Bridging Alberta’s AI Data Center Power Gap: A Case for Renewables

Likeleli Seitlheko, Economist

Date Published: June 16, 2026

- Category:

- Canada

- Future Ready Economy

Highlights

- Available grid capacity for new data centers in Alberta is minimal relative to demand from developers, which will necessitate significant new generation buildout.

- Although the province has abundant natural gas resources, expansion of gas generation is challenged by global turbine shortages and rising capital costs of new gas generation.

- Faster deployment timelines for renewable energy and falling battery costs position hybrid renewable-storage systems as viable solutions for powering new data centers especially under the province’s ‘bring your own generation’ model.

Alberta aims to position itself as the premier location for building artificial intelligence (AI) data centers in North America. However, limited electric grid capacity is slowing development. In the first phase of the Alberta Electric System Operator’s (AESO) large load integration program, just 1.2 gigawatts (GW) are available for data centers, representing less than 6% of the total capacity being sought for grid connection. Accommodating additional data center capacity commensurate with the province’s ambitions will require extensive expansion of electricity generation capacity.

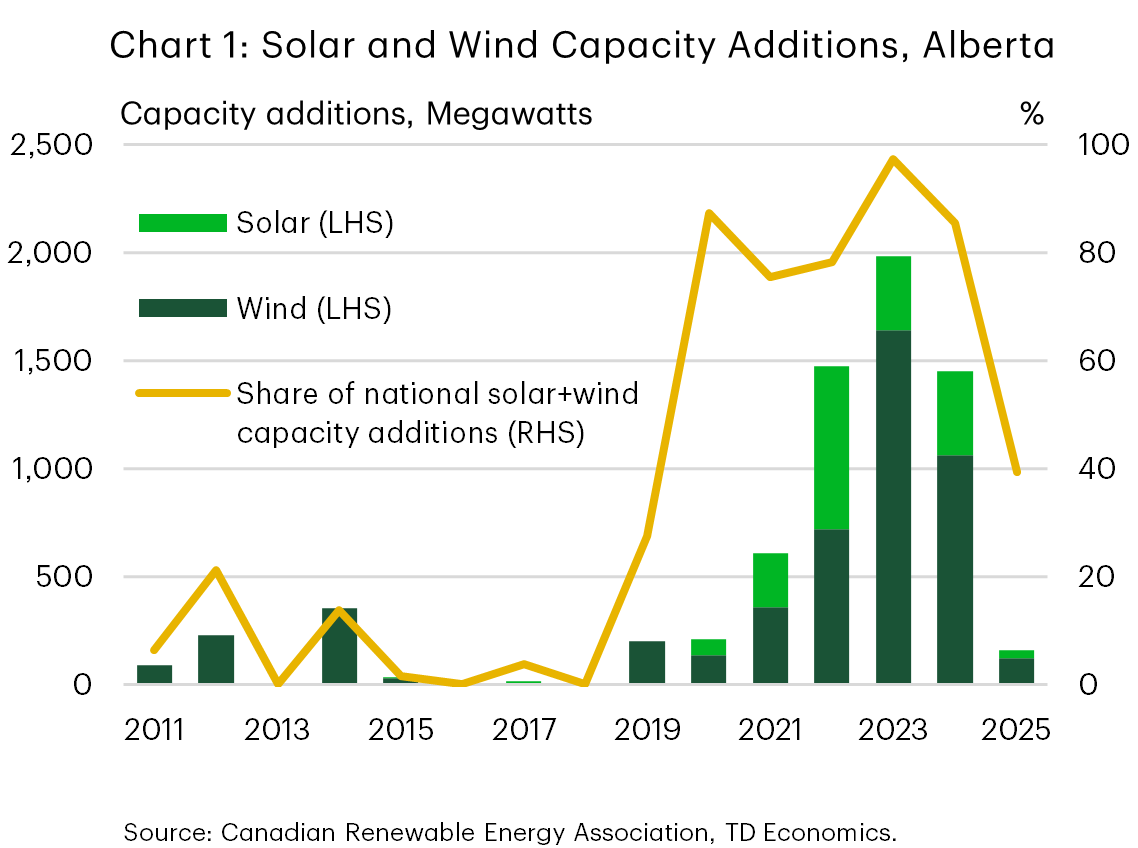

While Alberta’s AI Data Center Strategy highlights the dominant role that natural gas is expected to play in providing needed power to the industry1, supply chain issues for gas turbines could hinder a rapid buildout of natural gas power plants. This could pave the way for greater renewable energy capacity additions (plus storage), reversing course for a sector whose fortunes have declined recently, following years of sustained growth (chart 1). In their recent Implementation Agreement, the federal and Alberta governments pledged to support investment for renewables and boost electricity supply for data centers,2 highlighting renewables’ potential to supplement gas generation. Meanwhile, uncertainty surrounding power project economics will persist in the near term as Strait of Hormuz-related disruptions to the supply chains of natural gas and critical minerals will take time to resolve, assuming the new U.S.-Iran deal results in lasting peace.

New gas power generation projects slowed by turbine supply constraints

As Canada’s largest natural gas producing region, it is not surprising that gas generation is expected to be a leading source of power supply for data centers, as outlined in the province’s AI Data Center Strategy. However, these expectations are likely to run up against a tight gas turbine market, which is causing delays and even cancellations for new gas power plant projects.

The jump in demand for new gas electricity generation to power data centers has increased the capital costs of new gas power plants and strained global supply chains of gas turbines. Although the data center boom has largely been a U.S. story, Canada is subject to the same supply constraints as it uses similar equipment that is calibrated for the North American grid frequency. Moreover, the global gas turbine market is dominated by a handful of companies. The major manufacturers, such as Siemens Energy, GE Vernova and Mitsubishi Power, are said to be facing order backlogs stretching over five years for large turbines.3 Wait times for smaller turbines are shorter but rising. Equipment shortages have already contributed to the cancellation of gas power plant projects in the U.S.4 Also to blame is a doubling in capital costs over the past two years that has raised the levelized cost of energy for combined-cycle gas turbine plants by 22%.5

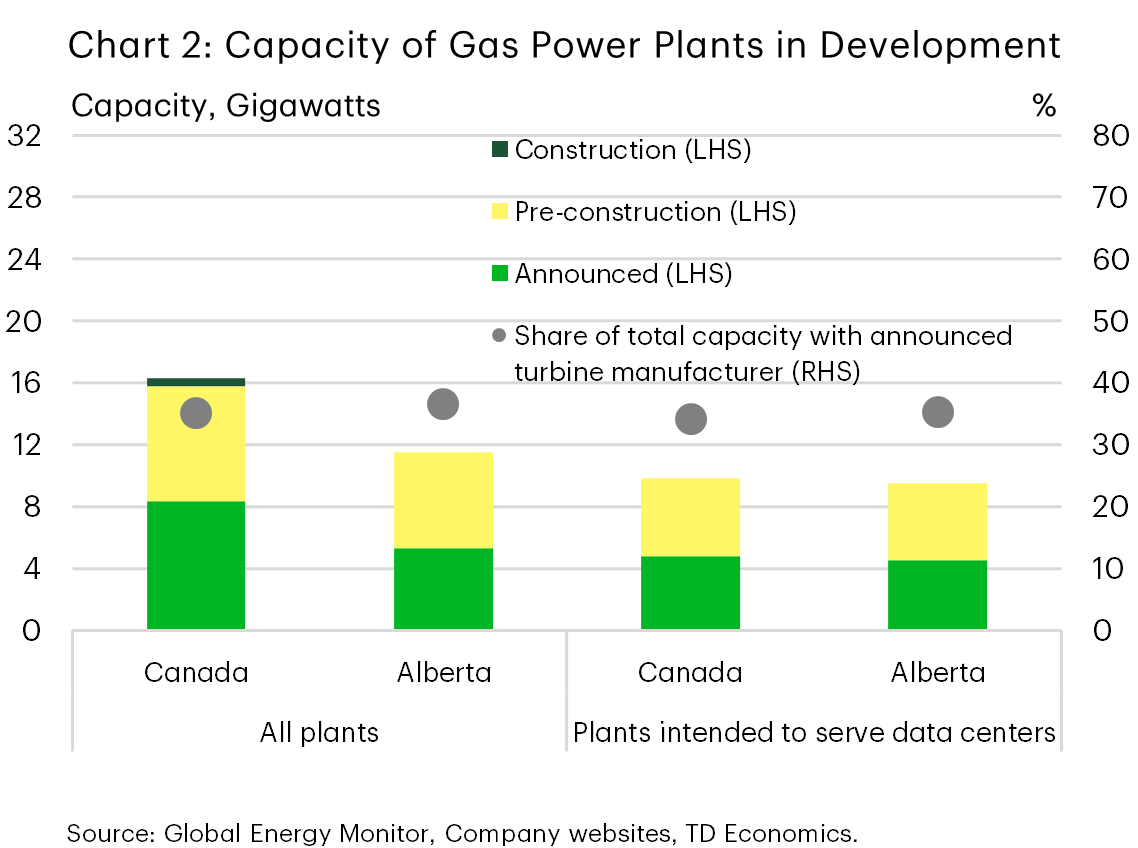

It is likely that some of the proposed gas plants in Alberta will also face delays due to these supply constraints, especially projects that have not yet reserved manufacturing slots for turbines. Approximately 35% of the proposed capacity in Alberta comes from projects that have disclosed their turbine technology and manufacturer (chart 2). While this data is not conclusive, it provides an indication of the proportion of projects that may already be in the queue for turbines although delivery timelines are generally unknown. One company with a project in Alberta publicly disclosed earlier this year that it had signed a reservation agreement with GE Vernova for a turbine that will be delivered by 2030. This is consistent with disclosures from GE Vernova, which has reported that it is sold out through 2028 and has 10 GW of cumulative capacity available for 2029 and 2030.6

Challenges with gas turbine procurement and affordability could resurrect the fortunes of the renewables sector in Alberta, which has been in a chill over the past two years, as developers look for other sources of power to supplement gas generation.

Alberta’s renewable energy market in a lull after years of growth

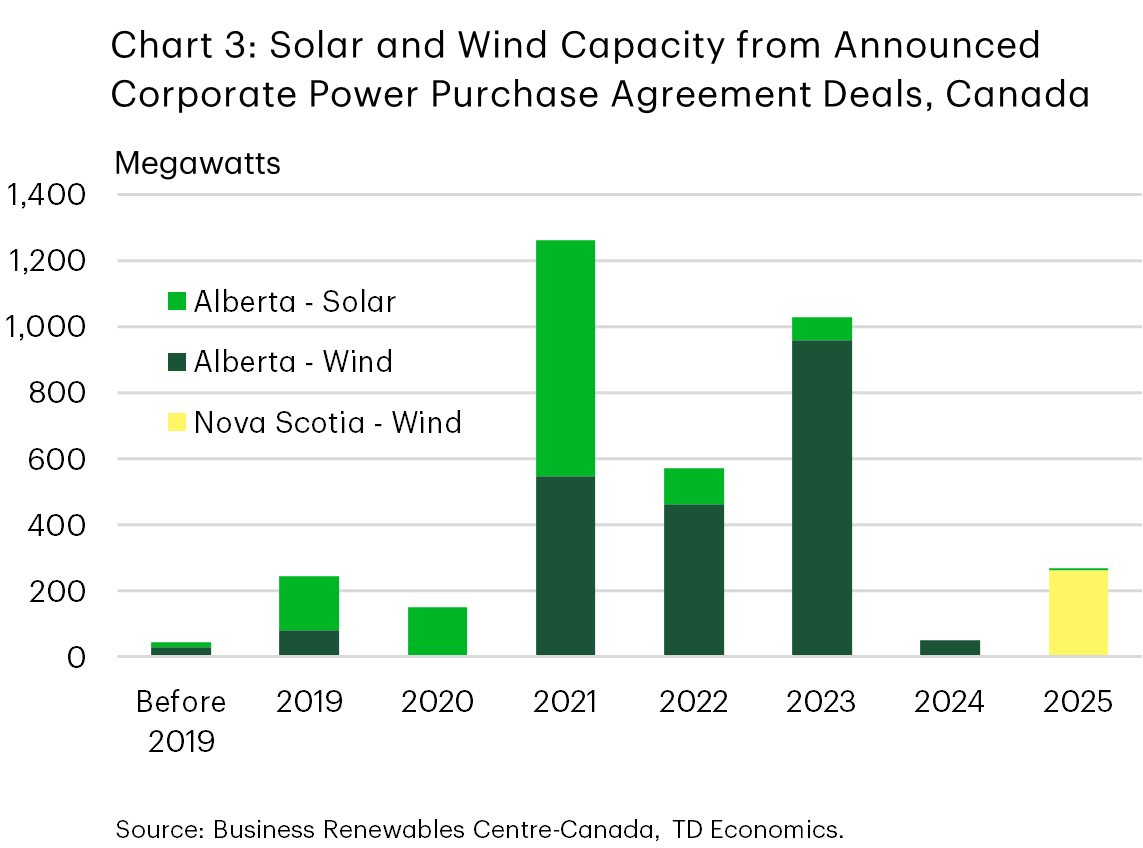

The renewable energy sector had a brief period of growth in Alberta starting during the pandemic when the province led Canada in renewable energy development. Combined solar and wind capacity additions in the province peaked in 2023 at nearly 2 GW, accounting for virtually all the renewable capacity installed in Canada that year (chart 1). The rise of renewables in Alberta was supported by power purchase agreements (PPAs) mainly from the corporate sector (chart 3). From 2019 to 2025, around 3.3 gigawatts (GW) of solar and wind capacity were contracted through PPAs7, representing over half the solar and wind capacity added to the Alberta grid during that period. However, the volume of new PPA contracts in Alberta dried up in 2024 and 2025 while new renewable capacity coming online started declining in 2024 and collapsed in 2025, reaching its lowest level since 2018.

The downturn in the renewable energy sector was driven by changes within Alberta’s electricity sector, including a moratorium on renewable project approvals that was in place from August 2023 to February 2024. Regulatory changes that were introduced at the end of the moratorium such as siting restrictions for solar and wind facilities also contributed to project withdrawals. Moreover, the electricity market reforms that the AESO was working on, such as updates to pricing systems, created uncertainty that may have put developers in a wait-and-see mode.

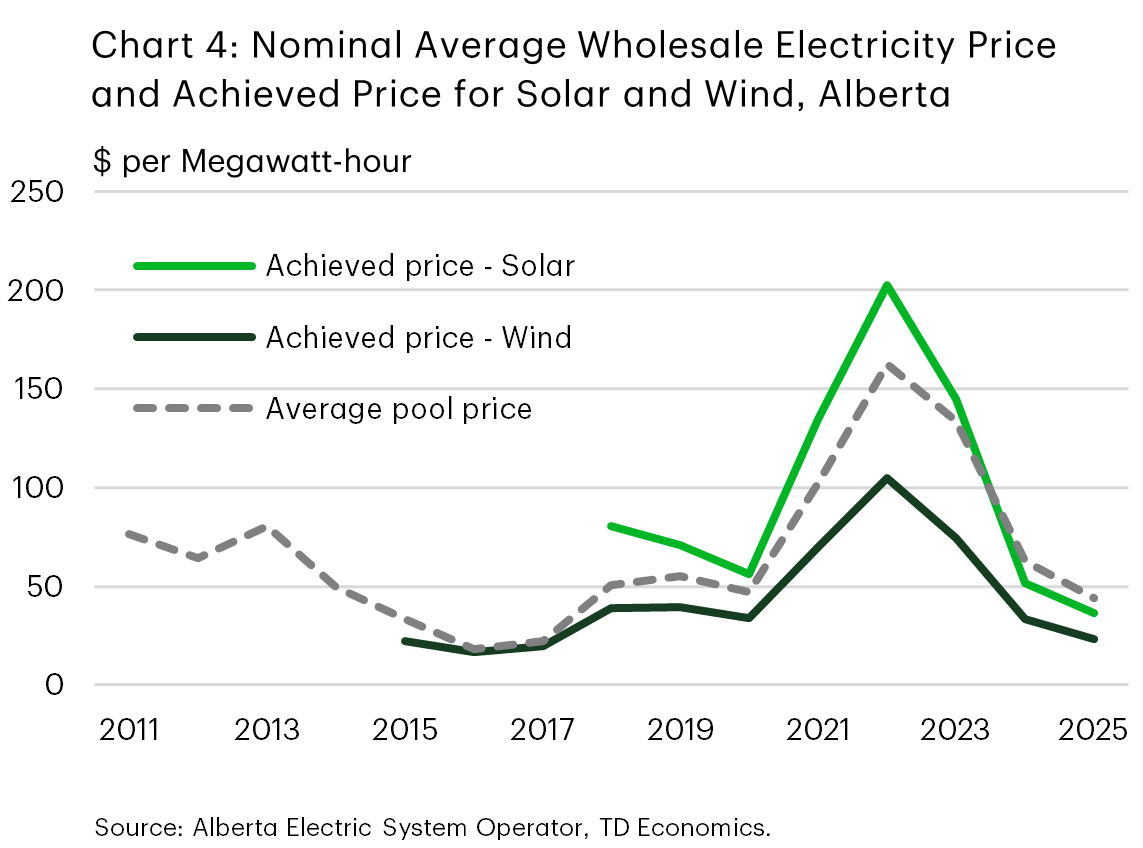

Market forces have also been at play. The average annual wholesale electricity price has declined each year since 2022, reaching roughly $44 per megawatt-hour in 2025, its lowest level since 2017 (chart 4). This was partly caused by large capacity additions of gas, solar and wind generation facilities during 2021-2024 that greatly outpaced demand growth.8 Furthermore, the average yearly price for wind power sold in the wholesale market was less than the overall annual market price because wind farms often produce electricity at the same time and generation is usually higher at night when demand is lower. Solar power also sold for less than the average annual market price over the past two years as its installed capacity has increased (chart 4). However, the growth of the data center industry could supercharge electricity demand and bolster wholesale prices, potentially improving the economics of renewable projects.

Turbine shortages could lead to renewable energy market recovery in Alberta…

Given the huge volume of data center capacity seeking to connect to the Alberta grid, the province is exploring a ‘bring your own generation (BYOG)’ model as an interim solution. While new gas generation is the preferred resource for powering surging AI energy demand as seen in the U.S., ongoing gas turbine shortages could create opportunities for other sources of power including renewables. For some of the Alberta data center projects that were not selected in the first phase of AESO’s large load integration program and hoping to make the cut in the next BYOG phase, solar and wind could offer a relatively faster pathway to meet their electricity demand. In addition, battery costs have been falling steadily, reaching their lowest level in 2025 – US$78 per megawatt-hour, down 27% from 20249 – which makes hybrid renewable-battery projects more cost competitive. Storage helps firm up intermittent generation from solar and wind, making the hybrid systems better suited to power data centers though grid backup will still be necessary.

There are already hybrid renewable-storage projects under development aimed at supplying electricity to data centers, such as the Google and Intersect Power co-located data center and solar-storage facility in Texas. Given Alberta’s rich renewable resources, similar initiatives are likely to emerge, especially as there is now clarity on the nature of the electricity market reforms. Without enabling renewables to play a bigger role, the province risks falling behind on its objective to establish itself as a leading data center location as gas generation alone will not be sufficient to meet the industry’s energy needs. Moreover, a thriving data center industry in Alberta would significantly contribute to Canada’s ambition of developing sovereign AI data centers.

…But uncertainty from the Iran conflict puts sand in the gears

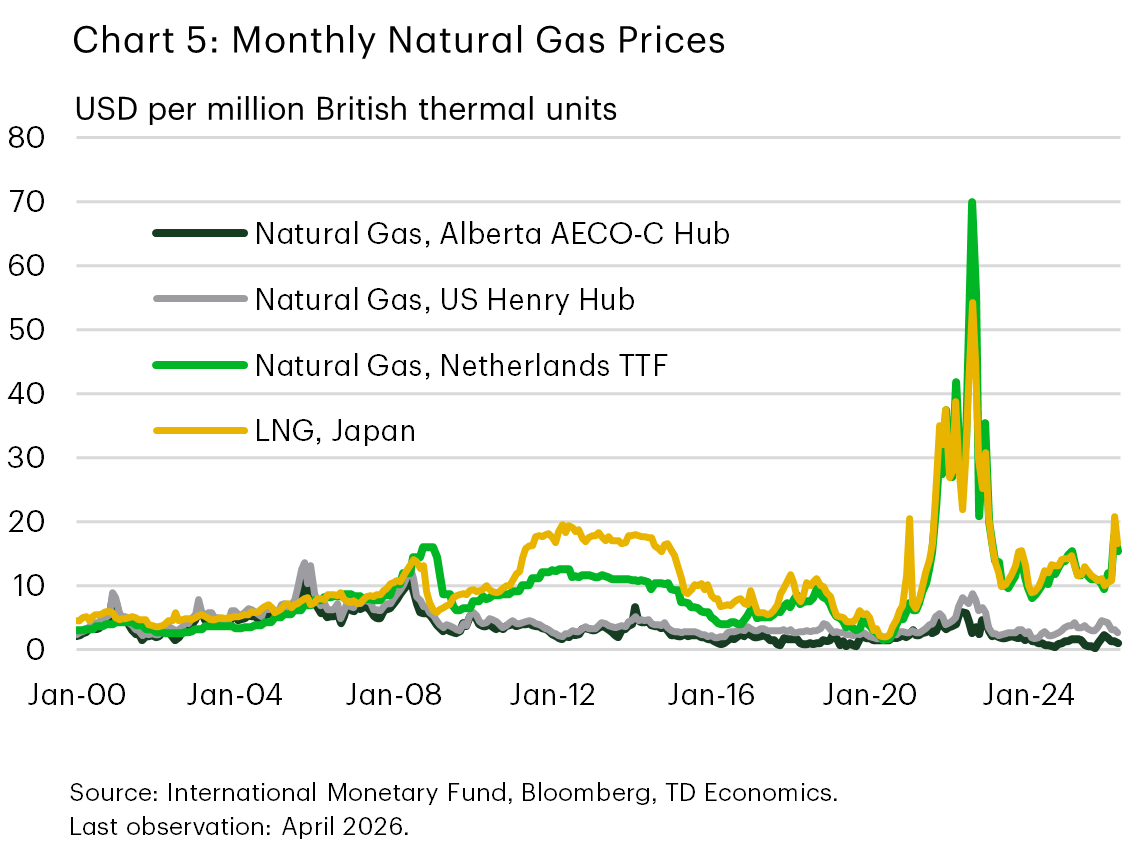

The Iran conflict has not only disrupted fossil fuel supply, it has also affected the supply of commodities that are integral for producing low-carbon technologies. The closure of the Strait of Hormuz has cut off exports of liquefied natural gas (LNG) from Qatar and the United Arab Emirates, which account for roughly a fifth of global LNG exports.10 This has led to significant price increases in Asia, the main recipient of Gulf LNG exports, and Europe (chart 5). In addition, reduced supply of sulphur from Gulf countries, which produce nearly a quarter of global supply, is impacting the production of metals like copper and nickel whose processing relies on sulphuric acid. Nickel is utilized in wind turbines and batteries while copper is essential for all generation technologies although wind turbines and solar panels require greater amounts per megawatt of capacity. Moreover, the Gulf is one of the biggest producers of primary aluminium,11 which is also critical for many low-carbon technologies including wind turbines and batteries but more so for solar panels.

While the newly announced framework agreement for peace between the U.S. and Iran promises the reopening of the Strait of Hormuz, it will take months or longer for supply flows to return to pre-war normals. This is of course assuming that the deal leads to permanent peace and does not come apart if the parties fail to reach compromise on some of the complex issues that are yet to be negotiated. So far, the rise in natural gas prices is smaller than that triggered by the onset of the Russia-Ukraine war in 2022 (chart 5). Higher natural gas prices in 2022 increased the levelized cost of energy for new gas-fired power plants that year (by 23%) though the cost declined the following year with falling fuel prices. A sustained disruption to critical mineral supply chains could similarly increase capital costs for renewable energy and grid storage.

Bottom line

Alberta’s push to become a leading North American hub for AI data centers is running up against severe power supply constraints. Meanwhile, gas turbine supply bottlenecks and rising capital costs raise the risk of delays to expanding gas‑fired generation. This creates an opportunity for renewables paired with storage to support data center growth under the province’s ‘bring your own generation’ model. Enabling a greater role for renewables will be critical for Alberta to meet its ambitions as gas alone is unlikely to deliver sufficient generation capacity in the required timeframe. However, uncertainty around power project economics will likely persist for some time as disruptions to natural gas and critical mineral supply chains caused by the closure of the Strait of Hormuz will take months to resolve, assuming the new deal between the U.S. and Iran leads to lasting peace.

End Notes

- Government of Alberta, Alberta’s AI Data Centre Strategy: Powering the future of artificial intelligence, December 4, 2024

- Office of the Prime Minister, Canada and Alberta strike agreement to diversify our exports, reduce emissions, and build a stronger economy, May 15, 2026

- Anna Flávia Rochas, Power developers adapt gas turbine strategies to mitigate tight supply, Reuters, March 2, 2026

- Kevin Clark, Long lead times are dooming some proposed gas plant projects, Power Engineering, February 20, 2025

- BloombergNEF, Sustainable Energy in America 2026 Factbook: Tracking Market & Policy Trends

- GE Vernova, 1Q 2026 Earnings Conference Call, April 22, 2026

- Business Renewables Centre-Canada, Deal Tracker data

- Alberta Electric System Operator, 2025 Annual Market Statistics, March 11, 2026

- BloombergNEF, Battery Storage Costs Hit Record Lows as Costs of Other Clean Power Technologies Increased, February 18, 2026

- Energy Institute, 2025 Statistical Review of World Energy Data, June 26, 2025

- The International Aluminium Institute, Primary Aluminium Production Data

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: