The GVA’s Condo Market is Still Searching for a Floor

Rishi Sondhi, Economist | 416-983-8806

Paul Kim, Eonomic Analyst

Date Published: June 11, 2026

- Category:

- Canada

- Real Estate

Highlights

- Vancouver’s condo market remains under pressure, with weak demand and elevated supply expected to push prices lower through 2026.

- We forecast a roughly 15% peak-to-trough decline from the 2023 high by mid-2027, marking the deepest correction on record back to 2005. For 2026, prices should fall around 7-8% in Q4/Q4 terms, although we see some stabilization taking place in 2027.

- While severe by its own historical standards, Vancouver’s downturn should remain milder than Toronto’s, with prices expected to stay above pre-pandemic levels.

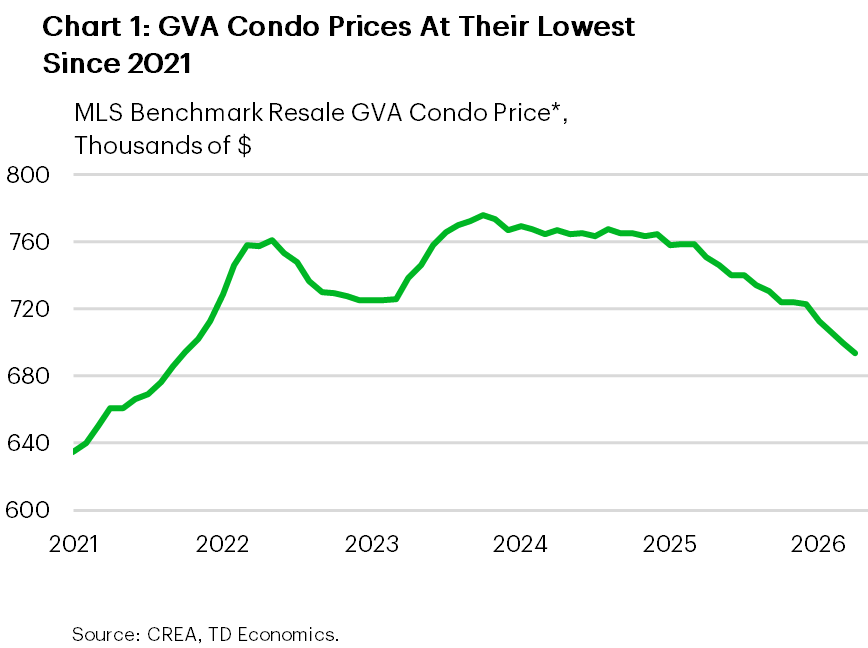

If it wasn’t for the Greater Toronto Area (GTA), Vancouver would probably have the dubious honor of hosting the softest major condo market in Canada. Indeed, Vancouver’s market has seen either flat or declining prices for nearly 4 years (Chart 1), and there’s likely more price downside to come. Vancouver’s market for new condos faces challenges although this note focuses on the resale market. The latter is a hugely important slice of the housing pie.

Tepid Activity in 2026

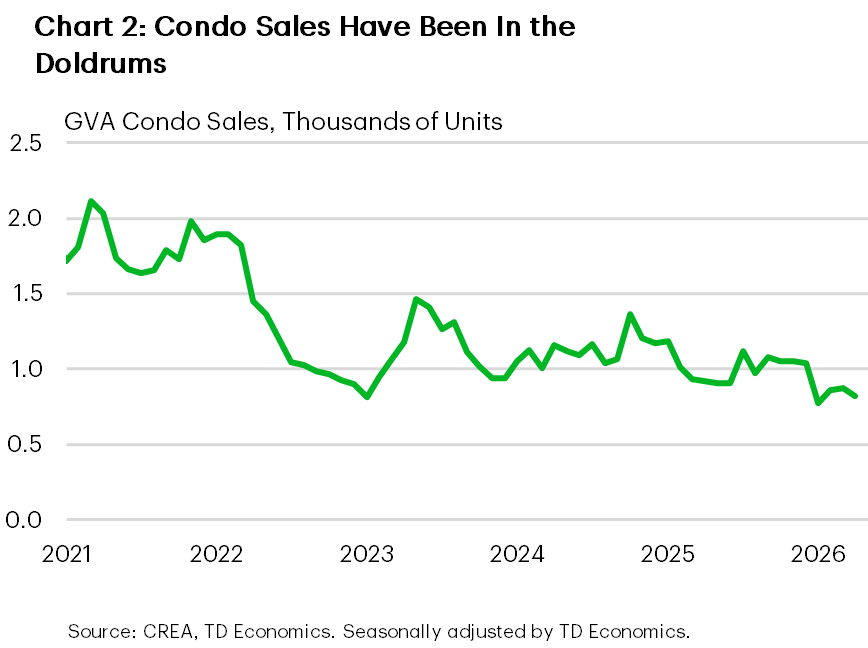

Condo demand remains muted (Chart 2). Sales in the first four months of the year fell 16% compared to last year, reaching their lowest (non-pandemic) levels since late-2018/early-2019. Back then, the combination of rate hikes by the BoC, tighter mortgage stress tests, and provincial measures aimed at cooling activity and improving affordability caused a significant decline in sales from their 2017 peak.

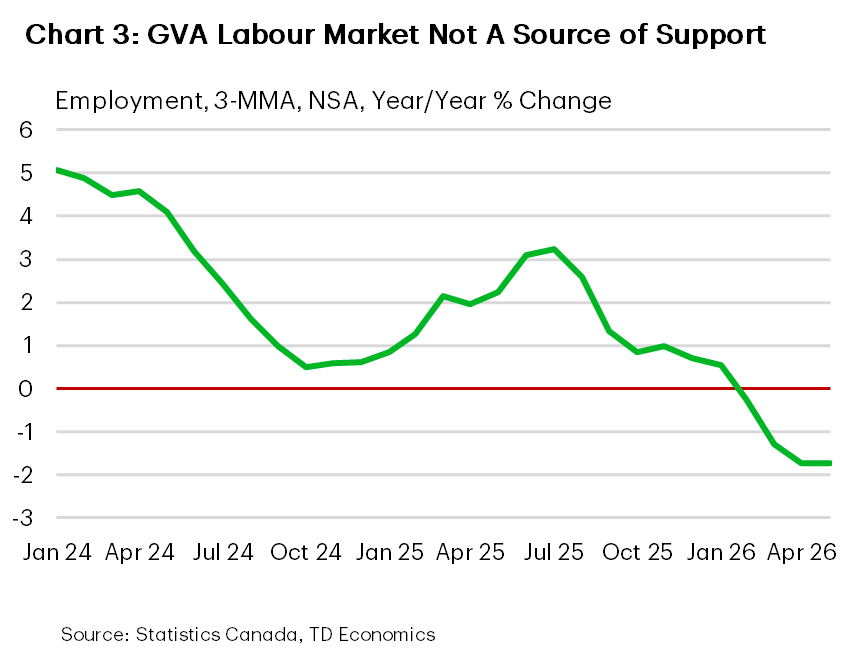

A subdued GVA labour market has likely been an important headwind for demand. Since last June, employment is down about 2% (-32.5k positions), impacted by a declining labour force (Chart 3). However, the unemployment rate has also risen about 0.5 ppts over that time, hitting its highest level since early 2025 in May (6.7% on a 3-month moving average basis). The trade war has weighed, with hiring pullbacks in manufacturing, wholesale/retail trade, and transportation/warehousing. Meanwhile, B.C.’s depressed housing market has restrained hiring in finance/insurance/real estate.

The upward pressure on borrowing rates since the onset of the Middle East conflict has also probably pressured activity. Note that our modelling suggests that markets in B.C. have historically been the most sensitive of any province to rate increases, as they interact with a generally poor affordability backdrop. There’s also the likelihood that falling prices are keeping buyers sidelined as they wait for a better deal to emerge.

Benchmark prices have been a touch more resilient. They dropped slightly from their October 2023 peak through early 2025 before giving way to more pronounced declines. The latter has been driven by tempered demand that’s strongly tilted market balances in the favour of buyers. Indeed, the sales-to-active listings ratio (a measure of the demand/supply balance), is some 50% below its long-term average. On a year-to-date, year-on-year basis, prices are down 7%.

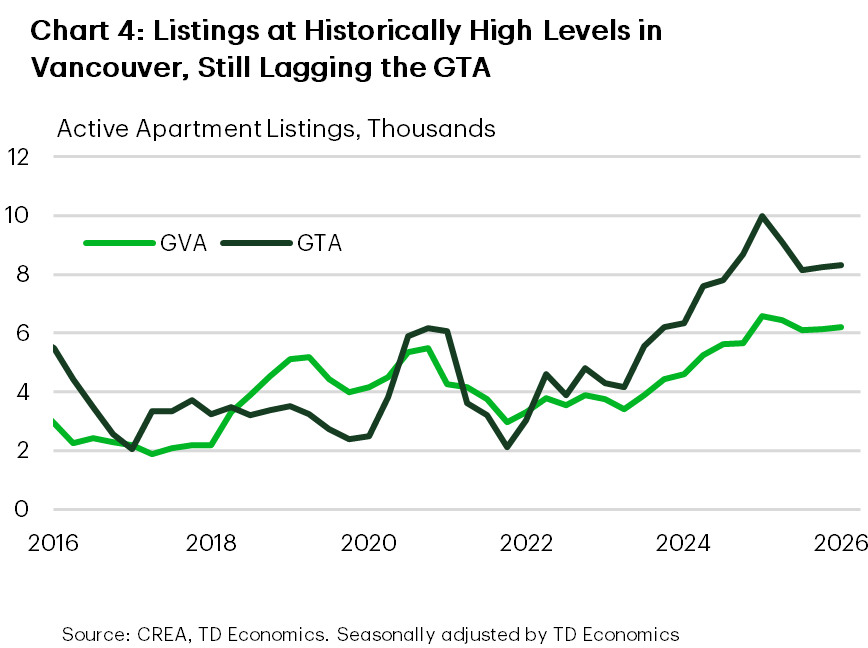

A comparison with Toronto can add some helpful context around Vancouver’s supply situation. The GTA condo market is grappling with a historically high level of listings. Falling rents and higher carrying costs have put pressure on investors, prompting many to list their properties. What’s more, condo completions had been elevated (although are rapidly retrenching now). The one-two punch of chilly demand and high supply has sent GTA condo prices down about 25% from their peak.

In contrast, Vancouver’s condo stock is more heavily skewed toward end-users rather than investors. This point is driven home by the fact that condos account for about 50% of resales in a typical month. Affordability constraints in the broader housing market make condos the more attainable entry point for ownership, underpinning a less volatile base for demand relative to Toronto, where investors have played a larger role in driving recent trends.

Of course, investors in the GVA market have seen the same pressures as in Toronto and accordingly, listings have increased to levels that are at the higher end of historical ranges. However, they have not touched the same elevated highs observed in Toronto (Chart 4), even with a higher level of condo completions in Vancouver.

Looking ahead to the next few quarters, we expect Vancouver condo prices to continue declining. Specifically, we forecast a roughly 7-8% decline on a Q4/Q4 percent change basis in 2026. This follows the initial adjustment already underway and reflects the ongoing imbalance between low demand levels and elevated supply.

Next Year Should See Stabilization

Conditions are expected to improve modestly in 2027, driven by several factors that should gradually support demand. Declining prices through 2026 will bring improved affordability, which should boost activity. At the same time, we see scope for yields to head lower in the second half of the year. Additionally, pent-up demand accumulated during the downturn should support the market.

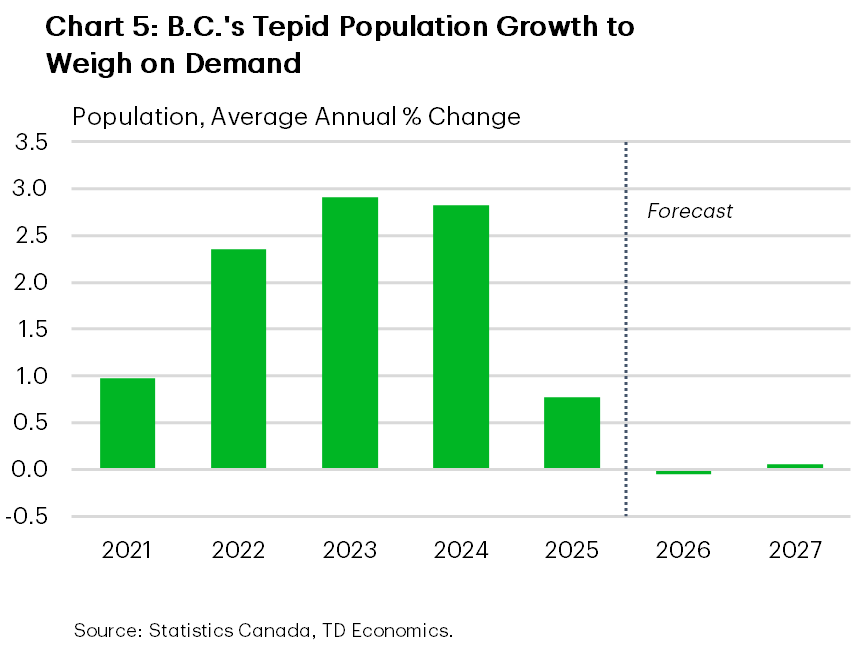

However, Vancouver’s recovery will likely be tempered by still-soft population trends in the province (Chart 5). And, while hiring should gain some traction next year alongside a firming in economic activity, labour market conditions are likely to remain muted. Together, these factors point to only a gradual and modest strengthening in sales over the next 12-18 months. Indeed, sales are likely to hold well below 10-year averages through next year.

On the supply side, rising sales growth should gradually eat into elevated inventory levels, helping rebalance the market over time. What’s more, condo completions are falling quickly, adding less upside pressure to supply, and this trend should continue into next year.

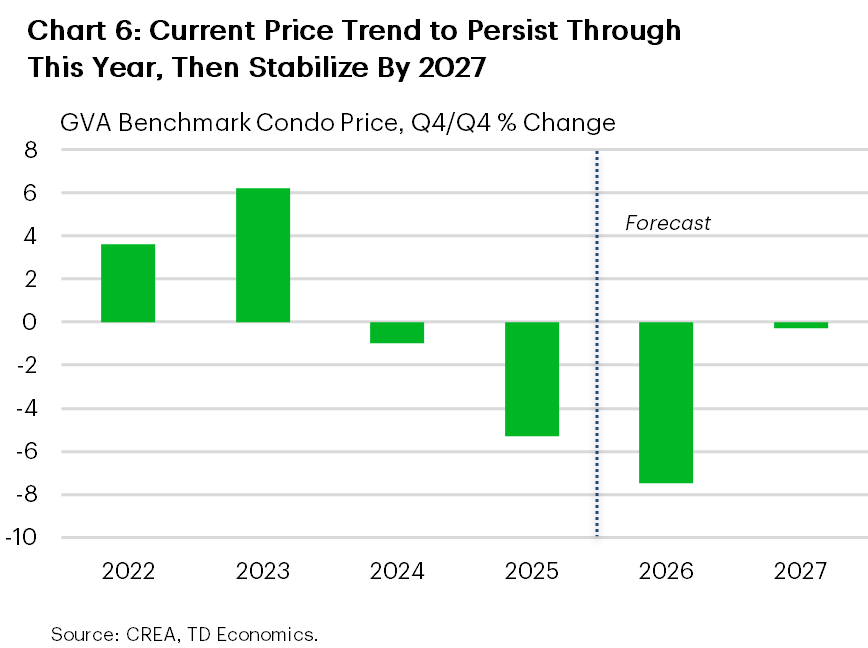

Putting the pieces together, we see condo prices stabilizing in the first half of next year, before flattening in 2027H2. For the year overall, condo prices are likely to be about flat in Q4/Q4 terms (Chart 6).

Combining our 2026 and 2027 views, Vancouver condo prices could fall by approximately 15% from their 2023 peak, marking the steepest decline since at least 2005 (the first period of available data).

Even so, by the end of the adjustment, benchmark condo prices in Vancouver will likely be above their pre-pandemic level. This stands in contrast to Toronto, where prices are projected to fall meaningfully below pre-pandemic benchmarks, underscoring the less extreme (but still pronounced) nature of Vancouver’s downturn.

Bottom Line

Vancouver’s condo market is in the midst of a notable correction, though one that appears less severe than in Toronto. Sales are down and prices are falling, reflecting softer demand and elevated supply.

We expect condo prices to decline further in 2026 before stabilizing in 2027. Even so, prices will likely remain above pre-pandemic levels, compared to well below in Toronto. As affordability improves and demand gradually returns, the beginnings of a more durable recovery should take shape in 2027, albeit one tempered by slower population growth.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: