2026 Manitoba Budget

Revenue-led Deficit Improvement

Rishi Sondhi, Economist | 416-983-8806

Date Published: March 24, 2026

- Category:

- Canada

- Government Finance & Policy

Highlights

- Manitoba’s deficit is projected to narrow sharply to $0.5 billion in FY 2026/27, the smallest shortfall among provinces so far this budget season, driven by a surge in revenues—particularly corporate tax receipts and federal transfers.

- Targeted tax relief is pledged, including the elimination of the PST on groceries and higher renter and homeowner credits. In particular, the elimination of provincial sales taxes on groceries could provide modest near-term support to household spending, at a fiscal cost.

- While a sizable capital plan could support the growth outlook, elevated debt levels and the highest debt servicing burden among provinces leave Manitoba more exposed should revenues disappoint.

Manitoba’s Budget 2026 aims to balance near-term stimulus with fiscal consolidation. The deficit is projected to narrow sharply to $0.5 billion in FY 2026/27 from $1.6 billion the year prior, driven by a sizeable revenue gain. At just 0.5% of GDP, the shortfall would be the smallest among provinces so far this budget season and well below the post–Global Financial Crisis average. The government remains committed to balancing the budget by FY 2027/28, though the debt burden remains elevated at 38.2% of GDP this fiscal year.

The budget delivers targeted tax relief for households, including higher renter and homeowner tax credits and the elimination of the PST on groceries. On the spending side, outlays remain focused on core services such as health and education.

Revenues to Jump This Year

Manitoba’s marquee new measure is its pledge to eliminate the 7% PST on groceries. Given that these expenses account for about 11% of a typical household’s spending basket, this measure could offer some inflation relief for households. It is expected to be in place by July 1st and is projected to cost the government some $32 million in revenues over a full year.

Alongside this measure, the government will also increase the Homeowners Affordability Tax Credit by $100 to $1,700. The credit will be reduced on a sliding scale for homes assessed at more than $1 million. Those with homes valued at more than $1.5 million would no longer receive any credit. Over a full year, this is estimated to cost the government about $29 million. The Rental Affordability Tax Credit will be boosted by $50 to $625 in FY 2026/27 and to $675 by FY 2027/28 at a full-year cost of about $10 million. Some revenue offset will come from measures to prevent the avoidance of land transfer tax payments.

The province expects sub-par real GDP growth of 1.5%, on average in 2026 and 2027 while nominal GDP growth averages 3.7%. Both forecasts are in line with our view.

Even with subdued economic growth expectations and tax relief measures, revenues are forecast to surge 10% in FY 2026/27. A big lift will come from federal transfers, which mainly reflects increases in equalization, health transfers and wildfire-related federal payments. However, income taxes are also slated to grow strongly, boosted by a surge in corporate tax revenues that’s driven by gains in business income. Retail sales tax revenues are forecast to grow more slowly, reflecting tax relief measures.

Manitoba Government Fiscal Position

[ Millions of C$ Unless Otherwise Noted ]

| Fiscal Year | 2025/26 Forecast |

2026/27 Budget |

|

| Revenues | 24,459 | 26,820 | |

| % Change | 0.5 | 9.7 | |

| Expenditures | 26,125 | 27,318 | |

| % Change | 2.5 | 4.6 | |

| Operating Surplus (+) / Deficit (-) | -1,666 | -498 | |

| % of GDP | -1.7 | -0.5 | |

| Net Debt | 38,057 | 39,714 | |

| % of GDP | 37.9 | 38.2 | |

Healthy Spending Growth Expected this Year

Total spending growth is pegged at a healthy 4.6% in FY 2026/27. Healthcare and education spending do the heavy lifting, with the former lifted by efforts to recruit and retain staff, and the latter supported by investments in the child-care work force.

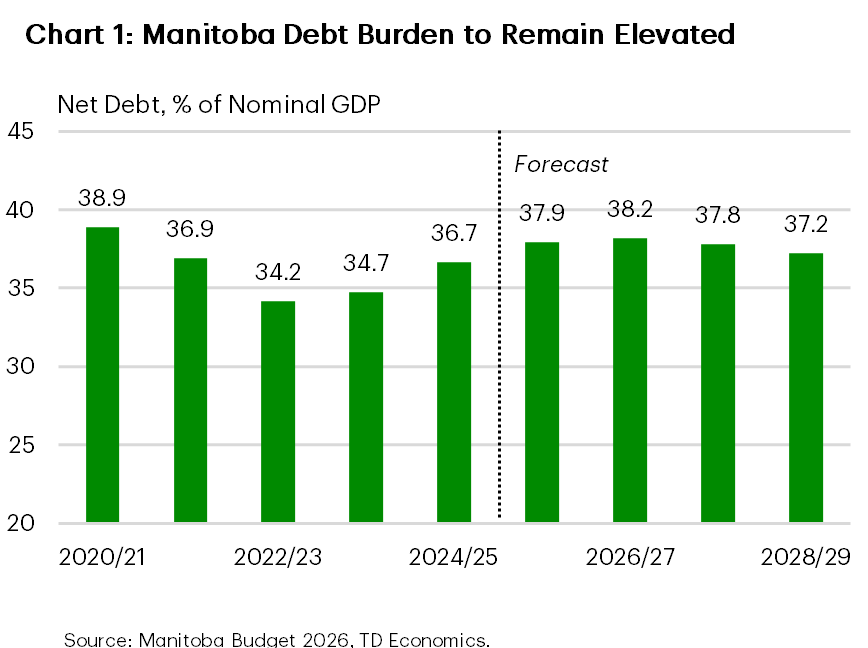

Debt Burden to Remain Elevated

Manitoba’s net debt-to-GDP ratio is expected to peak at 38.2% in FY 2026/27, before drifting lower toward 37% by FY 2028/29. This path reflects a combination of shrinking deficits and sustained nominal GDP growth. Capital outlays are seen as rising only 2% this year (though the level is elevated), with the recently released capital investment intentions survey flagging a softer 2026 showing. However, capital outlays are projected to rise aggressively thereafter, underpinning borrowing needs.

In FY 2026/27, the borrowing program totals roughly $4.2 billion, split between refinancing and new cash requirements. Debt servicing costs are expected to absorb close to 9% of revenues, the highest of any province so far this season.

Bottom Line

Manitoba’s plan to materially narrow its deficit next year relies on strong revenue growth. While much of that lift comes from federal transfers, the outlook also expects a sharp rebound in corporate tax receipts. Although recent Chinese tariff relief should provide some support to agri‑related businesses, seeing this gain may prove challenging against a highly uncertain backdrop—particularly as the government itself is forecasting subdued economic growth. Indeed, parts of the business sector were already under strain last year, with exports to the U.S. falling sharply.

The elimination of the PST on groceries may lower inflation and could provide a modest near-term lift to household spending, though at the expense of government revenues. A sizable capital plan could support near-term growth and offer longer-run productivity benefits. Nevertheless, higher debt-servicing costs increase the province’s vulnerability to adverse economic shocks and may gradually limit the fiscal space available for other expenditures.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: