Data Centers in a Grid Constrained World: Challenges and Opportunities for Canada

Likeleli Seitlheko, Economist

Date Published: March 23, 2026

- Category:

- Canada

- Future Ready Economy

Highlights

- The AI revolution is fueling a surge in data center development, with the U.S. and China leading global capacity growth and reaping significant economic rewards.

- While Canada is eager to attract more data center investment and bridge its computational infrastructure gap, grid constraints pose a challenge to accommodating large-scale data center development in the near term.

- However, as many regions also have limited grid capacity, Canada can position itself as a competitive location longer term if it can figure out how to connect new data centers to power in a timely manner.

- At the same time, it will be important to ensure that the costs of integrating new data center loads are borne by the industry while keeping electricity prices affordable for ratepayers to maintain public support.

The rapid growth of cloud computing, artificial intelligence (AI) and other digital services is driving rising demand for data centers. Global installed data center capacity has increased significantly in recent years though development is largely concentrated in the U.S. and China. The U.S. economy has benefited considerably from the investment boom in data centers and other AI-related activities, which accounted for approximately three-quarters of business investment growth in 2025. In addition, the sector has created thousands of jobs and generated sizeable tax revenues for local governments in primary markets like North Virginia. The rise of AI is also spurring innovation in many industries and holds the promise of improving productivity. With capital expenditure on AI and data centers expected to reach trillions of dollars over the next several years, many countries are vying to get a share of that investment.

In recent years, governments in Canada have expressed a desire to boost investment in AI data centers in the hope of gaining some of the economic benefits and to address the country’s computational infrastructure gap. Data center developers have also shown interest in locating facilities in Canada as currently evidenced by the volume of projects that have applied to be connected to the Alberta grid. As well, earlier initiatives by Quebec and British Columbia to attract large electricity users saw data center companies respond with overwhelming enthusiasm, quickly utilizing all available capacity and ultimately leading to the programs being discontinued.

Despite the aligned interests of government and industry, it is going to be difficult to accommodate large data center capacity due to limited electricity generation and transmission capacity. This scenario is currently playing out in Alberta where the system operator has said the provincial grid can reliably integrate just a tiny fraction of the total data center load requested in the near term. Other parts of the country including Quebec, British Columbia and Ontario are also not in a position to accommodate large increases in load based on current electricity grid capacity.

However, this does not mean that Canada should count itself out of the global competition to get a share of the growing capital investment in data centers as many countries are also struggling with similar grid capacity constraints. Longer term, regions that will do better will be those that can adapt their electricity sectors to be able to connect projects to power supply in a timely manner (be it on grid, off-grid or both). Canadian governments should learn from the experiences of jurisdictions in the U.S. where data centers are contributing to rising retail electricity prices. Ensuring that the costs of integrating new data center loads are borne by the industry will be important for getting public support.

Canadian governments aiming to expand data center infrastructure

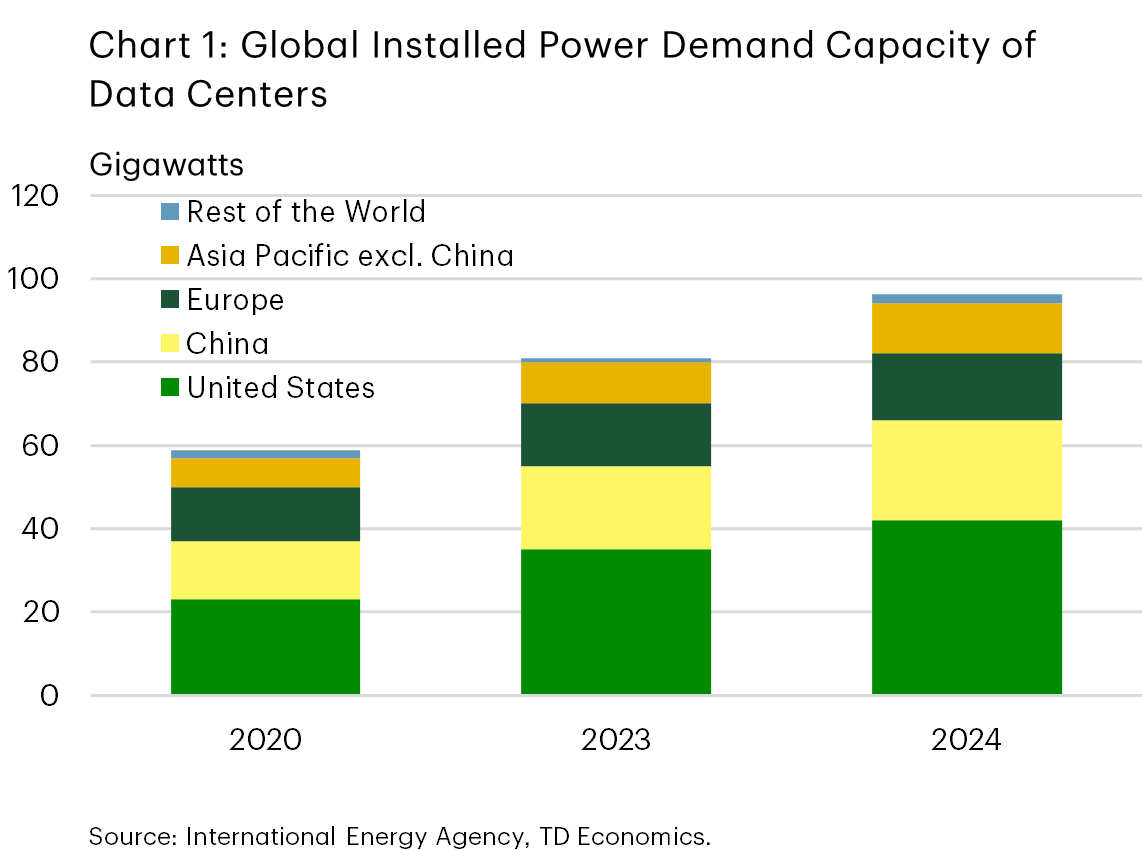

Global installed power demand capacity of data centers grew by over 60% from 60 gigawatts (GW) in 2020 to approximately 100 GW in 2024. However, the capacity build-out was concentrated in the U.S. and China, which accounted for about half and over a quarter of the increase, respectively (chart 1).

Virtually all of the installed capacity in North America is located in the U.S. and its economy has reaped significant benefits from the recent expansion in capital investment in data centers and associated industries. Capital expenditures on AI-related activities contributed nearly three-quarters of the growth in business investment in 2025. No state has gained more from this boom than Virginia, which has the most mature data center market in the U.S. It is estimated that the data center industry contributes US$9.1 billion to state GDP and supports about 74,000 jobs annually, with most of the benefits coming from construction activities.1 Some Virginia counties with mature data center markets are also generating large tax revenues from the industry. For example, Loudoun County received US$895 million in tax revenue in FY2025, almost enough to fully fund the county’s operating budget of US$940 million.2

Although Canada has witnessed investment in data centers in recent years, the scale of development has been considerably smaller than in the U.S., resulting in more modest economic benefits. With global cumulative capital investment in data centers projected to reach US$7 trillion between 2025 and 2030,3 Canadian governments are eager to secure a greater share of this massive investment and its accompanying benefits. Alberta, for example, has introduced an AI Data Centers Strategy to position the province as a leading destination for data center investment in North America and has an unofficial goal of C$100 billion worth of AI data centers under development by 2030.4 At the federal level, the Canadian Sovereign AI Compute Strategy aims to enhance the country’s computing infrastructure to support the growth of the domestic AI industry and adoption of AI across the economy. The strategy was allocated up to C$2 billion in the federal Budget 2024 out of which up to C$700 million is aimed at mobilizing private sector investment in new or expanded data centers.5

Insufficient grid capacity could hinder immediate development plans

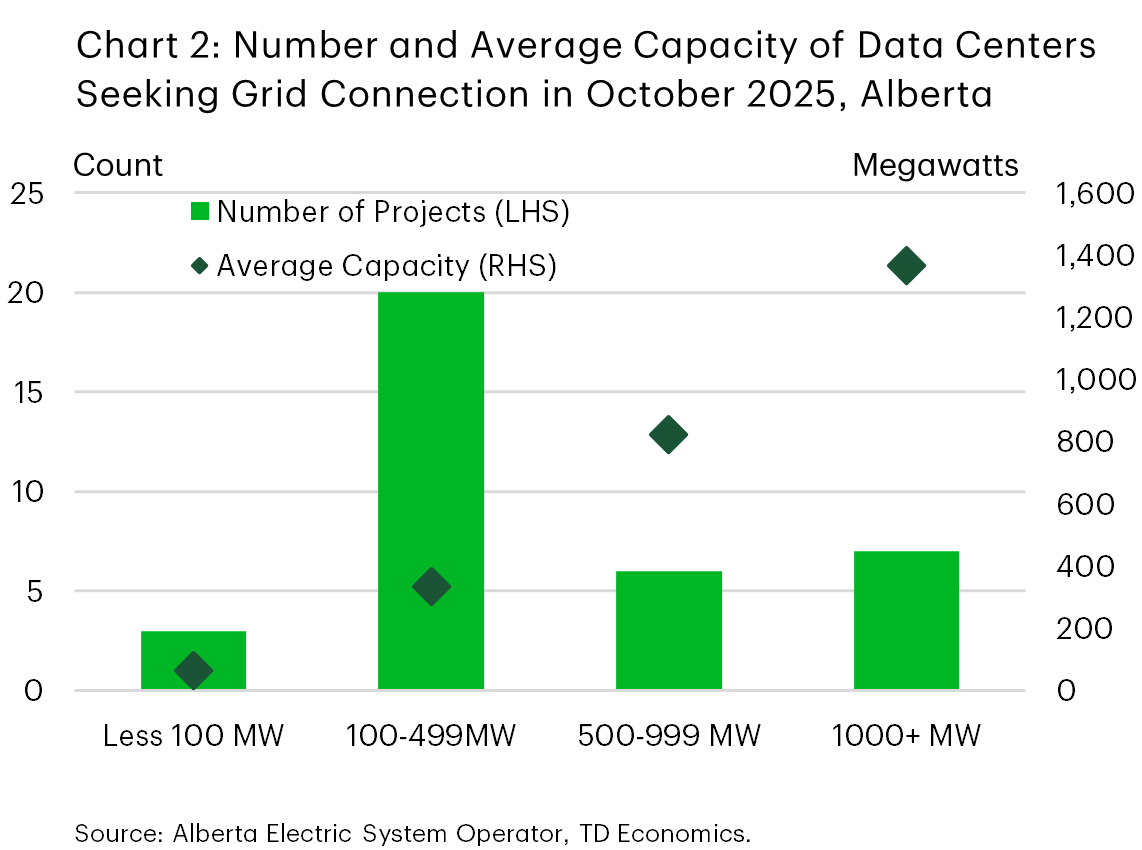

As Canada strives to attract more global data center investment and strengthen its AI sector, issues related to grid capacity are emerging as a critical factor that could shape the pace and scale of development. Prior to the age of cloud computing, streaming services and AI, an average traditional data center had power demand of less than 50 megawatts (MW). In contrast, AI data centers use a lot of power. Based on the demand capacities of many of the proposed projects, for example in Alberta, a facility with a power draw of 100 MW is on the small side while some of the large facilities use as much power as a small city (chart 2).

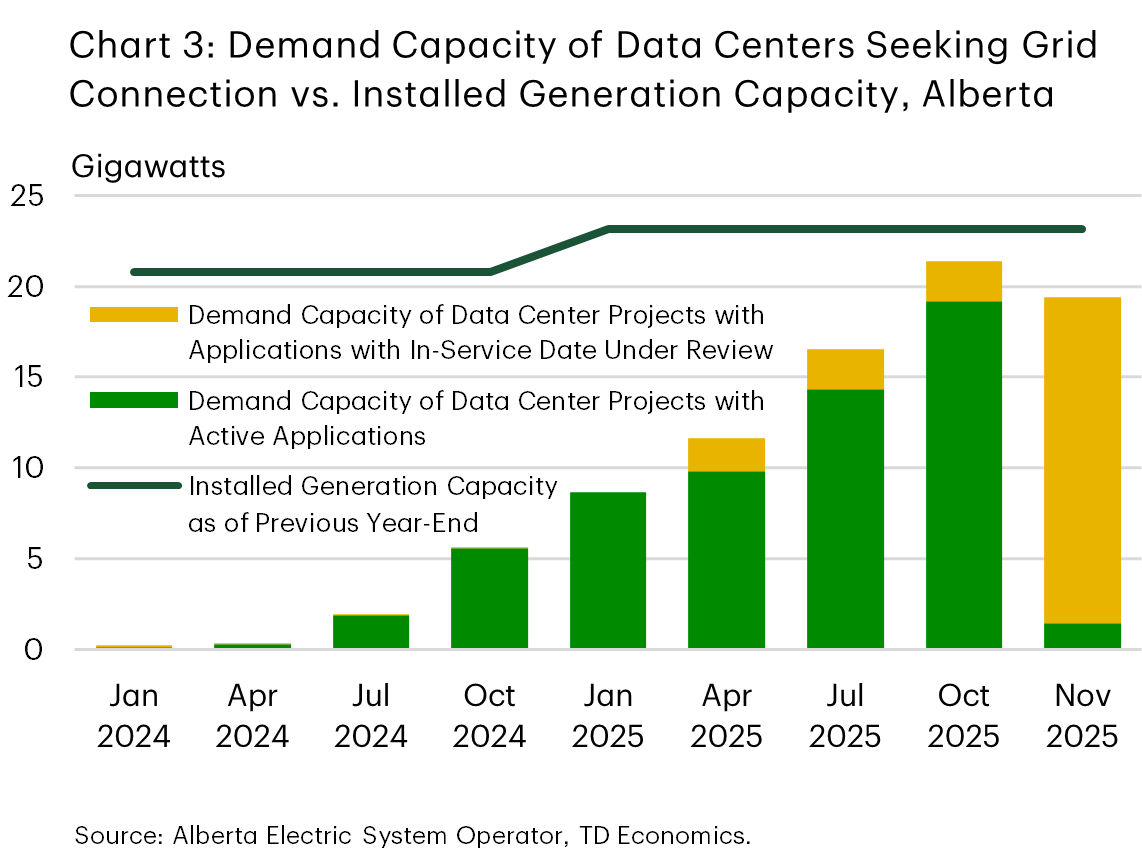

The recent experience of the Alberta Electric System Operator (AESO) with transmission grid connection requests from AI data centers highlights the challenge of connecting these power-hungry facilities to the grid. Over the past two years, the number of data center projects seeking to connect to the Alberta grid rose to more than 30 in the second half of 2025, up from just 2 in January 2024. What was even more notable though was the combined demand capacity of these projects, which reached as high as 21 GW in October 2025, with developers requesting to have around 90% of the new load online by 2030. For context, the proposed new data center load is over 60% greater than Alberta’s current peak demand of 12.8 GW (set December 2025). Moreover, with installed electricity generation capacity at about 23 GW (as of 2024), the proposed data center load would still be too much even if it was the only load running on the provincial grid.

In a sign of the slow pace of development that can be expected, the AESO has announced that it can connect just 1.2 GW of new data center load by 2028 without affecting grid reliability. This available capacity was allocated to two projects, out of the 36 that had active applications in October 2025, with the rest of the applications now temporarily paused while AESO consults with stakeholders to figure out solutions for the issue (chart 3). While 1.2 GW may not seem like a lot in the context of overall demand from data center developers, it is almost like adding another City of Edmonton (population 1.2M) to the grid in 3 years or so, which would be no mean feat!

Outside Alberta, there is unlikely to be a huge growth in data center capacity in other provinces. For instance, among the large provinces, Quebec has instituted restrictions on new power procurement for large data center projects due to grid constraints, which has put a halt on new development since 2024.6 A recent update from Hydro-Québec on 13 high-demand industrial sites indicates that nearly all of them have limited remaining transmission capacity and would need network reinforcements to connect new large projects.7 Similarly in Ontario, the areas that data center projects want to connect to require transmission infrastructure upgrades.8 British Columbia, on the other hand, has announced that it is going to prioritize the natural resources sector when granting access to the grid while new AI and data center projects will be allocated just 400 MW over the next two years.9

Other regions also facing grid capacity constraints

Grid constraint issues are not unique to Canada as many regions are also dealing with connection delays. The problem is most acute in markets that were at the forefront of data center development over the past decade. Among the worst affected places is Dublin, Ireland where there had been a moratorium on new data center grid connection since 2021 that was only recently lifted but with the caveat that facilities have to generate their own electricity.10 Elsewhere in Europe, developers also face long timelines in the Netherlands (up to 10 years), Germany (up to 7 years) and the U.K. (5-7 years). In the U.S., new data center projects spend up to 7 years waiting to connect to the grid in Virginia and around 3 years in California.11

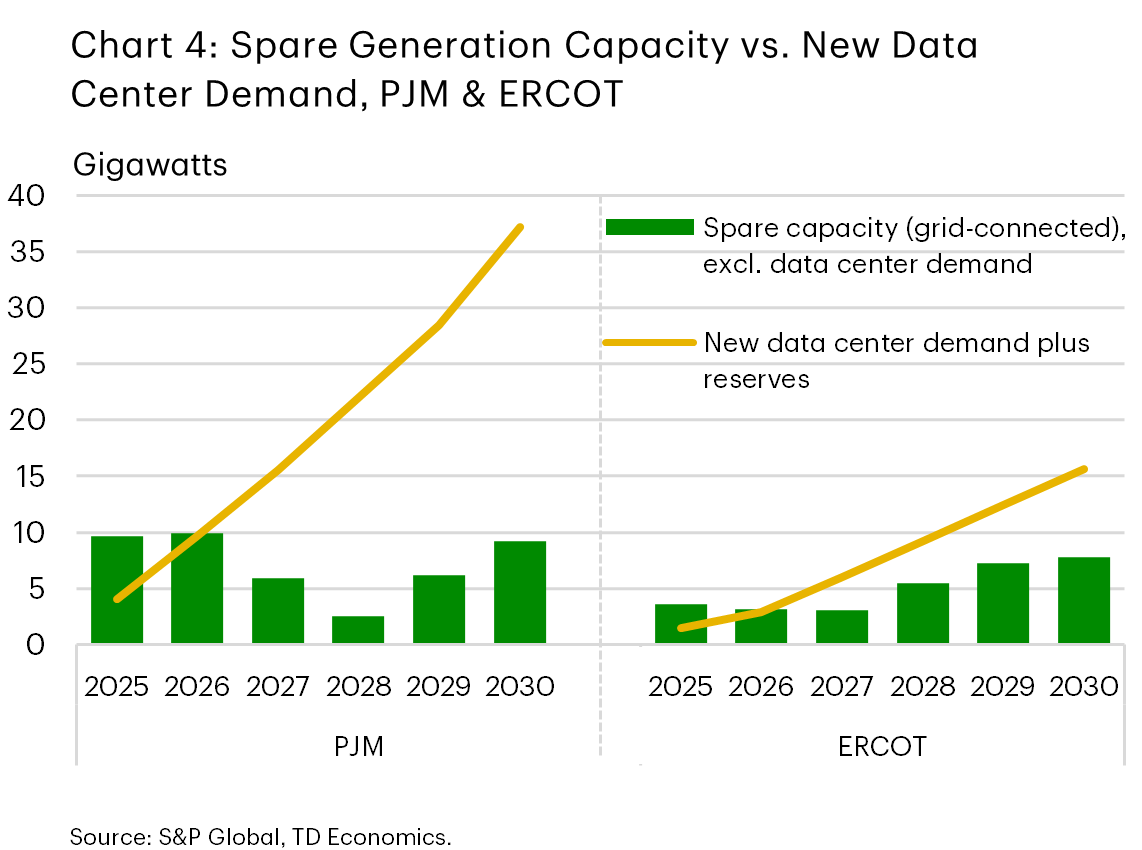

Globally, as in Canada, one of the factors driving long wait times for grid connection is the mismatch between the large amount of proposed data center capacity versus available power supply and transmission capacity. This is exemplified by the Electric Reliability Council of Texas (ERCOT), the grid operator for most of Texas, and the PJM Interconnection market, which covers 13 mid-Atlantic and Midwest U.S. states, including Virginia, as well as the District of Columbia (DC). In both electricity markets, spare generation capacity is insufficient to meet expected power demand from data center projects, and the shortfall is expected to get worse over the next few years (chart 4).

Concerns about data center impact on electricity prices causing backlash

While finding ways to resolve power access issues will be important in making Canada a more competitive location, policymakers should be mindful to avoid the experiences of some of the U.S. states where data centers are linked to rising residential electricity prices. In Q2 2025, around US$98B worth of data center projects were delayed or blocked in the U.S. due to opposition from local communities.12 Reasons vary, but the most prominent issue of late has been public concern that data centers are driving the increase in electricity prices and could lead to unaffordable energy prices as development ramps up even more.

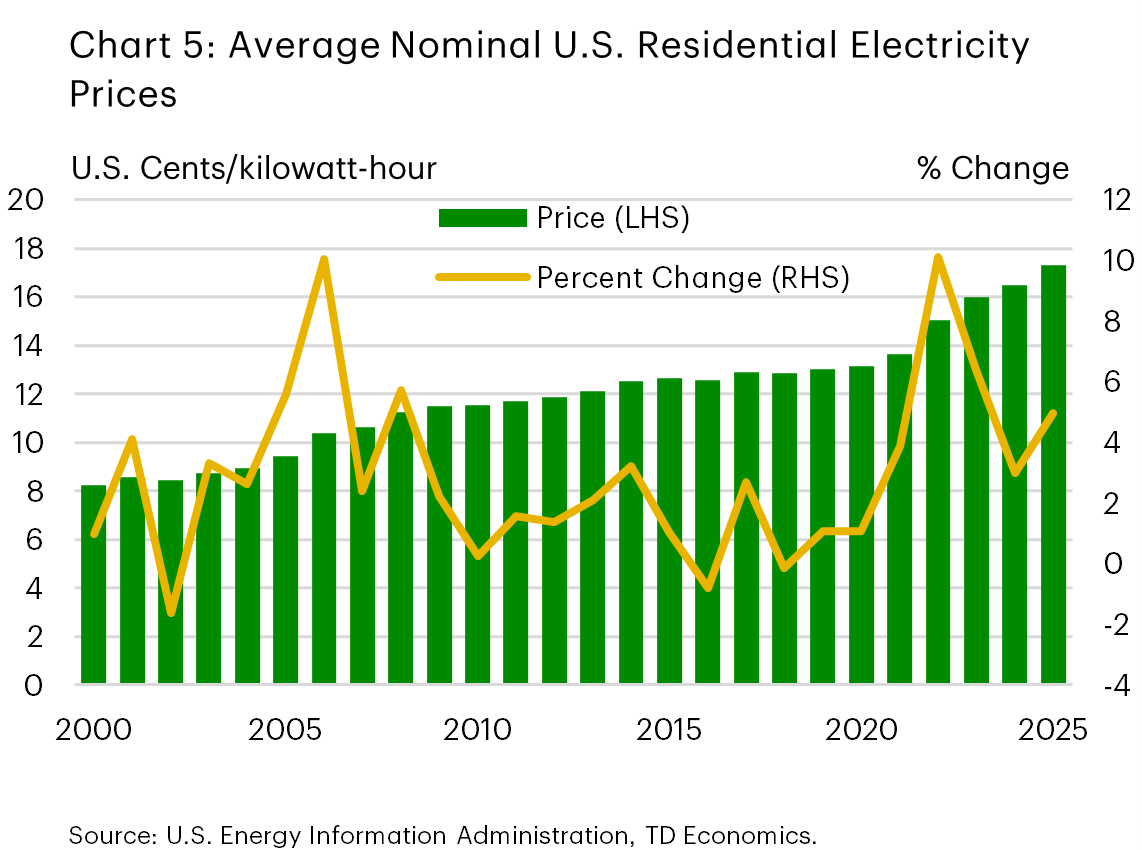

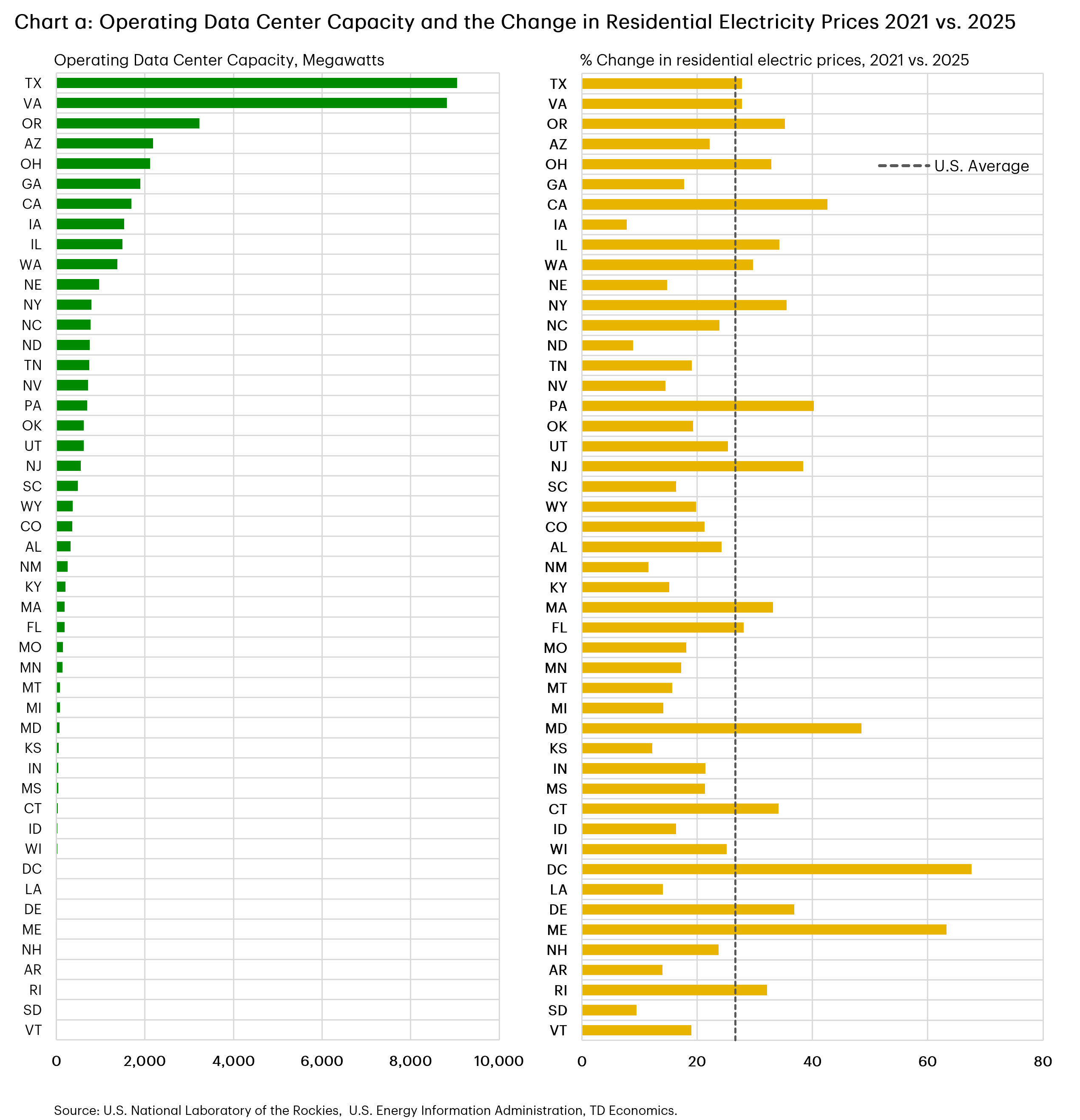

Indeed, average U.S. residential prices have been rising more rapidly in recent years compared to the decade before the pandemic (chart 5). Additionally, there is emerging evidence that rising load growth from data centers is contributing to the increase in retail prices in some regions though the story is complex. There are other factors also in play, like constrained natural gas pipeline capacity in the Northeast, that contributed to rapid growth in electricity prices in states that have little data center capacity (see chart a in appendix).

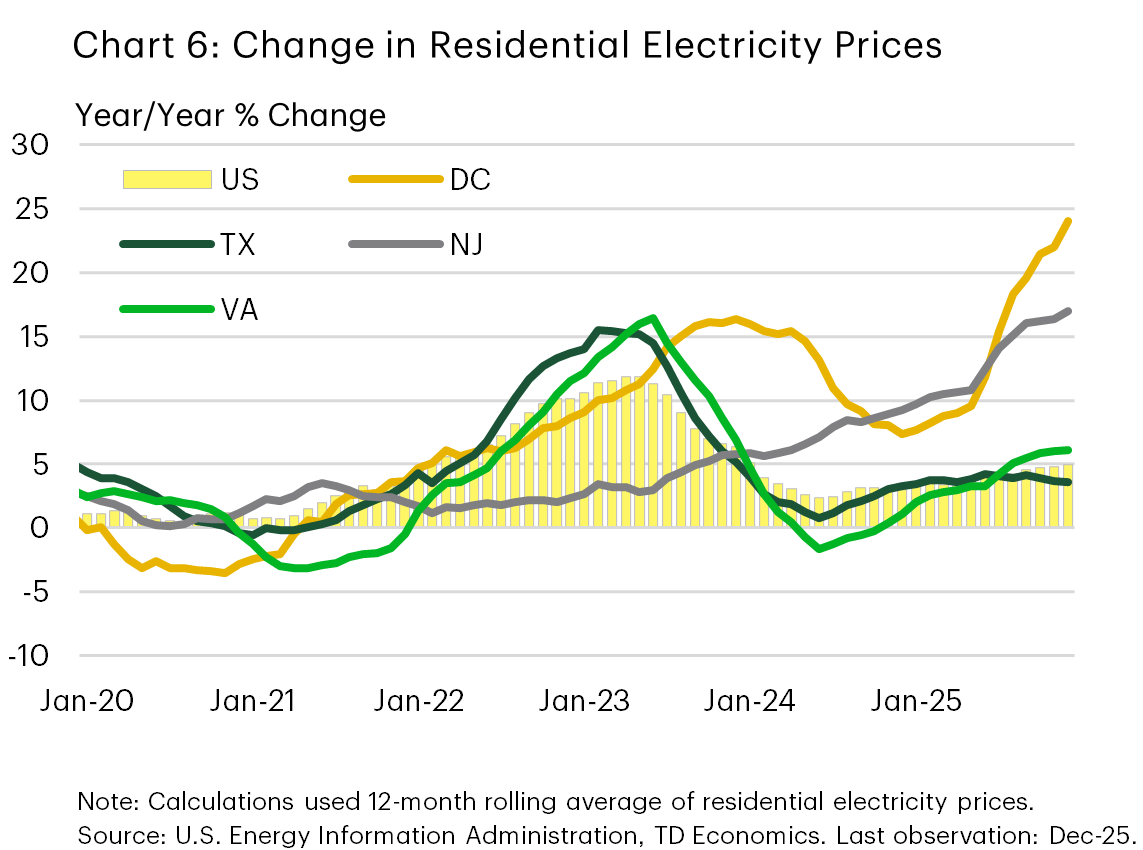

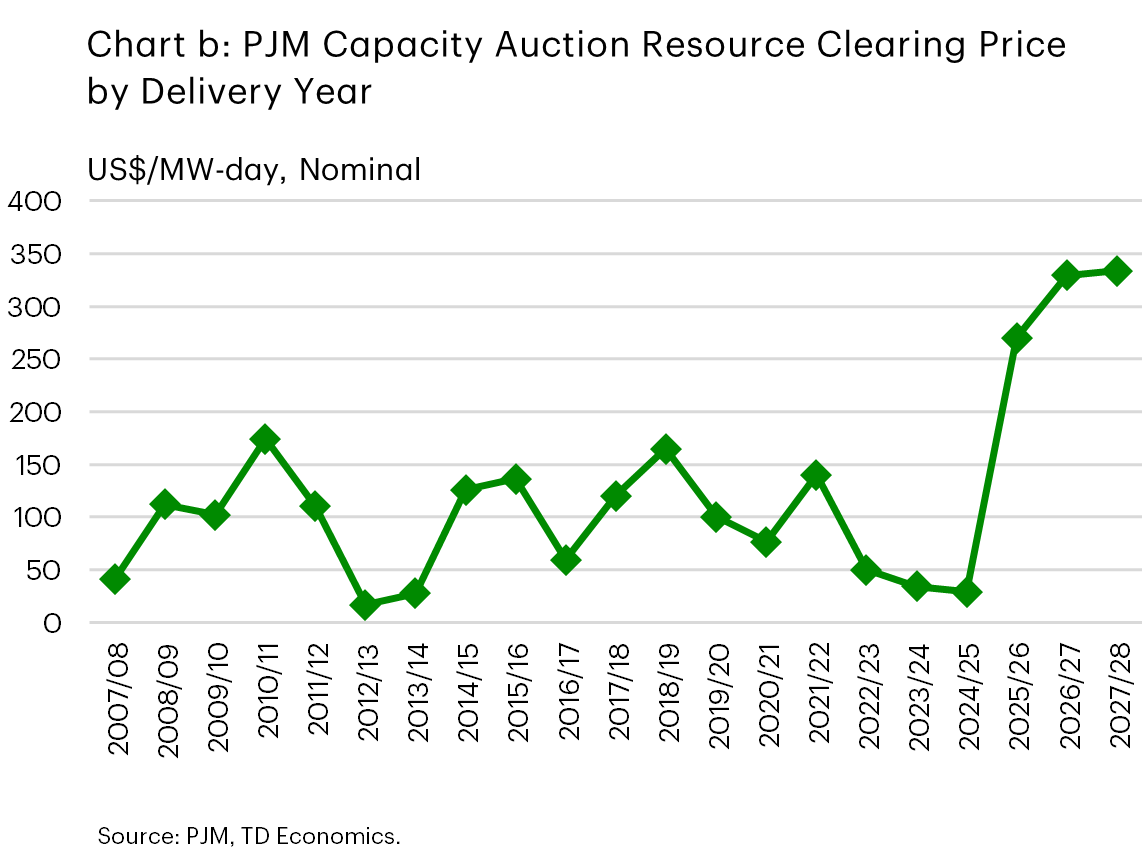

In a way, the PJM market illustrates some of the nuances involved. On the face of it, one would expect faster growth in retail prices in Virginia as the main hub of the data center industry. However, the District of Columbia and New Jersey saw the highest increase in residential prices, driven mainly by the recent spike in capacity prices (chart 6). Electricity generators that participate in PJM’s capacity market are paid for committing to have their generation capacity available when needed in the future. These payments are different from the revenue they earn from selling electricity for use by consumers. Capacity prices for contracts for the 2025-26 to 2027-28 delivery years have increased substantially compared to contract prices for earlier service years (see chart b in appendix). As a result, total annual capacity costs are expected to increase from about US$2 billion for 2024-2025 to US$15-16 billion during 2025-2028, with US$6.5-9.3 billion of these costs attributed to data center load.13

Ratepayers in Virginia have been more sheltered from the increase in capacity prices in part because the two main utilities that operate in the state own generation facilities and are less reliant on the wholesale market for serving their customers. Contrast this with New Jersey where the main utilities do not own power plants and pay capacity costs that are based on PJM prices. Residents of New Jersey felt the impact of the higher 2025-26 capacity prices in the second half of 2025 as the new contracts kicked in.14 With capacity prices for the next two years being even higher than current prices, residential prices in New Jersey and other jurisdictions like DC that use a similar procurement process are likely to stay high in the near term.

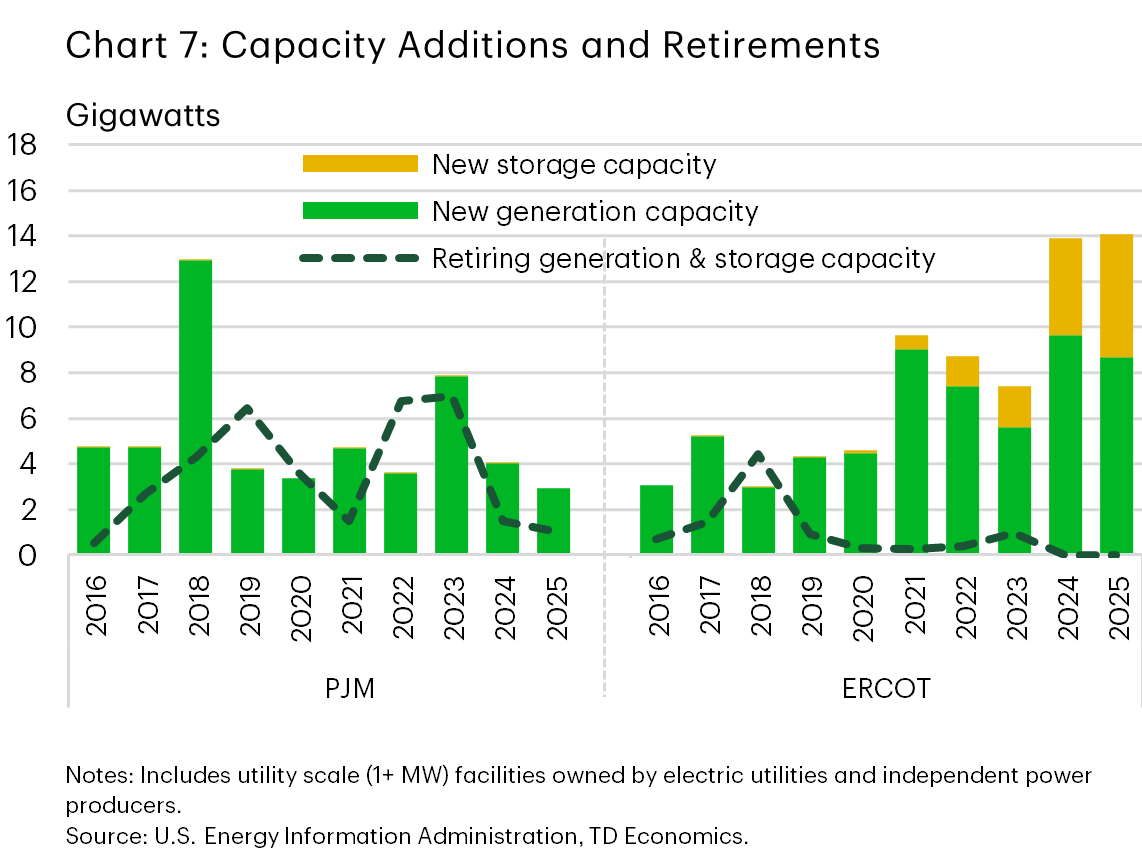

Delays in connecting new generation capacity to the PJM grid combined with capacity losses due to power plant retirements have also exacerbated the impacts of rapid data center load growth. The contrasting trajectories of supply growth in PJM and ERCOT may partly explain why retail prices grew at a slower pace in Texas in 2024 and 2025 even though the state has also added a lot of data center load in recent years.15 In the past five years, PJM brought online about 23 GW of new generation, around 60% of which was solar and wind, while close to 18 GW of capacity was retired. In contrast, ERCOT,16 which is a smaller market, added 40 GW of new generation, 90% of which was solar and wind, and 13 GW of battery storage and lost less than 2 GW to plant retirement (chart 7). It currently takes around 6.3 years on average to connect new generation facilities to the PJM grid compared to 3.7 years in ERCOT, which likely accounts for the smaller capacity additions in PJM. There is a lesson here for Canada as it has also struggled with long connection timelines for renewable energy projects.

Bottom line

Although Canada faces near-term hurdles to its plans to increase AI data center infrastructure due to constrained generation and transmission capacity, the country is not out of the race to attract more of the expected capital expenditures on data centers. Many countries are also dealing with similar grid constraints, which means that regions that can adapt their electricity sectors quickly to enable new large loads to connect to supply in a timely manner will come out ahead.

This situation creates an opportunity for Canada to create conditions that can enable faster data center connection to the grid or to off-grid alternatives. The ‘bring your own generation’ model that is being explored by Alberta is one such promising tool. Data center companies in Texas are already opting for this option as it is faster than waiting to be connected to the grid. Also, other regions are considering it as a way to shelter ratepayers from the costs of building new generation and transmission for data centers. Ontario, on the other hand, can lean on its advantage as the first jurisdiction in North America to build a small modular reactor (SMR). One way to do this would be to include SMRs in the new corporate power purchase agreements program, which allows companies to procure their own generation. The proposed 40 GW offshore wind farm in Nova Scotia is another potential generation source that could support a data center industry in Atlantic Canada.

Whatever policies and tools are used, protecting ratepayers from electricity price increases will be important for gaining public support. Governments can look to jurisdictions in the U.S. and elsewhere for lessons on what can be done differently to avoid repeating actions that have contributed to rising retail electricity prices in other markets like the PJM Interconnection.

Appendix

End Notes

- Joint Legislative Audit and Review Commission, Data Centers in Virginia, December 9, 2024

- Mike Turner, Loudoun County, Virginia: Data Center Capital of the World, October 20, 2025

- McKinsey & Company, The cost of compute: A $7 trillion race to scale data centers, April 28, 2025

- Jack Farrell, Alberta minister wants to see $100-billion in data centre infrastructure in next five years, The Globe and Mail, December 4, 2024

- Innovation, Science and Economic Development Canada, Canada to drive billions in investments to build domestic AI compute capacity at home, December 5, 2024

- CBRE, Montreal: North America Data Center Trends H1 2025, September 8, 2025

- Hydro-Québec, Capacités de raccordement de projets industriels au réseau de transport: 13 zones de développement industriel ciblées, December 2025

- Independent Electricity System Operator, Large Step Loads: Spotlight on Data Centres and Electric Vehicle Supply Chain, July 2025

- Government of British Columbia, New legislation powers economy with clean energy, North Coast Transmission Line, October 20, 2025

- Bloomberg, Ireland ends moratorium on grid links to data centers, December 15, 2025

- International Energy Agency, Energy and AI, April 10, 2025

- Data Center Watch, Q2 2025 Update: 125% Surge in Data Center Opposition

- Monitoring Analytics, Analysis of the 2027/2028 RPM Base Residual Auction: Part A, January 5, 2026

- Bates White Economic Consulting, Annual Final Report on the 2025 BGS RSCP and CIEP Auctions, May 6, 2025

- ERCOT also does not have a capacity market.

- Lawrence Berkeley National Laboratory, Queued Up: Characteristics of Power Plants Seeking Transmission Interconnection, 2025 Data File, December 2025

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: