For Japan, Fiscal Credibility and Nominal Growth

Date Published: March 5, 2026

- Category:

- Global

- Asia

- Global Economics

Highlights

- A decisive election outcome earlier this month expands the government’s scope to pursue fiscal and industrial policy.

- A sustained recovery in the yen and in Japanese government bond yields hinges on successful execution of the government’s fiscal plan and building credibility.

- Above all, Japan’s fiscal strategy relies on stronger nominal GDP growth to lift revenues, creating asymmetric risks if growth underperforms.

Prime Minister Sanae Takaichi has been in office only since October last year, but her first five months have been unusually eventful. The early period of the new government was marked by market volatility. Budget proposals floated late last year raised concerns about widening deficits and heavier borrowing needs, particularly amid fears that additional spending concessions would be required to secure opposition support. An election pledge to suspend Japan’s consumption tax further amplified borrowing expectations, triggering renewed turbulence in bond markets in late January (see our commentary). Against this backdrop, an early February election was called.

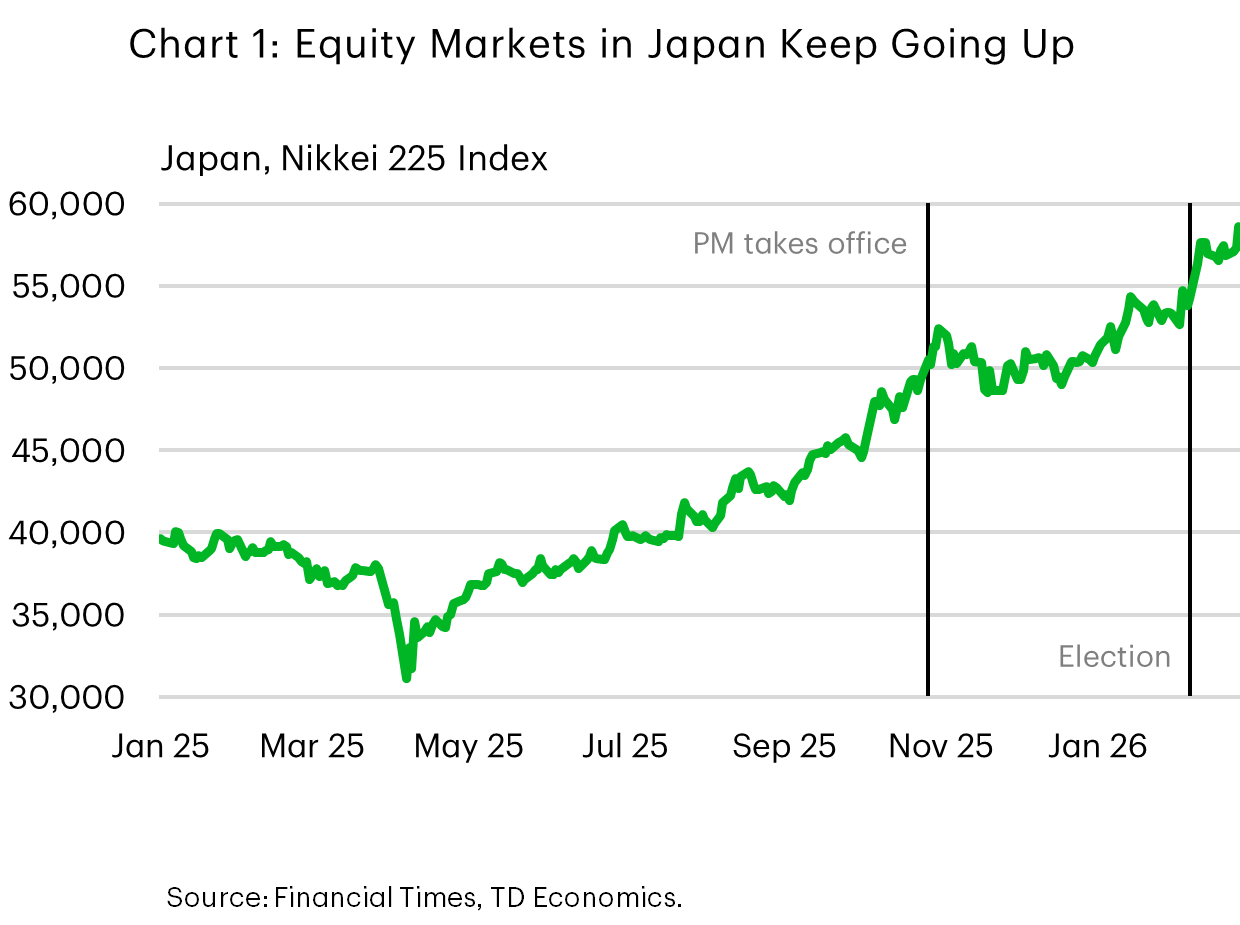

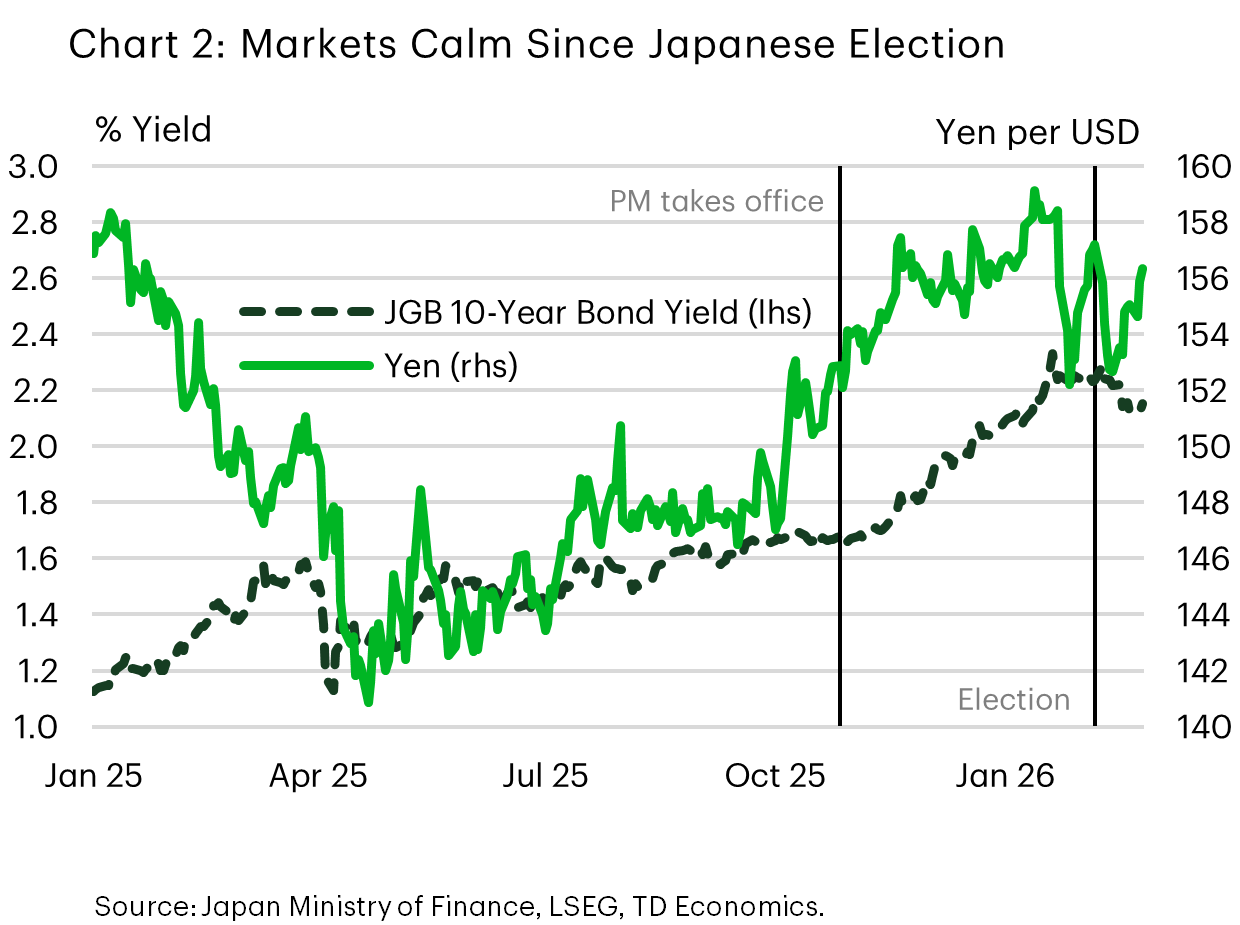

Since then, Prime Minister Takaichi’s landslide victory has delivered a parliamentary supermajority, materially easing market concerns (see our commentary). Equity markets extended their rally, the yen bounced back from multi-decade lows, and government bond yields retreated (Charts 1 and 2). The strengthened mandate increases the likelihood of followthrough on a clear and focused fiscal agenda, bolstering investor confidence that growth oriented priorities will support the economy. Execution risk remains high, but for now global investors appear willing to give the new government the benefit of the doubt.

More spending, with a strong emphasis on credibility

The recent market rally has occurred despite a FY2026 budget submission in February that was unchanged from the draft approved by cabinet in December 2025. Investors have nevertheless reacted favorably to the government’s commitment to keep new JGB issuance below ¥30 trillion, to maintain a declining bond financing ratio, and to restore a primary budget surplus in the medium-term. The government’s core argument to markets is that fiscal expansion can coexist with discipline if supported by a sustained acceleration in nominal growth, which has become the central benchmark for policy success. Market behavior in recent weeks suggests a willingness to tolerate greater fiscal ambition, provided financing remains credible and debt management signals are clear.

As shown in Table 1, spending increases in the FY2026 budget are concentrated in social security, defense, and growth oriented investment—most notably in semiconductors, AI, and the green transition. While headline spending is set to reach a record level, a large share of the increase reflects higher debt service costs, projected to rise by roughly ¥2.5 trillion. General expenditure—the component most relevant for near term growth—accounts for only about one third of the total increase.

Table 1: FY2026 vs FY2025 Initial Budget

| Item | FY2025 | FY2026 | Change | Notes |

| General expenditure (一般歳出) | ¥68.2 tn | ¥70.2 tn | +¥2.0 tn | Policy-relevant spending |

| └ Social security (inflation & wage-linked) | ¥38.3 tn | ¥39.1 tn | +¥0.8 tn | Pensions, medical fees, benefits |

| └ Defense (Defense Buildup Program) | ¥8.5 tn | ¥8.8–8.9 tn | +¥0.3–0.4 tn | Scheduled multi-year increase |

| └ Industrial policy (AI, semiconductors, GX)* | ≈¥1.5 tn | ≈¥2.0 tn | Increase | Growth & economic security |

| └ Child & family support* | ≈¥0.4 tn | ≈¥0.7 tn | Increase | Childcare & education |

| └ Economic security & supply chains* | ≈¥0.3 tn | ≈¥0.5 tn | Increase | Strategic goods & resilience |

| Transfers to local governments | ¥19.1 tn | ≈¥20.9 tn | +≈¥1.8 tn | Local allocation tax grants |

| Debt service (interest & redemption) | ¥10.5 tn | ≈¥13.0 tn | +≈¥2.5 tn | Higher yields & rollover |

| Total general-account spending | ¥115.5 tn | ¥122.3 tn | +¥6.8 tn | Headline budget size |

| Tax and other revenue | ¥78.4 tn | ¥83.7 tn | +¥5.3 tn | Nominal income & profit growth |

| Deficit / net financing need | ¥28.6 tn | ¥29.6 tn | +¥1.0 tn | New JGB issuance, highlighted as below 30tn |

A critical assumption underpinning the budget’s deficit projection is faster nominal growth, which is expected to boost revenues through higher wages and profits. Given Japan’s historically weak nominal GDP backdrop, this creates a one sided fiscal risk: underperformance in nominal growth is more likely than an upside surprise. Even modest shortfalls in wage or profit growth would put pressure on the government’s commitment to keep new JGB issuance below ¥30 trillion.

The sharp increase in revenue warrants closer scrutiny, particularly given official communication that it largely reflects organic growth in the tax base rather than new tax measures. The ¥5.3 trillion increase amounts to nearly a 7% rise from FY2025. With inflation running between 2–3% recently and trend real GDP growth around 1%, we would expect nominal GDP growth of roughly 3–4% annually. This aligns with Japan’s Cabinet Office outlook, which assumes nominal GDP growth of 3.4% in FY2026 – reasonable given recent trends, but not high enough to explain the full increase in revenue.

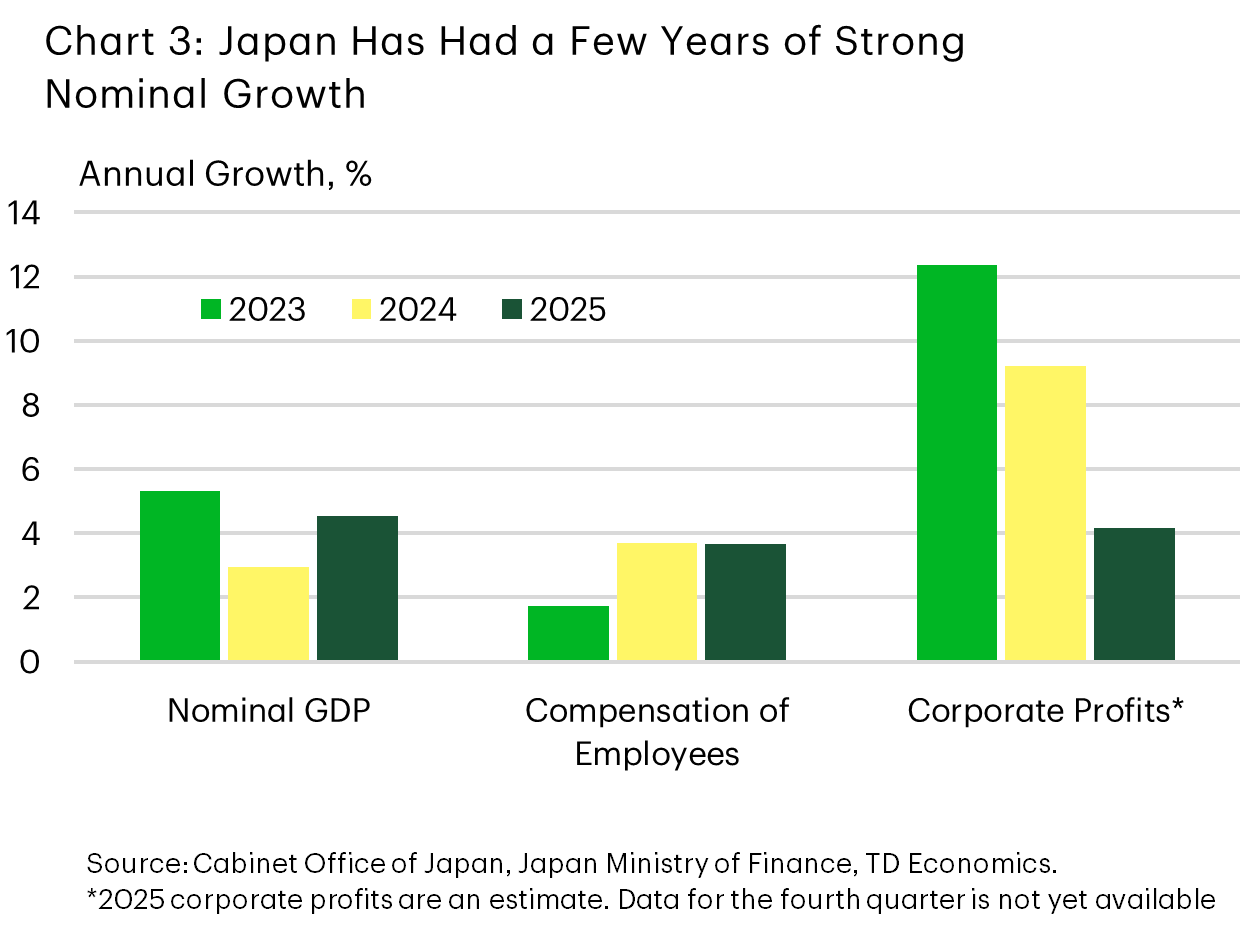

That said, several measures in the budget do raise revenue. Some special tax measures are being rolled back, tourism related taxes are increasing, and visa and residency fees are rising. These measures may generate around ¥1.5 trillion in additional revenue, leaving about ¥3.8 trillion—or 4.8%—to be explained by growth in the nominal tax base. This exceeds our expectations for nominal GDP growth, but wages and profits can outpace overall GDP in an environment of elevated inflation and fiscal expansion. While this creates an asymmetric vulnerability, the revenue forecast is plausible. Corporate profits have outperformed nominal GDP over the past three years, wage growth has been strong, and expectations are for these trends to continue (Chart 3).

Modest near-term change, wider distribution of risks

One potential upside risk to growth stems from the budget itself. Some forecasters have begun nudging up their near term outlooks in anticipation of postelection stimulus. Over time, several policy elements—notably the scaleup in industrial policy and supply chain investment, both central election themes—could support productivity gains and strengthen resilience to future supply shocks. In the near term, however, the growth impact is driven primarily by direct fiscal outlays. Based on the FY2026 budget, the resulting fiscal impulse from higher general expenditures is modest, at roughly +0.2 percentage points of GDP. This implies at most a similar upward revision to our 2026 real GDP growth forecast, which we had at 0.6% in our December forecast.

Importantly, the budget does not yet incorporate the government’s flagship election pledge: a two year suspension of the VAT on food. The IMF has cautioned against this measure, citing its untargeted design and the associated loss of fiscal space. While the government appears determined to proceed, the key test for markets will be whether it can do so without additional bond issuance, as promised. We expect further details on the VAT proposal to emerge later this year through a process separate from the core budget, possibly as early as late summer or early fall.

The government has established a multiparty national council to discuss the tax cut, which began deliberations on February 26. The Prime Minister has indicated that the council will deliver an interim report before the summer, paving the way for legislation that would likely implement the tax cut in the next fiscal year, though potentially sooner.

The macroeconomic impact of this measure is difficult to quantify. At an estimated cost of ¥5 trillion—roughly 1% of GDP for two years—the tax cut could represent a sizable upside to consumption growth. However, the associated revenue offset mechanisms may blunt its stimulus effect. If the government adheres to its objective of implementing the tax suspension without additional borrowing, the policy may function more as relief from cost of living pressures than as meaningful fiscal stimulus. It is difficult to be certain how much the revenue offset would reduce the growth impact – some of the revenue options the government has floated, such as selling government assets and foreign exchange reserves, would have a limited impact on growth, while other options, such as ending or limiting certain corporate subsidies and tax breaks, would reduce growth.

For the Bank of Japan, more room tactically, more complexity politically

Placing Japan’s debt-to-GDP trajectory on a sustained downward path will require maintaining this year’s elevated nominal growth over the long run. Sustainable debt dynamics require nominal GDP growth to exceed the nominal interest rate on government debt once primary balance is achieved. Japan’s 10 year government bond yield has risen to just over 2%, while the 40 year yield stands near 3.5%. Although Japan’s average interest cost on outstanding debt remains below 1%—reflecting legacy issuance at very low yields—the effective rate will rise as maturing debt is refinanced.

The government projects nominal interest payments to double from roughly ¥10 trillion in FY2025 to over ¥20 trillion by FY2029. Assuming new issuance occurs at an average yield of 3%, the effective interest rate could approach 2% by 2029 and continue rising thereafter. While nominal GDP growth may outpace borrowing costs in the near term, fiscal consolidation pressures will intensify as higher yield debt replaces legacy issuance.

The current yield environment assumes short term policy rates peak around 1-1.5% and inflation remains near the Bank of Japan’s 2% target, which it reached last month. While underlying inflation remains firm, headline and core measures softened sharply in January. This moderation affords the BoJ greater tactical flexibility, reducing pressure to tighten policy rapidly in the absence of renewed strength in wages or prices. As a result, the next rate hike is increasingly likely to be delayed until June or later, even as market pricing still leans toward an April move.

The government’s nomination of two widely perceived dovish academics to upcoming BoJ board vacancies has reinforced expectations that policy normalization will proceed more gradually. This shift helps explain why the yen retraced part of its post‑election gains in late February (Chart 2). With the currency still hovering near historically weak levels, authorities have reiterated their commitment to close coordination with U.S. counterparts, keeping the risk of foreign‑exchange intervention in focus should market moves become disorderly.

Bottom line

Japan’s super majority mandate increases the likelihood of a sustained push toward higher nominal growth through fiscal, defense, and industrial policy, and is likely to support upward revisions to growth forecasts. However, execution and credibility are now central to market outcomes. The key question is whether policy implementation can anchor expectations and limit volatility in bond and foreign exchange markets.

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: