Provincial Housing Outlook:

Housing on Shaky Foundation Amid Tariff Turbulence

Rishi Sondhi, Economist | 416-983-8806

Date Published: March 26, 2025

Highlights

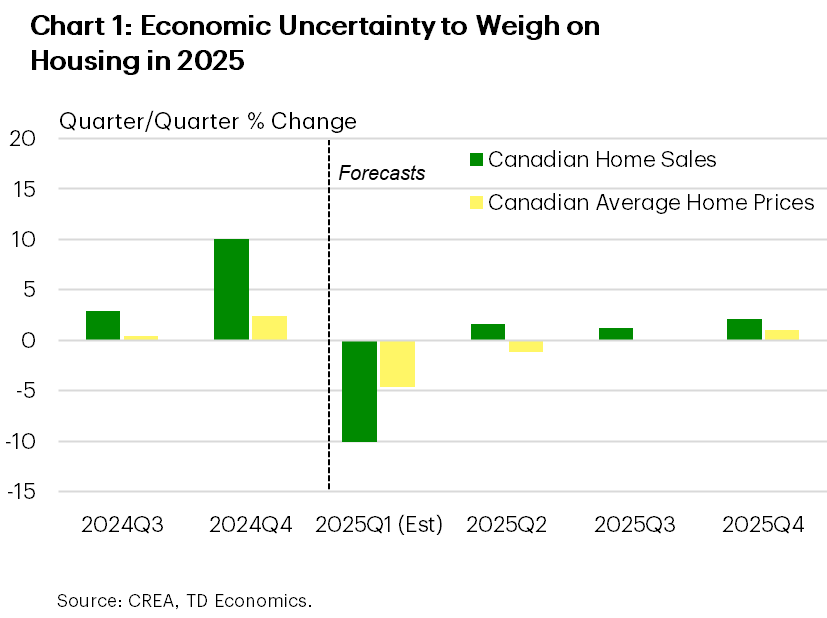

- The one-two punch of winter storms and tariff-related economic uncertainty sent a chill through Canadian housing markets in the first quarter. We’re now tracking a double-digit quarterly decline in Canadian home sales and a mid-single digit drop in Canadian average home prices. These outcomes are much weaker than our pre-Trump inauguration forecast made in December, where we assumed that a loosening in federal mortgage rules, lower interest rates and continued economic growth would fuel a modest Q1 gain in sales and prices.

- This much softer starting point has us led to materially mark down our 2025 annual average growth forecasts for Canadian home sales and prices. Moving forward, its unlikely that activity will be as weak as it was in the first quarter. However, we still think that elevated uncertainty and a deteriorating jobs market will yield subdued sales and price growth for much of 2025 (Chart 1).

- 2025 home price forecasts have been cut the most in B.C. and Ontario, where we now think that prices will decline in annual average terms this year. This reflects muted demand conditions in both markets and supply/demand balances that are heavily skewed in the favour of buyers. Of note, the GTA condo market is particularly soft, which will weigh on prices in Ontario this year. Elsewhere, 2025 quarterly price growth forecasts have been marked down to sub-trend levels in other parts of the country. We’re retaining our view that quarterly price gains will outperform in the Prairies moving forward given relatively tight supply/demand balances and comparatively better affordability.

- An improving backdrop should set the stage for a notable rebound in home sales and average home prices in 2026. Specially, hiring should improve as we’re assuming a dialing back in tariff-related uncertainty (see our updated Quarterly Economic Forecast for tariff assumptions underpinning our economic projections). At the same time, interest rates should be at multi-year lows. These factors will facilitate the release of significant pent-up demand. However, the scale of bounce-back in Canadian average home prices will likely be restrained by poor affordability in key markets like B.C. and Ontario.

Forecast Table |

|---|

| Home Sales and Price Outlook |

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: