2026 Saskatchewan Budget

Red Ink Returns, But Risks Contained

Marc Ercolao, Economist | 416-983-0686

Date Published: March 18, 2026

- Category:

- Canada

- Government Finance & Policy

Highlights

- For the year ahead, Saskatchewan is projecting a narrower deficit of under 1% of GDP, with its sights set on returning to black ink over the medium term.

- The debt-to-GDP ratio is expected to creep up in FY 2026/27, but remain at a comparatively low levels.

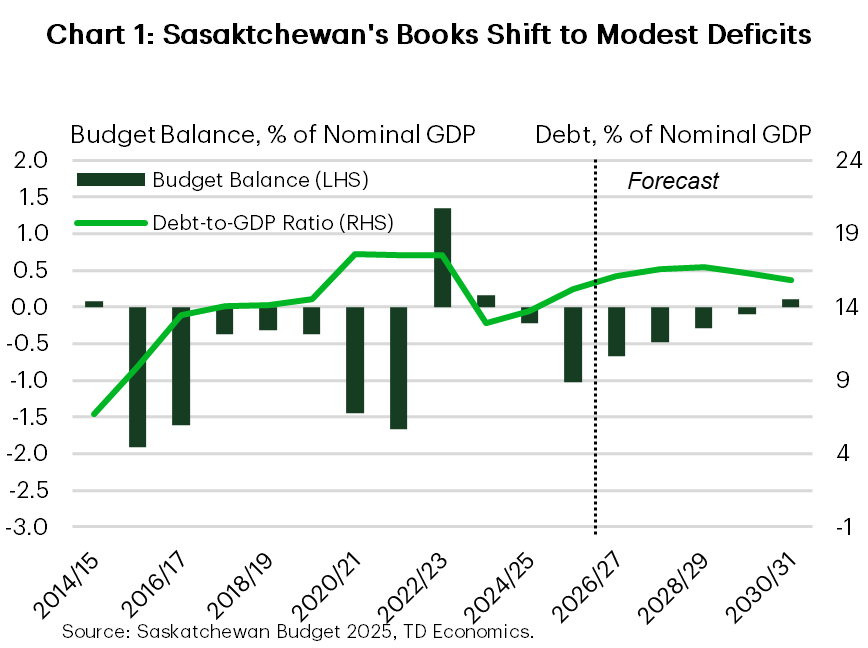

The Province of Saskatchewan is projecting a moderate $819 million deficit in FY 2026/27 (0.7 % of GDP), a marginal improvement from the $1.1 billion shortfall now estimated for the current fiscal year. The overall erosion of the fiscal position – relative to last year’s surplus projection – resulted from cost overruns in health care and wildlife response as well as emergency spending. The government forecasts ongoing, though gradually diminishing, deficits with the objective of attaining a modest surplus by FY 2030/31.

The budget sprinkles in some new affordability measures, including a doubled Volunteer First Responders’ Tax Credit, a 5% boost to low-income tax credits, and a one-time utility arrears repayable benefit. Most support measures outlined in the budget come from continued tax credits and sector aids. The government also reformed the corporation capital tax (CCT), raising the rate for large institutions from 4% to 6% as of April 1, while eliminating CCT for small financial institutions.

Revenue Outlook Faces Upside

Total revenues are projected to rise by 2.9% in FY 2026/27, recovering after a year of near zero growth. Gains in provincial sales taxes (PST) and federal transfers are expected to account for the bulk of the increase. In contrast, personal income tax growth is anticipated to be slight as tax credits introduced last year are set to also weigh on this year’s anticipated take.

Meanwhile, there appears to be some upside risk to the government’s assumptions around non-renewable resource revenue. Notably, the budget assumption of $59.75/bbl for WTI for the next fiscal year now appears very conservative, especially since prices have surged roughly 40% since the month began due to ongoing conflict in the Middle East. According to our latest forecast, oil prices are likely to average at least $75/bbl. That would add more than $250 million to government revenues based on the government’s latest sensitivity estimates. Elsewhere in the commodity space, 2026 budget projections for potash prices ($289/tonne) and the Canadian dollar (72.7 cents/USD) appear reasonable.

The economic outlook more broadly is derived from average private-sector economic forecasts that were collected in early February, before the ongoing war in the Middle East. Real GDP projections of 1.6% and 2.0% for 2026 and 2027, respectively, are still prudent and align with our own latest forecasts released earlier this week. However, we see additional upside to this year’s revenue forecast from higher GDP inflation in 2026 compared to that assumed in the budget.

Saskatchewan Economic Assumptions

[ Percent Change Unless Otherwise Noted ]

| Budget 2026 | |||||||

| Calendar Year | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | |

| Nominal GDP | 0.0 | 4.3 | 3.3 | 4.3 | 3.9 | 3.6 | |

| Real GDP | 3.0 | 2.2 | 1.6 | 2.0 | 2.4 | 2.4 | |

| Unemployment Rate (%) | 5.4 | 5.2 | 5.1 | 5.1 | 5.1 | 5.2 | |

| CPI | 1.4 | 2.1 | 2.3 | 2.1 | 2.0 | 2.0 | |

| WTI (US$/Barrel) | 74.5 | 61.7 | 59.8 | 63.5 | 69.0 | 72.5 | |

| Potash (US$/KCI Tonne) | 233 | 271 | 289 | 299 | 308 | 318 | |

Program Spending Modest; Capital Spending Elevated

Total spending in FY 2026/27 is expected to grow by a tepid 1%, slowing from the upwardly-revised 4.3% growth estimated in the current year ending in March. Health care and education expenditures will gobble up nearly 60% of the total spend. Lower spending earmarked for security, environment and natural resources are expected to provide an offset.

Saskatchewan’s capital plan is expected to pull back to $4.3 billion in FY 2026/27, a 7% decrease from last year’s levels. That said, capital spending plans of $4.4 billion on average over the next three years still put spending well above historical levels.

Net Debt Trajectory Still Intact

The net debt-to-GDP ratio is projected to rise modestly to 16.7% over the next few years, before embarking on a gradual decline thereafter. This is a modest uptick that contrasts with the general provincial trend of steeper increases. Moreover, it solidifies Saskatchewan’s standing as the province with the second lowest debt burden. The near-term rise in debt levels primarily results from ongoing deficits and capital borrowing. Meanwhile, total borrowing requirements for FY 2026/27 are slated to decrease by 9% to $5.3 billion, although new in-year taxpayer-supported borrowing caused the total FY 2025/26 requirement to exceed last year’s budget forecast by over $1.8 billion.

Bottom Line

Saskatchewan is expecting a second straight deficit in the year ahead, albeit manageable while prudent underlying economic assumptions leave scope for a revenue overshoot. The outlook for relatively solid economic growth in the province and moderate spending plans should allow Saskatchewan to restore fiscal balance in due course.

Saskatchewan Government Fiscal Position

[ Millions of C$ unless otherwise indicated ]

| Fiscal Year | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | 2030-31 | |

| Forecast | Budget | Target | Target | Target | Target | ||

| Revenues | 20,804 | 21,417 | 22,295 | 23,209 | 24,161 | 25,151 | |

| % Change | 2.1 | 2.9 | 4.1 | 4.1 | 4.1 | 4.1 | |

| Expenditures | 22,014 | 22,236 | 22,903 | 23,591 | 24,298 | 25,027 | |

| % Change | 5.5 | 1.0 | 3.0 | 3.0 | 3.0 | 3.0 | |

| Surplus (+)/Deficit (-) | -1,211 | -819 | -608 | -381 | -138 | 124 | |

| % of GDP | -1.1 | -0.7 | -0.5 | -0.3 | -0.1 | 0.1 | |

| Net Debt | 16,675 | 18,421 | 19,620 | 20,587 | 20,878 | 20,966 | |

| % of GDP | 15.2 | 16.1 | 16.6 | 16.7 | 16.3 | 15.8 | |

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: