Dollars and Sense

U.S. Dollar: The Great Unwind

Beata Caranci, SVP & Chief Economist | 416-982-8067

Thomas Feltmate, Director & Senior Economist | 416-944-5730

Maria Solovieva, CFA, Economist | 416-380-1195

Date Published: April 29, 2025

- Category:

- Canada

- Forecasts

- Financial Markets

Highlights

- The sharp increase in trade tensions has undermined America’s economic exceptionalism narrative, acting as a catalyst pressuring the greenback lower over the last four months.

- The potential for both higher inflation and unemployment puts policymakers in a tough spot. A weakening economy should win-out in the Fed undertaking “insurance” cuts this summer.

- The depreciation of the dollar is likely not yet complete. We anticipate at least another 3% slippage in the broad trade weighted measure by year-end.

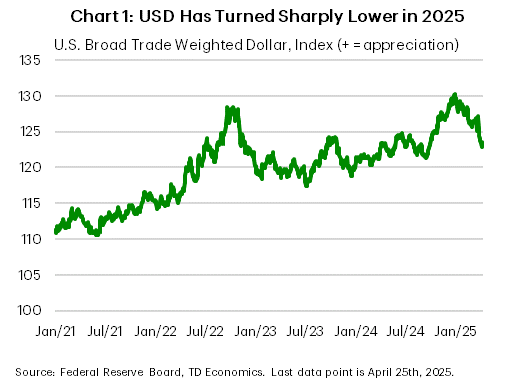

The U.S. dollar has hit a wall in 2025. After appreciating by over 16% between 2021 and 2024, the trade-weighted dollar has given back over a quarter of those gains in just four months (Chart 1). Many investors are questioning the ability for the U.S. economy to maintain its exceptional global growth position as uncertainty lights up the airwaves. The administration’s on-again-off-again tariff approach has spiked the economic policy uncertainty index to pandemic levels, has pushed consumer and business sentiment indicators sharply lower, and has tightened financial conditions. Although President Trump has backed off rhetoric that shook investor confidence in the Federal Reserve’s independence – a bedrock of global financial stability – the threat lingers and will remain top of mind with the next Chair appointment in May 2026.

Fed futures are priced for nearly four quarter-point rate cuts this year, one more than our forecast. But trying to pinpoint the exact amount in today’s uncertain environment is a bit of a fool’s errand. There are considerable risks to the near-term economic outlook, with the potential for both rising unemployment and higher inflation, creating tension between the Fed’s dual mandate of price stability and maximum employment. Difficult forecast environments mean that the best course of action is for policymakers to be in risk-management mode. And on that front, analysts have been universally marking down forecasts in a demonstration that the economic risks have tilted to the downside. With a policy rate sitting at 4.50% -- the highest of any G7 country – the Fed has room to undertake two-to-three insurance cuts to inject some balance to the risks created by a tariff policy shock of magnitude and scope never witnessed in history. Even though the near-term risks to inflation are to the upside, this will ultimately prevent a more aggressive policy response to a weakening economy. Under this scenario, the greenback could depreciate by another 3% by year-end. However, there’s scope for the dollar to fall even further should fiscal pressures start to mount or there’s another brush-up with the debt ceiling later this summer.

Challenging the Status Quo

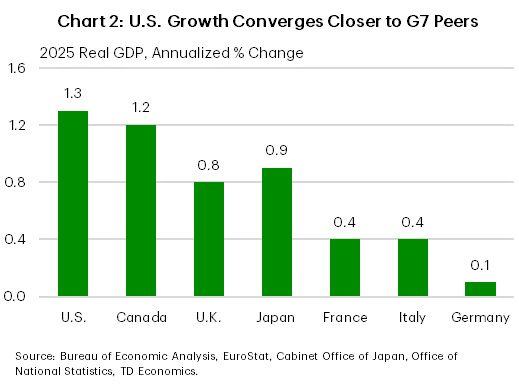

The U.S. economic recovery was a global stand-out following the pandemic, creating a wave of investor interest in dollar-denominated assets. Between 2021 and 2024, the dollar surged against both advanced (+18%) and emerging market (+14.5%) economies. The economy revealed tailwinds that were strong enough to weather not only a 1970’s-style surge in inflation but also the highest Fed funds rate since the early-2000’s. For context of its outperformance, the U.S. economy averaged annualized growth of 2.8% over the two-years ending in 2024, which was more than 3.5 times the average growth experienced across other G7 economies over the same period.

But the sharp shift in trade policy is now undermining that exceptionalism narrative. Higher tariffs will not only erode real household incomes but also firm profitability. We expect the U.S. economy to expand by just 1.3% in 2025, bringing it more in line with G7 peers (Chart 2).

Fed’s Next On Deck

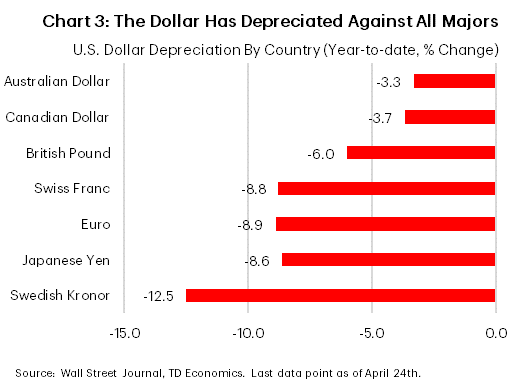

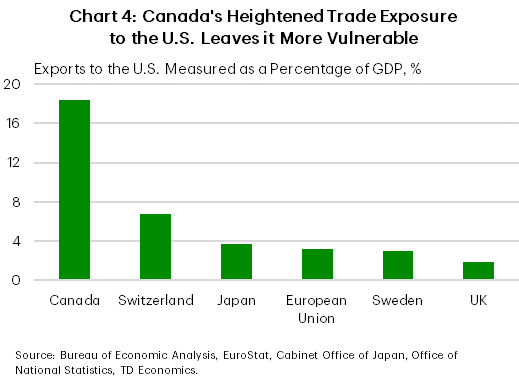

On a trade-weighted basis, the 5% depreciation in the dollar so far this year has come mostly from a pullback against advanced economies (-8%). The biggest moves were against Sweden (-12.5%), Switzerland (-8.8%), the EU (-8.9%), and Japan (-8.6%) (Chart 3). Meanwhile, the U.S.-Canada cross has slid by a little less than 4%, as Canada’s heightened trade exposure to the U.S. leaves it more vulnerable to a persistent trade spat (Chart 4).

At this point, there is still great uncertainty on the economic outlook. Embedded in our forecast, is a view that economic growth stalls through H1-2025, before gradually edging higher alongside some reprieve in tariffs. Under this “tariff-reprieve” assumption, a sharp reversal eventually occurs in near-term inflation dynamics. However, in the interim, core PCE inflation could reach anywhere from 3-4% over the coming quarters – up from a pace of 2.6% in March. That rise in inflation is expected to be met with a modest increase in the unemployment rate, creating tension in the Fed’s dual mandate of maximum employment and price stability. Against this backdrop, Chair Powell has said that policymakers would have to assess which of its mandates were further from their long-run goal and adjust policy accordingly. Provided inflation expectations remain reasonably anchored, policymakers can provide some rate-relief to limit the hit to growth, perhaps as early as June. If the Fed were to cut by a total of 75 bps by year-end, our models suggests that the narrowing in interest rate differentials vis-à-vis other advanced economies could pressure the dollar lower by as much as another 3%.

Fiscal Pressures Add Further Downside Risk…

Beyond interest rate differentials, there is also the impact that a new fiscal package could have on the dollar. Investors have become increasingly mindful of the worsening fiscal trajectory, and the Republican’s tax cut agenda is highly likely to add further pressures to deficits over the coming years.

As it currently stands, House and Senate Republicans have agreed on the broad strokes of a multi trillion-dollar budget framework that includes significant tax cuts and further spending on defense, energy, and immigration. While it’s still early days, the proposed plan(s) could add anywhere from $2.8 – $5.8 trillion to the deficit over the next decade. The upper-end estimate exceeds the nearly $5 trillion spent on fiscal stimulus during the pandemic.

A sharp increase in the deficit stemming from unfunded tax cuts is bringing back memories of the United Kingdom’s 2022 “mini” fiscal crisis. Following the release of a five-year, £162 billion tax cut and spending plan, Gilt yields jumped by over 200 bps, and the pound depreciated by nearly 10%. We’re not expecting these types of moves, but it does highlight the directional risks to yields and the dollar should the fiscal package land on the high side. Conventional estimates suggest that for every percentage point increase in the deficit (measured as a share of GDP), it can add anywhere from 10-30 bps to longer-term yields. In the event investors ever started to question the credibility of U.S. sovereign debt holdings, there’s potential for the dollar to be pressured lower.

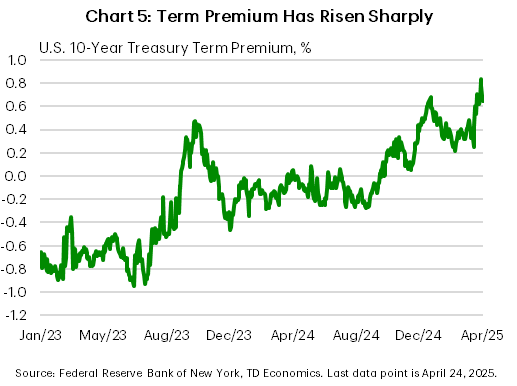

Admittedly, some of this “risk” has already been priced into yields and the dollar amidst the recent pullback. Financial markets rarely move in an orderly fashion, and the recent spike in the 10-year term premia – hitting a 10-year high – underscores investors growing angst (Chart 4).

Uncertainty on the debt ceiling is also likely playing some role. Based on tax receipts collected to date, we estimate that the Treasury will have sufficient funds to last until mid-July. Congress’s current plan is to raise the debt ceiling by $4-5 trillion as part of the larger tax reconciliation package, which Republicans are hoping to pass by Memorial Day (May 26th). Any push back on that timing could result in the debt ceiling portion getting split into a separate bill to avoid breaching the debt limit. But any brush-up to the “X-date” would further shake investor confidence.

… Recent Attacks On Powell Haven’t Helped

Adding fuel to the fire is the erosion of the Fed’s perceived independence. President Trump’s public dissatisfaction with Chair Powell—voiced through social media and tacitly echoed by National Economic Council Director Kevin Hassett—has gotten the attention of not gone unnoticed markets. The dollar’s sharp decline on April 21st stands as a clear pricing-in of this risk: the fear that the Fed might succumb to political pressure and prioritize short-term presidential goals over its inflation-fighting mandate. In that scenario, the “loser” label—Trump’s own words for Powell—could well apply to the dollar, as investors reassess the greenback’s role as a stable store of value.

Though those fears have since moderated, the episode marked a turning point. Markets no longer take Fed independence for granted. This loss of certainty joins a broader list of unorthodox risks, including a “weak dollar” policy as outlined in the Council of Economic Advisors Chair Stephen Miran’s blueprint, published last year. While President Trump has never endorsed this approach and has, in fact, threatened retaliation against countries seeking alternatives to the dollar, the so-called “Mar-a-Lago Accord” has entered the financial lexicon. The mere possibility of its resurrection could jeopardize the dollar’s safe-haven status and raise questions about America’s role as issuer of the world’s primary reserve currency.

Portfolio flows remain the bedrock of the dollar’s strength. The long-held belief that there is “no alternative” to U.S. assets—thanks to their unrivaled liquidity and institutional depth—has kept capital anchored in U.S. markets. But that assumption is beginning to fray. While it’s difficult to quantify how much of the recent dollar depreciation stems from foreign divestment, the signs are mounting. The latest Commitments of Traders report shows a surge in short positions on 10-year Treasury futures, nearing the levels seen last August when the Fed hinted at a more dovish path.

In short, we are in uncharted territory – today’s risks are structural and political. Accounting for recent depreciation, the dollar is nearing its fair value, but how much further and how quickly it adjusts in the future may depend less on rates, and more on whether markets continue to believe in the rules that once underpinned its supremacy.

Bottom Line

Heightened trade tensions have sparked fears of U.S. economic stagnation, in the best case, and a recession, in the worst case. This has been the primary catalyst pressuring the dollar lower. At this point, the future path of monetary policy is highly uncertain and dependent on the evolution of the economic data. But the end of America’s economic exceptionalism is not the only factoring weighing on the dollar. Increased fiscal pressures, the potential for another debt ceiling showdown and attacks on Fed independence are also notable headwinds. So long as these risks linger, there’s potential for further downside pressure on the dollar, beyond what underlying fundamentals would suggest.

Forecast Tables |

|---|

| Interest Rate Outlook |

| Foreign Exchange Outlook |

| Commodity Price Outlook |

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.