2026 New Brunswick Budget

Swelling Deficits

Marc Ercolao, Economist | 416-983-0686

Date Published: March 18, 2026

- Category:

- Canada

- Government Finance & Policy

Highlights

- New Brunswick is expected to record a deficit of 2.7% of GDP in FY 2026/27. Shortfalls improve only by a razor thin margin over the three-year projection horizon.

- The Province’s debt burden is expected to record steady increases over the next several years. At 30.6% in FY 2026/27, New Brunswick’s debt-to-GDP ratio would still be on the lower end of Canada’s provincial jurisdictions.

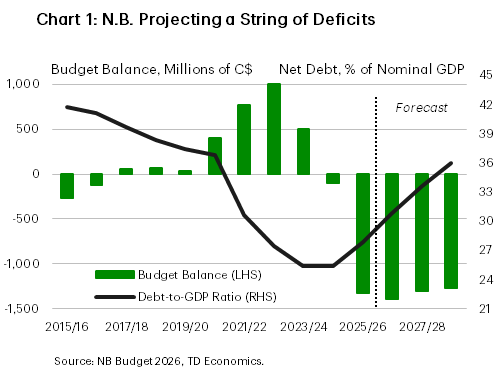

The Province of New Brunswick (N.B.) is projecting a $1.4 billion budget deficit for FY 2026/27 (or -2.7% of GDP). This forecast shows virtually no improvement from the revised $1.38 billion record deficit (-2.8% of GDP) now expected for the current fiscal year. The larger shortfalls reflect both weaker revenue momentum and continued spending pressures in core program areas. What’s more, the government opted to remove the $50 million annual contingency that was implemented only last year.

Policy changes in this budget are light. There had been widespread expectations that the government would push ahead with major spending rollbacks, but that didn’t materialize. Instead, the government announced a reduction in the size of the civil service (through attrition) by 12% over three years. Other highlights include new highway tolls on non-New Brunswick vehicles, a $9.9 billion investment for nuclear development, and sizeable investments in the health care sector. Taken together, these measures only go a small way toward alleviating deficit concerns over the next three years.

Revenue Growth Moderates Amid Slowing Economic Backdrop

Thanks in large part to a jump in federal transfers, total revenues in FY 2026/27 are projected to rise by a sturdy 5.6%. Personal and corporate tax revenue are expected to post modest gains, constrained in part by forecasts for subdued economic conditions. On that front, economic assumptions underlying the budget estimates are reasonable. The government is anticipating real GDP growth in 2026 to slow to 1.0% from an estimated gain of 1.3% in the year prior. Growth in 2027 is expected to strengthen a tenth of a percentage point before returning back close to the province’s steady state of around 1.3% over the longer haul. The slowing growth for the year ahead is attributed to a deceleration in population growth, moderating residential construction activity, and ongoing trade uncertainty.

These projections are slightly below our recent March forecast of around 1.3% this year and next. The budget has, however, adopted cautious assumptions around GDP inflation in 2026, leaving nominal GDP forecasts roughly a full percentage point lower than our own. In this regard, there may be some upside to the near-term revenue targets.

New Brunswick Economic Assumption

[ Percent Change Unless Otherwise Noted ]

| Budget 2026 | |||||

| Calendar Year | 2025 | 2026 | 2027 | 2028-30 | |

| Nominal GDP | 3.6 | 3.1 | 3.0 | 3.2 | |

| Real GDP | 1.3 | 1.0 | 1.1 | 1.3 | |

| Employment | 1.3 | 0.6 | 0.6 | 0.8 | |

| Unemployment Rate (%) | 7.1 | 6.9 | 6.7 | 6.8 | |

| Population | 1.3 | 0.3 | 0.3 | 0.8 | |

| Retail Trade | 4.9 | 2.4 | 2.6 | 2.9 | |

| CPI | 1.7 | 2.2 | 2.0 | 1.9 | |

Brisk Spending Gains in FY 26-27, More Modest Increases Beyond

On the opposite side of the ledger, expense growth is projected to expand at a 5.5% rate after last year’s robust 7.7% spending growth. New spending of $710 million is earmarked for the health care sector–the biggest contributor to new spending– with other focus areas including education and housing. Expense growth subsequently slows to an average of 2.5% per year over the remainder of the forecast horizon.

Meanwhile, the province has ramped up capital spending with a $1.47 billion plan for FY 2026/27, representing more than a 20% year-on-year gain. Capital spending growth is almost entirely focused on transportation infrastructure and health care.

Debt Burden Chugs Higher as Capital Spending Continues

New Brunswick’s net debt-to-GDP ratio is expected to breach 30% in FY 2026/27 as a modest gain in nominal GDP is outstripped by an increase in the level of debt. From there, the debt-to-GDP ratio is expected to continue grinding higher to 36% in FY 2028/29, or 10 percentage points higher than this year’s estimated debt ratio. Despite this rising trajectory, the government still boasts one of the lower debt ratios among the provinces and the lowest in the Atlantic. Meanwhile, total borrowing requirements for FY 2026/27 are forecast at $4.3 billion, an $800 million ramp-up from the last fiscal year.

Bottom Line

The New Brunswick government is projecting sizeable deficits for the foreseeable future as it continues to keep its foot on the spending pedal amid continued soft economic conditions. Achieving a sustained path back to balance will likely require either stronger economic growth, tighter spending controls and/or additional revenue measures in the years ahead.

New Brunswick Government Fiscal Position

[ Millions of C$ Unless Otherwise Noted ]

| Fiscal Year | 2025-26 | 2026-27 | 2027-28 | 2028-29 | |

| Revised | Budget | Plan | Plan | ||

| Revenues | 13,488 | 14,244 | 14,857 | 15,175 | |

| % Change | 1.7 | 5.6 | 4.3 | 2.1 | |

| Expenditures | 14,816 | 15,638 | 16,162 | 16,442 | |

| % Change | 8.4 | 5.5 | 3.4 | 1.7 | |

| Surplus (+)/Deficit (-) | -1,328 | -1,394 | -1,305 | -1,267 | |

| % of GDP | -2.7 | -2.7 | -2.5 | -2.3 | |

| Net Debt | 13,947 | 15,902 | 17,874 | 19,739 | |

| % of GDP | 27.9 | 30.8 | 33.6 | 36.0 | |

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: