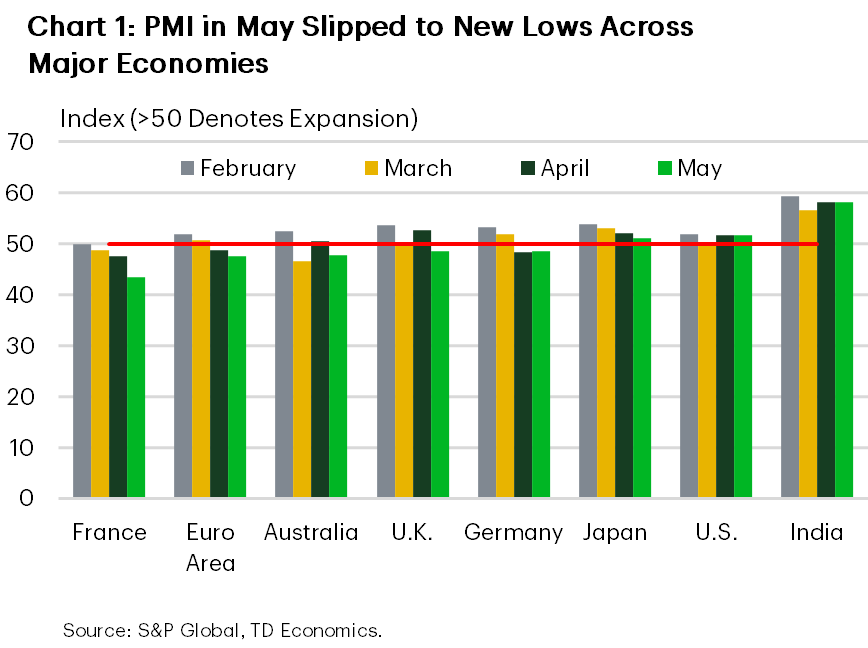

- In the euro area, the composite PMI slid to its lowest level in nearly three years. Services slumped to its lowest level in over five years, while manufacturing is still in growth territory, but output slowed to 51.0, a 4-month low. Input cost inflation hit a ~3½-year high and selling prices also accelerated (fastest in 38 months), underscoring a stagflationary backdrop. This is the second month in as row that the composite PMI has been below the contractionary threshold of 50 in the euro area.

- In France, the composite PMI plunged to a 66-month low, reflecting a steep contraction in output across services, which also hit a 66-month low, and manufacturing output, which reached its lowest level in six months. War-driven surges in energy costs crushed demand and lifted input and output price indices to their highest level in at least three years, indicating intense inflationary pressure even as activity slumps. This was a significant surprise as consensus expectations were for France to hold around its April level.

- In Germany, the composite PMI edged higher but remained below 50, signaling a second month of mild contraction. Input costs rose at the fastest pace in about 3½ years, while output price inflation eased slightly from April’s high, suggesting firms are absorbing more costs in their margins.

- For the United Kingdom, the composite PMI fell below 50 for the first time since April 2025. This downturn was led by a steep decline in services, even as manufacturing output rose slightly, reaching a three-month high. Input cost inflation remained steep (just below April’s 41-month peak), while output price inflation moderated marginally, still implying strong pass-through of costs to customers. As in the case for France, this was a big surprise – markets were generally expecting UK PMI to remain above 50 this month.

- In Japan, the composite PMI eased to 51.1, a five-month low, yet still in modest expansion. Services stagnated at exactly 50.0, ending a 13-month expansion, while manufacturing output growth remained solid, just below April’s 12-year high. Input costs rose at the quickest rate since late 2022, and selling prices climbed at a record pace (nearly 19-year survey high), in a sign of inflation pass-through.

- In Australia, the composite PMI fell back to 47.8, after briefly entering expansionary territory in April, making its second decline in three months. Both services and manufacturing output weakened, as new orders slumped to the worst in roughly 4½ years. Input price inflation remained elevated (near the highest since 2022), while output price inflation, though still strong, was comparatively softer – pointing to margin pressures alongside weak demand.

- In the United States, the data was unchanged in May at 51.7. The services and manufacturing sub-components also barely moved. Both remain in expansionary territory, albeit somewhat subdued in services, while the manufacturing index is at a four-year high. As in other economies, U.S. data for May showed a surge in input costs, with the input price index reaching its highest level since November 2022, driven largely by manufacturing, and the output price index remained elevated.

- In India, the composite PMI held at 58.1, sustaining robust growth (22nd straight month of expansion) and bucking the global slowdown. Input costs ticked higher (composite input inflation at its second-highest in roughly 3 years), but output price inflation slowed to a four-month low as firms limited price hikes to support demand – underscoring India’s relative resilience.

Key Implications

- May’s PMI releases for key global economies point to a broad-based loss of momentum in global activity. Purchasing manager confidence in many economies reached multi-year lows in composite or services indices and major economies in Europe registered significant downside surprises. At the same time, input cost pressures have reignited, reaching multi-year highs. Output price indexes remain elevated too, though some show slight moderation as companies appear to absorb some of the cost increases. This combination of weakening output and resurgent costs raises concerns of a potential stagflationary phase if war-driven disruptions endure.

- The euro area and UK in particular look to be at risk of sliding toward a stagflationary quagmire, with contracting activity and stubbornly high price pressures. This complicates near-term policy for the ECB and BoE: further rate hikes could deepen the downturn, but pausing risks letting inflation expectations drift up. The European PMI data hint that Q2 GDP may contract even as inflation remains elevated. In effect, with their economies facing a faltering recovery and renewed cost shocks, the ECB and BoE are confronted with exceptionally tough trade-offs for monetary policy in the months ahead.

- The one silver lining in this release is that, somewhat surprisingly, economies in Asia seem to be holding up better than in Europe. Japan and India remain in expansionary territory despite the significant headwinds. The U.S. economy is also proving resilient, as it is expected to hold up better in the face of higher oil prices (see report).

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: