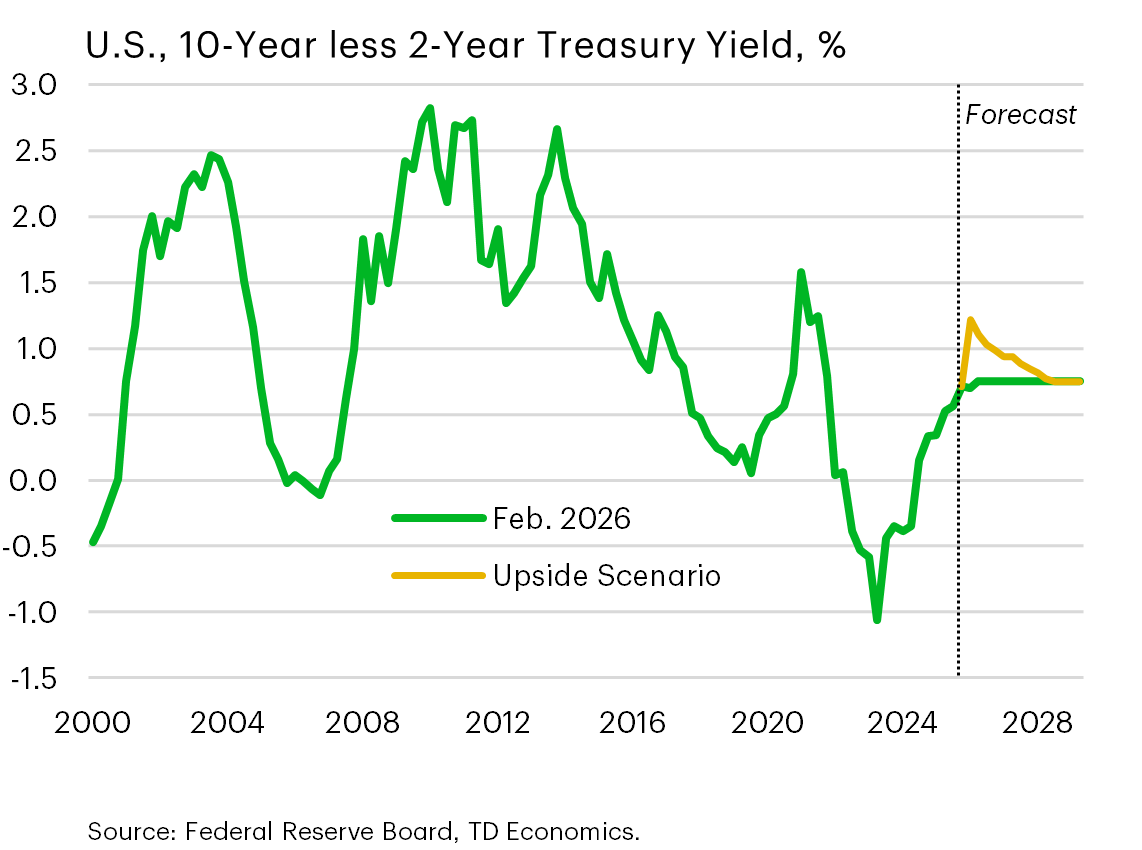

Returning to the notion that rule-breaking has boundaries, the administration welcomes some depreciation to improve export competitiveness but nothing that displays a loss of confidence or loss of market dominance, because it runs counter to their national security strategy. In addition, they must be mindful of the repricing along the yield curve, which has steepened alongside stubborn long-term yields.

The Upside Scenario in the 10-2 yield spread graph is based on how it behaved in the past during rate-cut cycles. There’s been a lot of market chatter on a higher risk premium at the long end of the curve. And when we see yield movements in isolation, they do look large. But when we pull back the historical lens, a term premium of 100 basis points would be considered normal in a rate-cut cycle, suggesting that even if there’s more spread widening, we shouldn’t naturally assume it’s related to a meaningful loss in investor confidence.

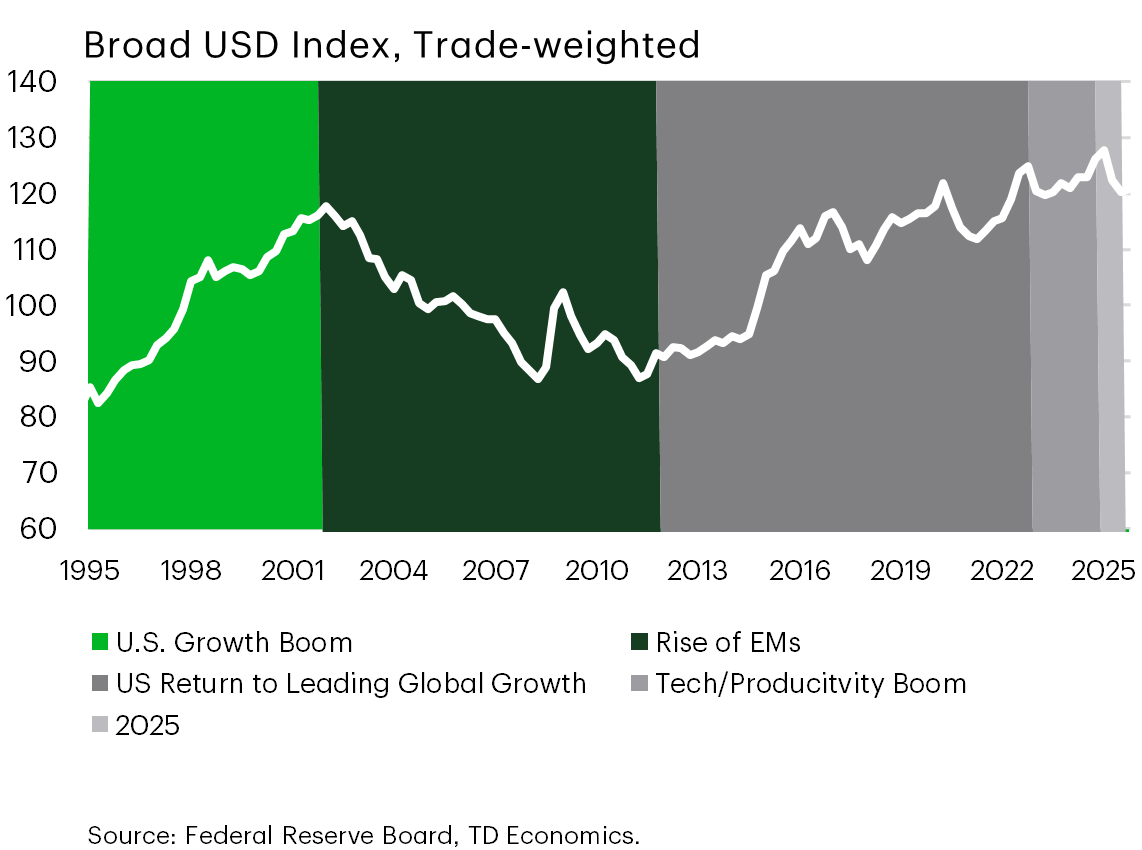

Context Matters on the U.S. Dollar

And to reinforce the importance of historical context, here’s the U.S. dollar back three decades that requires you to almost have to squint to see the depreciation that occurred last year.

This also shows a broader point that currency cycles are multi-year, shown by the color coding. When the momentum holds, it unfolds over years with shifts of 25% to 40%. There are similarities today to the Dot.com boom and bust which was when:

- the US economy was growing faster to peer countries

- U.S. equities were outperforming

- And the Federal Reserve was holding interest rates higher than peers

If this AI boom cycle turns into a bust cycle, this becomes an argument that U.S. dollar depreciation could be another 10% or more, if it mirrors that cycle. But the current movements are not yet alarming or unusual in this historical context.

Surprisingly, Nothing Shaking U.S. Economic Momentum

For now, nothing seems to be shaking the U.S. economic dynamics.

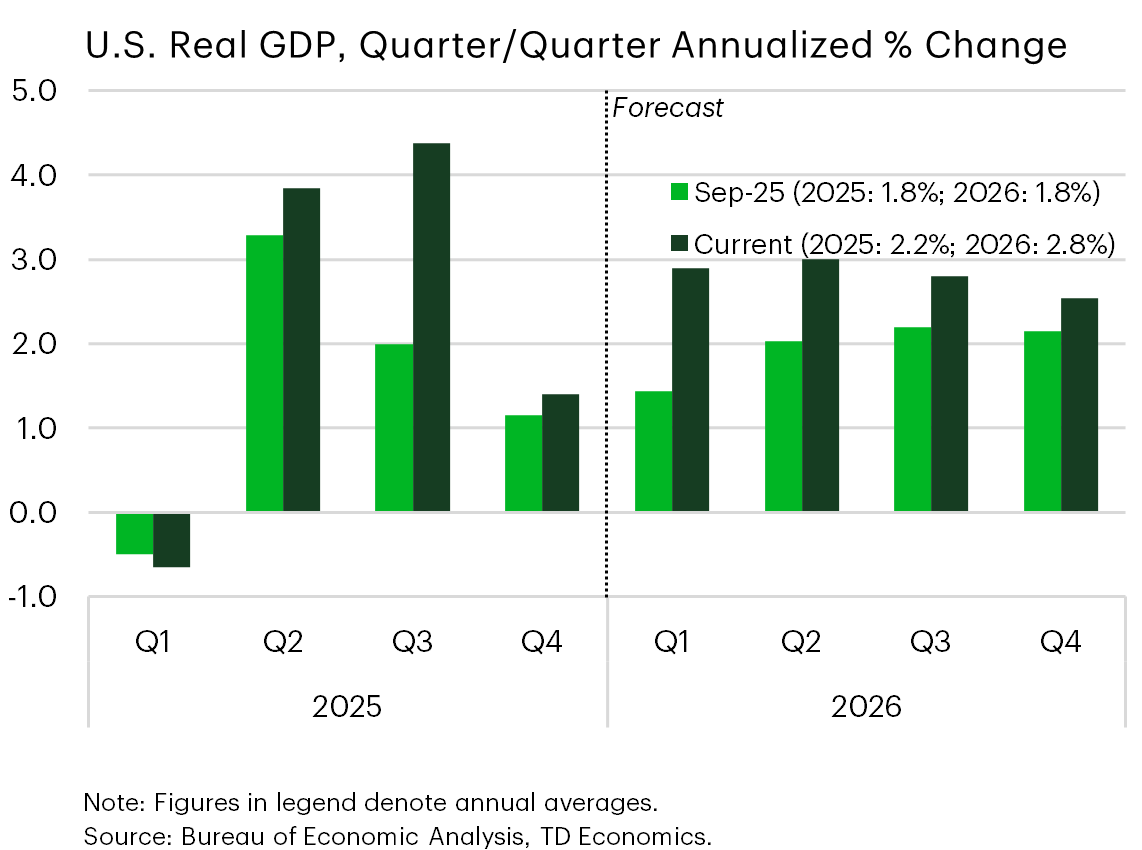

Since our forecast in September, there have been significant upward revisions to the U.S. outlook. The near-3% annual rate expected this year is impressive, and may seem surprising given last week’s fourth-quarter GDP estimate, which came in weaker than expected, at only 1.4%. But most of the undershoot reflected weaker government spending partly due to the shutdown. Stripping that impact away, economic growth came in at a solid 2.5%. Much of the temporary shutdown-related losses will reverse in the first quarter of 2026, leading us to upgrade our estimate closer to 3%.

The two catalysts behind this resilience are stronger AI investments and consumer spending. What’s most impressive is that this is occurring with heightened trade uncertainty and with a fed funds rate that was in restrictive territory for nearly the entirety of last year.

Reason 1: U.S. Dominates AI Investment

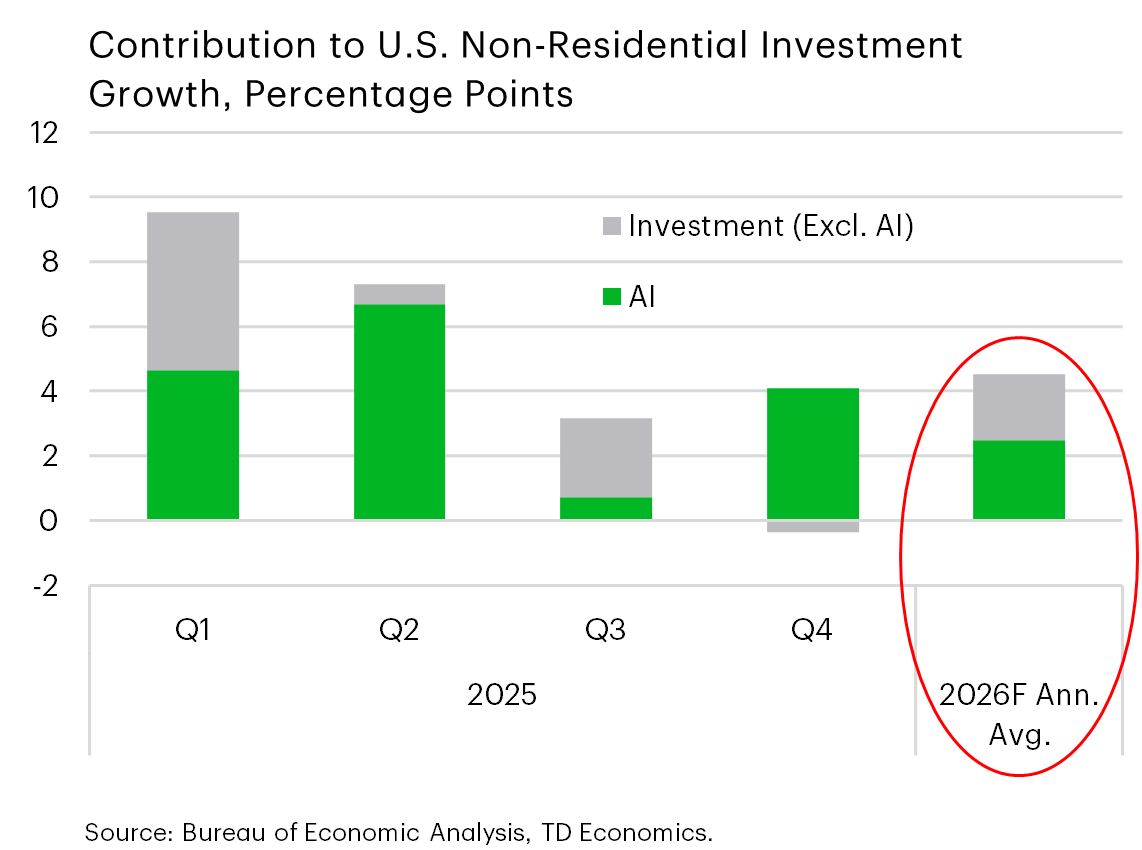

So, digging into the details, we’ve been telling this story for some time, but here it is again.

AI is dominating investment in the economy, but now it has a twist. This graph shows the contribution to total investment from AI versus all other types of business investment. AI continued to dominate the investment picture in the fourth quarter, but it appears only a matter of time before we see higher investment from other types of businesses.

As 2026 unfolds, this rotation of investment is embedded into our forecast as a theme, even with ongoing massive hyperscale capex from AI companies, which showed another 30% increase from last year. And that was from just 4 companies - Microsoft, Meta, Alphabet and Amazon.

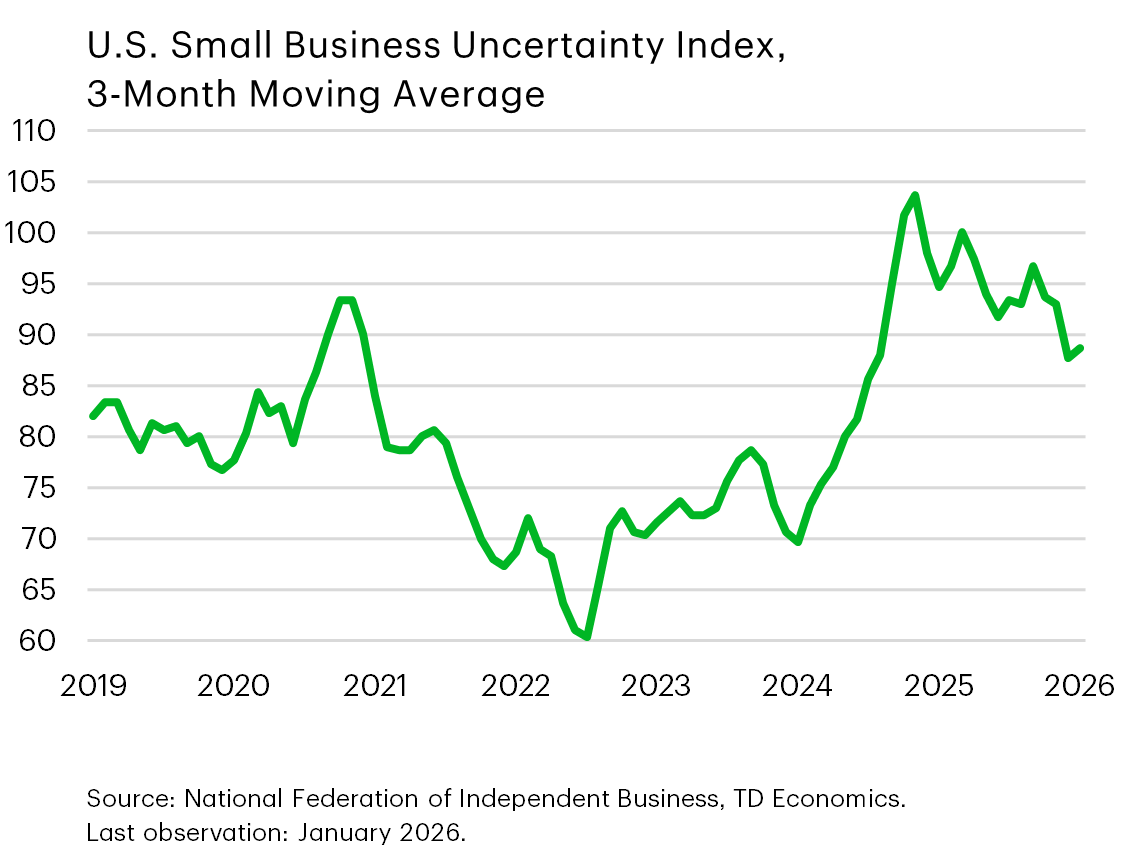

The second graph shows that there’s also a corresponding drop in business uncertainty, even though it remains historically high. We suspect businesses have sat on the sidelines too long and are now learning to navigate through uncertainty. This is substantiated by a Federal Reserve survey that showed an increase in C&I loan demand by small and medium sized businesses, which shot to its highest level since the onset of the tightening cycle.

And then let’s not forget there will also be an investment impulse coming from the OBBB that changed several business provisions including full bonus depreciation on equipment, full expensing for research & development costs, and temporary expensing for manufacturing structures.

Reason 2: U.S. Consumer Spending Proves Resilient

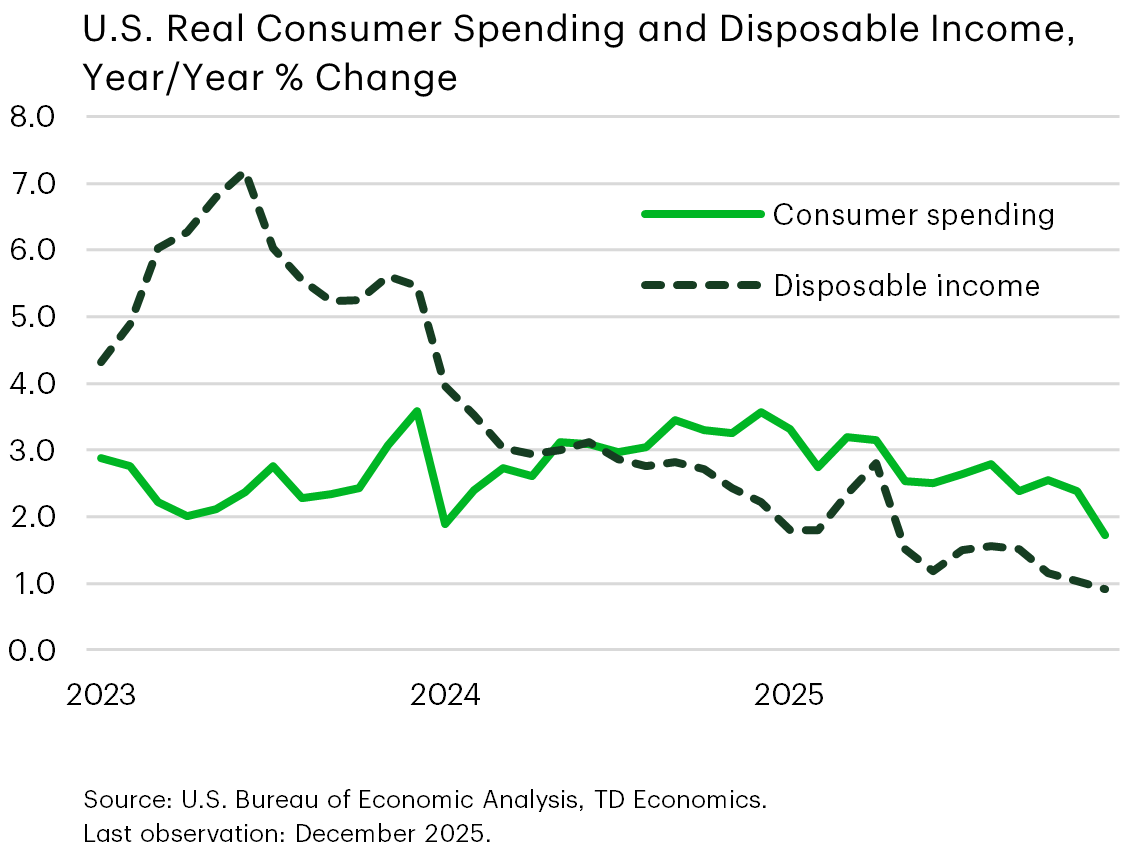

Turning to the other growth-catalyst, it came from a resilient consumer in the second half of 2025 despite weakening after-tax income fundamentals.

This would normally lead us to question its sustainability in 2026, but the income picture is about to get a big boost…

Fiscal Tailwinds Should Sustain Consumer Momentum in 2026

There are two fiscal tailwinds about to hit household pockets from tax changes in the OBBB.

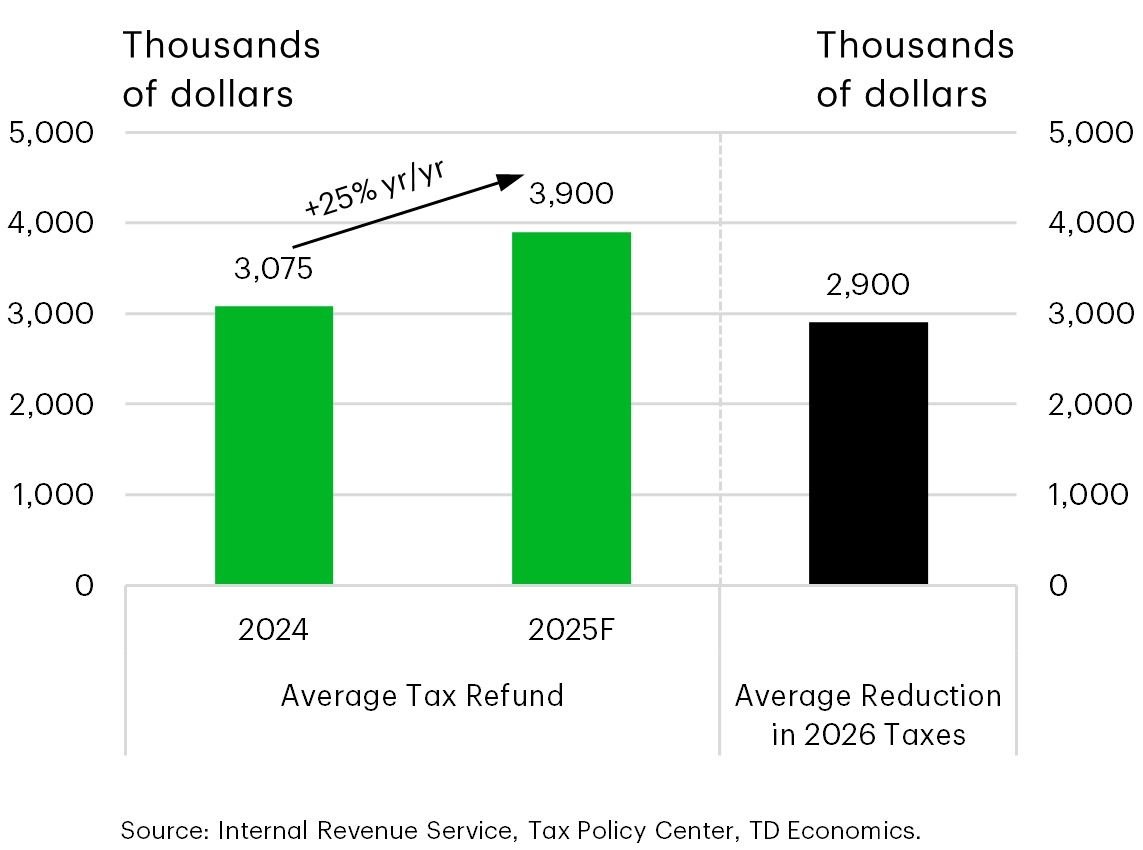

The first is larger tax refunds, which were retroactive through 2025, hitting bank accounts this quarter and next. Because the IRS didn’t update its withholding tables until this year, many will benefit from refunds that will average roughly $900 more per tax-filer relative to last year. The second benefit is on the right side of the graph, showing higher tax-home pay from tax cuts.

The combined effect is expected to lift after-tax incomes by over $200 billion this year. And even though tax breaks skew to higher income households, applying conservative economic multipliers still causes a lift in nationwide consumer spending by several tenths of a percentage point.

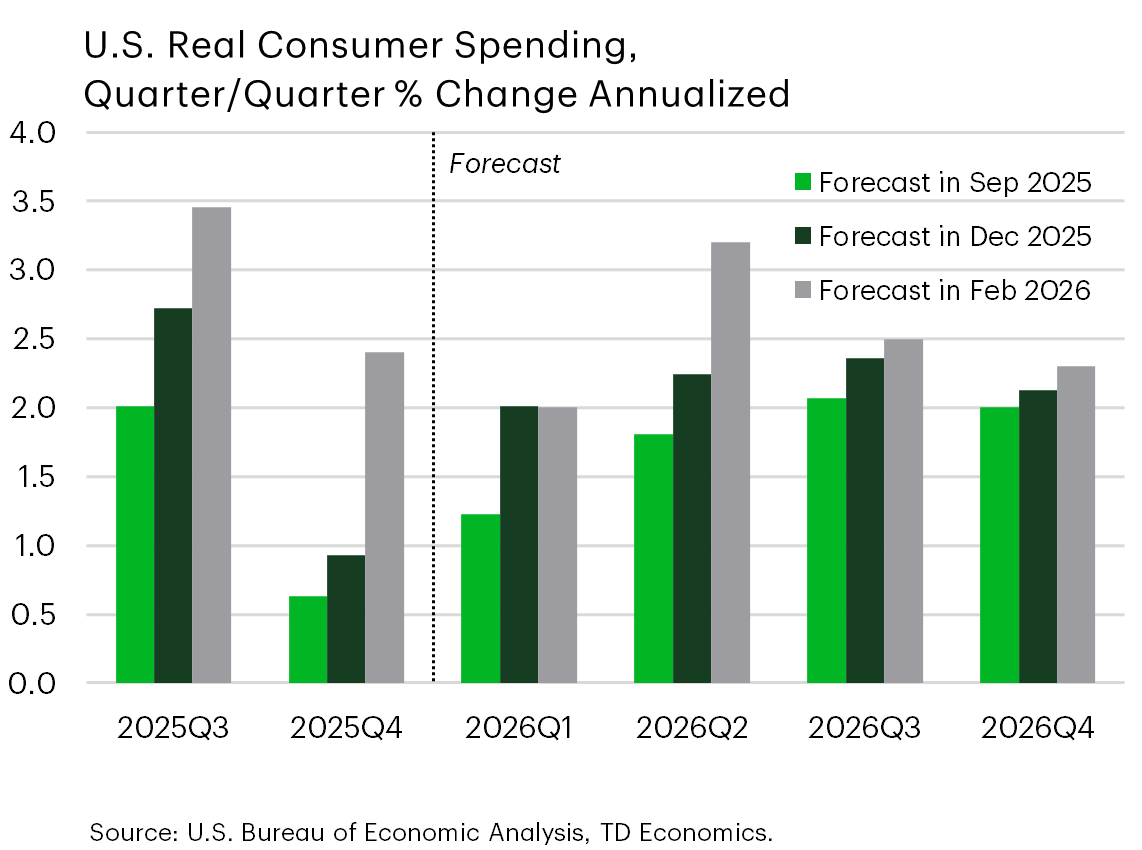

Chasing the Forecast

And this is the net result, which I call “chasing a forecast” because we’re getting the direction right, but not the magnitude. Ultimately, households dug into their savings more than expected in the second half of 2025, which helped to power solid consumer spending gains despite the impact of the record long government shutdown. Real consumer spending expectations now sit at 2 1/2% in 2026, relative to our December forecast, which reflected a more trend-like 2%.

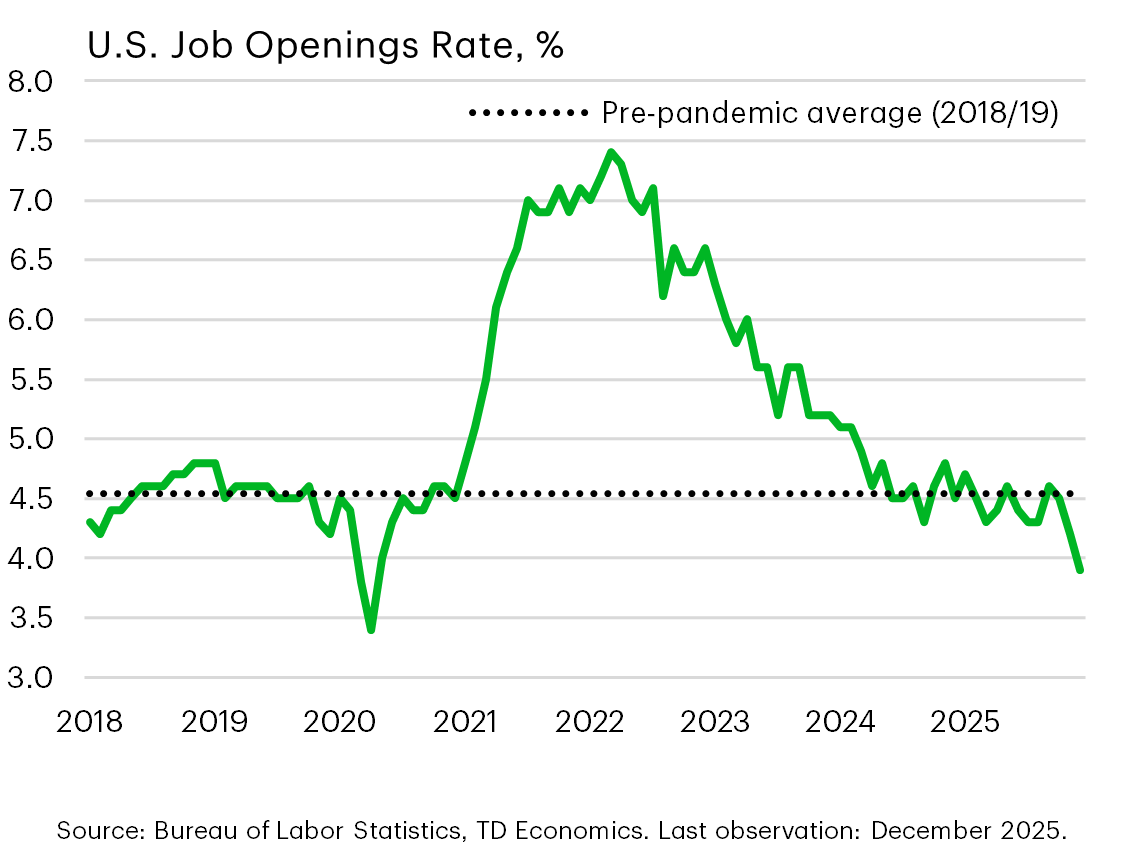

Soft Spots Exist: Cooling U.S. Labor Demand

Now it’s not all sunshine and rainbows. I couldn’t respect myself as an economist if I didn’t deliver some words of caution or bad news.

Starting with the good. January jobs data were double market consensus at 130,000 new positions, with an unemployment rate that ticked down to 4.3%. That’s all good. But it’s superficial to leave it there.

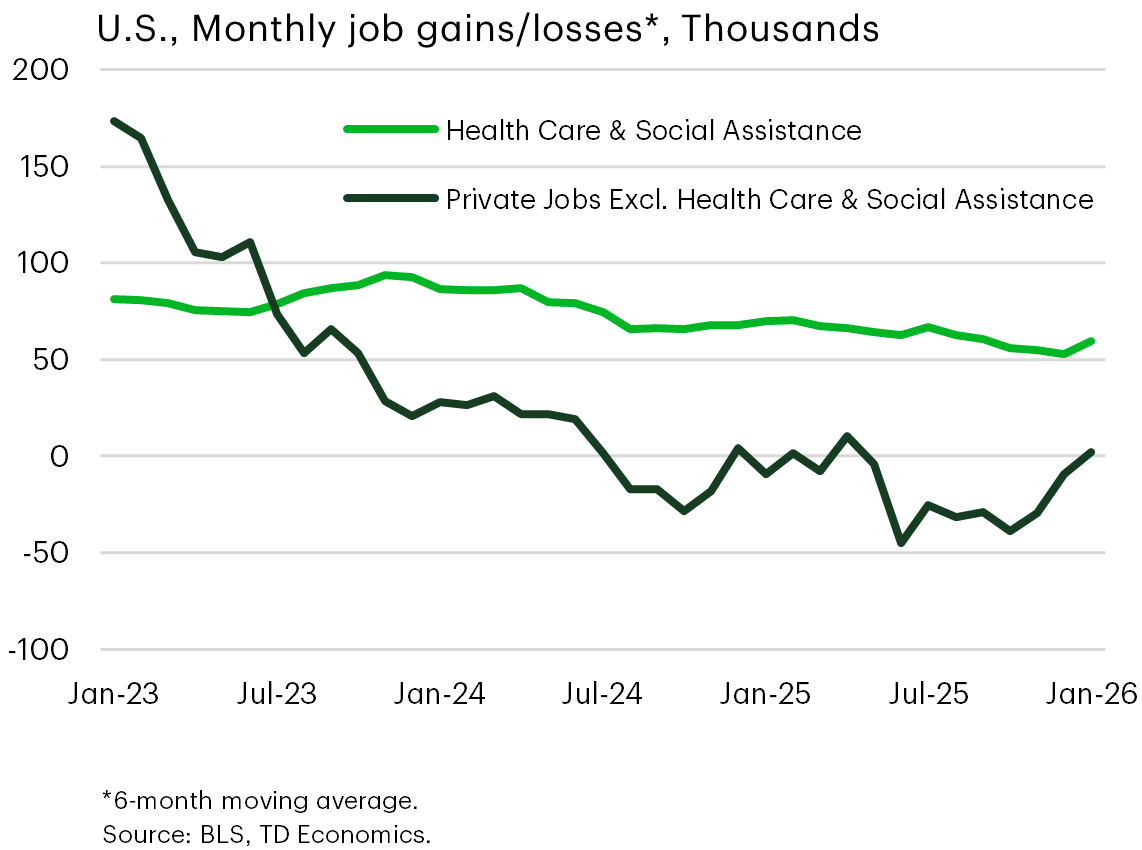

A collapse in job openings suggests the prospect for more big surprises is limited unless this turns around. And, when we look under the hood of that January jobs report, it reveals demand is largely centered in a single sector – health and social assistance. This long-standing theme is now starting to get challenged, with is shown by the uptrend in the dark line, but it needs to be substantiated with more time and conviction.

Summary

For the U.S., it’s steady as she goes. The economy has a good underbelly on a combination of investment and consumer spending, with a tax tailwind coming in. The inflation outlook risks upside in the near term if further tariff pass-through occurs. But since Trump is doing a course correction in some areas, this helps build the case for two more rate cuts once Kevin Warsh is in seat as the Chair, presuming his appointment is approved by mid-year.

In a nutshell, our U.S. rate view hasn’t changed from last quarter and, so far, is broadly consistent with market pricing.

DisclaimerThis report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share this: