Beyond Silicon Valley

Technology Industries Now a Global Phenomenon

Fotios Raptis, Senior Economist | 416-982-2556

Yasmine El Baba, Research Analyst | 416-415-0881

Date Published: December 19, 2018

- Category:

- Global

- Asia

- Global Economics

Highlights

- Although Silicon Valley continues to be the top destination for tech talent and financing, innovation hubs in other U.S. and international cities are offering competitive alternatives.

- Canadian cities are among the competitive alternatives, and are research leaders in fintech, artificial intelligence, robotics, and manufacturing. The innovation ecosystems in Toronto and Montreal are attracting global attention, and have become hotbeds for venture capital in recent years.

- But, the big story has been the rise of technology hubs in the developing world. Lower costs, access to large talent pools, and a shorter window to the commercialization of new discoveries are the main drivers of the broadening out of innovation centers to cities in China, India, and other developing economies.

- China’s government-driven innovation agenda, codified in its China 2025 plan, has accelerated its drive to become a serious global competitor to Silicon Valley. However, China’s tech industry faces a number of challenges that are likely to hold the pace of progress in check, such as the ongoing gap between efficiency and reputable quality, the lack of strong intellectual property laws, a poor compliance record with regard to WTO regulations, and a heavy reliance on government spending during an era of slowing economic growth, and thus slowing government revenue growth. The irony is that recent trade tensions between the U.S. and China to address these concerns may ultimately serve to help accelerate China’s innovation agenda if a convincing deal on intellectual property protections is achieved.

- More innovation is often viewed as unambiguously positive for future economic growth. Trade is often a means of knowledge transfer that can help less developed regions of the world catch up, lifting all boats. However, there are a few challenges, namely the potential for job losses and the exacerbation of existing income inequality, that have to be managed by policymakers in order to ensure that we reap the full benefits from new discoveries.

When one thinks of global technology leadership, Silicon Valley first comes to mind. Indeed, no other technology hub in the world shares its record of birthing so many new technologies and successful industries. Over the decades, tremendous growth has dramatically transformed this part of California, attracting high skilled workers where average wages far outstretch the nation as a whole. But, the rapid growth and reach of the technology sector is no longer contained within the confines of Silicon Valley. Other locales in the U.S. and international cities are offering the advantage of lower costs, alongside greater access to large and diverse talent pools.

This report is the first in a series on innovation that TD Economics plans on publishing in the weeks ahead. The focus is to describe the process of how innovation industries are spreading around the globe, and the opportunities and challenges that come with it. For instance, investments in a number of emerging market economies are bearing fruit from broadening technology hubs, particularly in China, where the government has targeted innovation as a critical part of its growth strategy for the decades to come. Within advanced economies, technology clusters have been gaining stronger footings within Toronto, Tokyo, London, and New York. The prospect for increased collaboration and enhanced trade is even evidenced within trade pacts, such as the CPTPP that comes into force in Canada at the end of this year. However, with rapid technology evolution comes social challenges. Policymakers have an important role to play in order to ensure an equal distribution of gains, while limiting disruption as much as is feasible. This theme will be fully addressed in an upcoming report.

Measuring regional hotbeds of innovation

Admittedly, pinning down the leading global technology hubs is a complicated task for a couple important reasons. First, there is no precise definition of what constitutes a “hub”, which raises difficulties in terms of measuring performance. One definition is a cluster or community – informal or otherwise – that fosters innovation for technology start-up companies. But, that leaves considerable scope for interpretation. Second, another challenge relates to a lack of hard data. Some of the most commonly used measures are: growth in tech talent, employment in tech industry as per state based statistics, venture capital flows, market-cap of tech giants, spending on research and development, and the availability of a proficient labor force and leadership. However, there is no data set that is both complete and comparable across regions.

Table 1: KPMG Survey of Leading Technology Innovation Hubs over the Next Four Years, 2018 vs. 2014 |

||

| Ranking | 2014 Responses | 2018 Responses |

| 1 | Shanghai, China | Shanghai, China |

| 2 | Tokyo, Japan | Tokyo, Japan |

| 3 | Beijing, China | London, UK / New York, U.S. |

| 4 | New York, U.S. | Beijing, China/ Singapore |

| 5 | Seoul, South Korea | Seoul, South Korea |

| 6 | London, UK | Bengaluru, India/ Tel Aviv, Israel |

| 7 | Mumbai, India | Berlin, Germany |

| 8 | Tel Aviv, Israel/Hong Kong, China | Sydney, Australia |

| 9 | Boston, U.S. | Boston, U.S/ Chicago, U.S. / Toronto, Canada |

| 10 | San Francisco, U.S. | Hong Kong, China/Shenzhen, China |

| Note: In 2018 the question changed to: In addition to Silicon Valley/San Francisco what three cities will be seen as leading technology innovation hub over the next 4 years? Source: KPMG (The Changing Landscape of Disruptive Technologies, 2014 & 2018), TD Economics |

||

In order to fill the data void, a number of organizations publish the results from surveys and benchmarking exercises of the global technology industry. These include KPMG’s annual global tech innovation survey that assesses the views of more than 750 global technology industry leaders, and CB Insights that groups technology centers into categories (i.e., established heavyweights, high-growth and up-and-comers).1,2 The World Economic Forum and Savills UK work around global data limitations to carry out benchmarking exercises based on subjective views on what are seen to be the key factors driving innovation.

While not providing a definitive picture, a number of themes fall out of these surveys:

- Innovation hubs dot the global map – led by Silicon Valley, the U.S. still tops the list of virtually all rankings of world-leading tech regions. However, other countries have been busy replicating America’s tech innovation blueprint and are not that far behind. For example, in the 2018 KPMG survey of executives, China continued to rank second in terms of world leading innovation hub, followed by Tokyo, Japan. The UK jumped significantly to rank fourth alongside New York. Another survey that adds credence to this view is CB Insights and the Focus Report by Expert Market.3

- U.S. strength goes well beyond Silicon Valley – Silicon Valley remains a perennial leader, but a number of U.S. centers occupy the upper end of most international rankings, including Austin, New York, Boston, Washington, and Chicago.

- Canadian innovation hubs have been gaining ground on global leaders - While Toronto was not part of the discussion a few years ago, it now enjoys a top-ten ranking in most surveys (Table 1). CB Insights has placed the city in its “high growth hub” category along with Shanghai and Tokyo.

- The dynamism within developing economies extends well beyond China – Although Shenzhen and other Chinese cities stand out, Bengaluru, India and cities elsewhere in developing economies are shooting up on global innovation hub charts.

- Specialization a secret of success – many technology industries are gaining strength in the tech world by focusing on specific areas, taking advantage of what makes them unique.

U.S. tech is more than just Silicon Valley

Nowhere is this changing landscape more evident than in the powerhouse U.S. market. Undeniably, Silicon Valley still stands its ground as the world’s largest tech hub, fueling global innovation. As shown in surveys, the Valley ranks highest among all up-and-coming tech hubs. It’s home to some of the world’s largest tech companies, such as Apple, Facebook, Google, Netflix, and Airbnb. Moreover, Silicon Valley continues to attract about half of all U.S. venture funds. However, as it fills with tech giants, its high barriers to entry make it less accessible to startups.

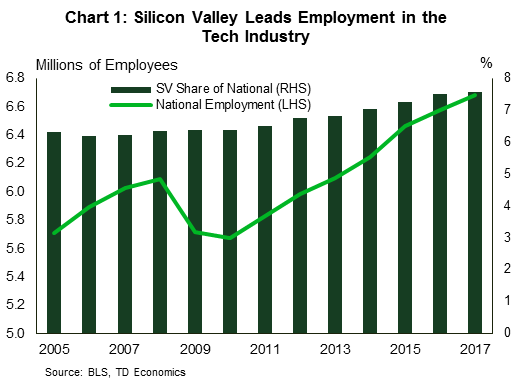

Nationwide employment in various tech sectors has been growing, but is yet to outpace employment in Silicon Valley. Although employment growth in Silicon Valley has slowed in the past two years, it still remains the leading employer of tech talent in the U.S. (Chart 1). That said, momentum may have started to shift as other centers become more attractive to tech talent.

Rising net tech jobs in Silicon Valley conceals outflows on a gross basis. In 2015, Silicon Valley lost an average of 832 people a month.4 Since then, the outflow has more than doubled; an average of 2,548 people a month left Silicon Valley in 2016. In August 2017, Facebook and Amazon set up R&D offices next to the best tech universities in Boston to recruit new graduates. Boston has a large number of tech-centric venture capital firms, as does New York City. And, according to the Office of the New York State Comptroller, employment in NYC’s tech sector increased by 57% between 2010 and 2016, equivalent to an additional 46,900 jobs.5 Furthermore, the number of firms in the industry reached 7,600 in 2016, up 23% since 2010. Washington, DC is also nurturing a strong tech culture, home to more than a thousand startups. More recently, Amazon announced that its second headquarters (dubbed HQ2) would be split between Long Island, New York and Crystal City, Virginia. Employment gains of 25,000 are expected in each city over the next 17 years, giving local technology industries a big boost. Last but not least, Apple announced a major expansion to other U.S. cities, including a $1 bn investment for a new campus in Austin, Texas.6

There are a number of factors driving capital, tech talent, and startups away from Silicon Valley and into other cities within the U.S. and around the world. One such factor is that the cost of business is significantly cheaper elsewhere. Silicon Valley and the Bay Area boast some of the highest housing and commercial real estate costs in the world. Put simply, there is not enough affordable housing to meet the demand, resulting in moderate and low income households being priced out of the region. Transportation is another challenge in the leading tech hub, where the average commute time is 72 minutes, imposing both a direct and an indirect economic cost on the city.7

Canadian cities in the spotlight

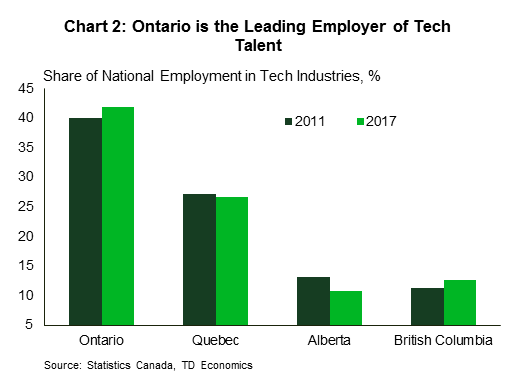

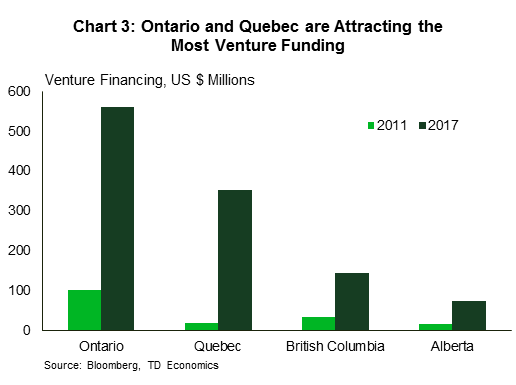

Canada’s largest urban centers are also becoming more attractive to innovation industries. Tech employment remains highest in Ontario and Quebec, and is on the rise in Western Canada (Chart 2). Global recognition is attracting investor interest in Canadian cities (Chart 3). The Greater Toronto Area continues to attract the most funding, but Montreal is not far behind. Canada’s largest cities have specialized in different fields and developed whole ecosystems designed to attract and sustain startups. Montreal is widely recognized for having the largest concentration of AI research. As it fiercely competes with Toronto and Montreal, Vancouver has grown a tech hub identity of its own, buoyed by its connection to international hubs such as Seattle and Silicon Valley and the entrepreneurial drive of residents.8

Still, Canada’s most established and highest ranked tech hub is Toronto. Toronto forms the core of a provincial innovation corridor that extends from Kitchener-Waterloo through Cambridge and the GTA, and up to the Ottawa Valley. This corridor links tech firms to world-class academic research centers, talent pools, connective infrastructure, and venture financing. There is a lot of diversity within this tech industry corridor, with emphasis on automotive tech, security, big data, and machine learning.

One of the factors that has allowed Canada to quickly rise up the global rankings for innovation is the immigration system.9 It provides various programs that allows for a comparatively frictionless move from student to the work force relative to other jurisdictions. This helps create a ready pool of high-quality talent for Canada’s technology ecosystem. As a result, up to 10% of Canada’s economic class permanent residents work in the technology sector - an industry that comprises only about 4% of total Canadian employment.10

Although Canadian cities are gaining ground, they face some challenges that are holding them back from achieving global acclaim.11 Historically, Canada’s strength has resided in the export of raw materials to the rest of the world. As a result, it has often lagged in its ability to commercialize its innovative end products. Despite an abundance of STEM talent, the Canadian tech industry still lacks experienced C-suite executives who are able to turn startups into global leaders. This absence of “big-enough” home grown companies with the expertise to foster and transform start-ups into globally competitive firms has left the Canadian STEM sector stuck in a “build and flip” cycle.12 Canadian start-ups tend to opt-out of the game through an acquisition by large global companies instead of organically growing to become global firms themselves. Lastly, the aversion to change in Canadian industry slows the pace of adoption and implementation of technology. Both government and private businesses delay incorporating new technology into their organizations, as decision makers are hesitant to bring on new technology due to the burden of additional-cost. However, new technology maintains the long-run competitiveness and productive capacity of the Canadian ecosystem.

Innovation beyond North America

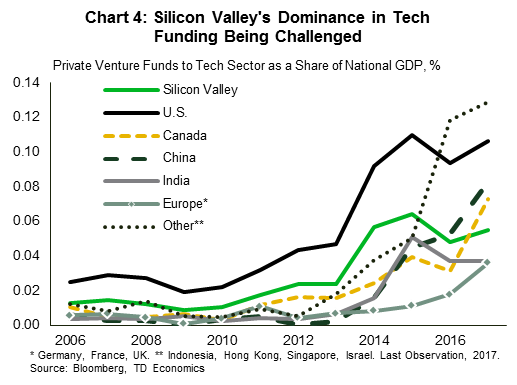

Other parts of the globe are succeeding in attracting a rising share of venture funds relative to the size of their economy (Chart 4). This is in part because foreign governments have been eager to attract private investment in innovation industries. As has often been the case historically, public expenditures have been focused on laying the groundwork necessary to build self-sustaining, innovation-friendly ecosystems. While the U.S. government has cut spending on basic research, a number of countries including China, Germany, and Canada have ramped up this type of spending. Furthermore, specialized ecosystems have popped up in other countries that can offer faster paths to commercialization.

Based on KPMG’s Global Technology Innovation Hubs report, Australia, India, Ireland, Japan, Korea, and Russia all rank at the high end of scale of nations that have been successful in cultivating domestic tech industries (Table 2). Australia’s tech industry excels at the Internet of things and quantum computing industries. The Japanese AI sector is buoyed by robotics, but is also notable in banking and transportation. Germany continues to be one of the global leaders in the automotive, software, and engineering sectors. The UK has a key role in Europe’s tech industry, despite the ongoing headwinds in its economy with Brexit negotiations. London’s connection to international cities, favorable time zone, multiculturalism, reputable universities, and well-rounded ecosystem has made the city a destination for tech companies and talent. India has managed to achieve early success in the digital revolution as it has stamped out its place as a global powerhouse for software development and information services.

In our view, the most important development occurring within the technology sector has been the broadening out of innovation hubs from developed markets in North America and Europe to those within the developing world. Once again, the main drivers of this move are domestic advantages over developed economies, namely low cost, access to large talent pools, and the ability for much more rapid commercialization of discoveries. Indeed, the appearance of Shenzhen and Bengaluru (formerly Bangalore) on lists of top global innovation hubs is not an anomaly. Both of these locales have experienced dramatic growth in the past few decades, with heavy support from all levels of government. Shenzhen is largely viewed as the world’s most critical hub for computer hardware manufacturing. Global communications giant Huawei has its headquarters there, with 25k of its 60k total workforce at its facility working in research and development.

Bengaluru is the home of India’s largest tech titans, Infosys and Wipro. Recently there has been a shift away from providing low cost services to a startup mentality as new waves of computer engineers have embraced a more entrepreneurial mindset. The interest is largely in blockchain, AI and machine learning technologies. Somewhat surprisingly, the tech scene in Bengaluru has advanced sufficiently that it’s now attracting Indian ex-pat entrepreneurs, investors, and workers.13

Although interest is building in the tech ecosystem in India and elsewhere, the biggest threat to Silicon Valley’s dominance is cities like Shenzhen in China. The speed at which China has been able to build up its own homegrown, whole tech ecosystems has caught many by surprise. Although U.S. firms have established a large global footprint, Chinese tech firms have rapidly achieved a lasting presence on a list of the world’s largest tech companies (Table 3). Well known Chinese firms, such as Ali Baba and Tencent, take the 6th and 7th spots respectively. What’s more, most of the Chinese firms on the list were non-existent 10 years ago, accenting the incredible feat of growth.

China’s rise

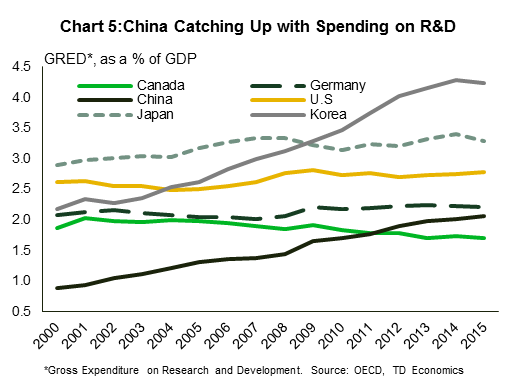

As with most things in China, this growth has not occurred by pure luck. The Chinese government has laid out plans to improve the longer term productive capacity of its economy, and has emphasized boosting R&D expenditures with the goal of eventually becoming leaders in high tech industries (Chart 5).

“Made in China 2025” (or MIC 2025 hereafter) was announced on May 2015 as a continuation to precedent industrial polices.14 The initiative aims to modernize the manufacturing process by ensuring that it’s innovation driven, while creating a competitive advantage for China by the end of 2025. The Chinese government will provide the financial tools, the support for creating manufacturing innovation centers (55 new centers by 2025), and a major role in strengthening and enforcing intellectual property rights.15 MIC 2025 focuses on applying AI and machine learning to modernize its manufacturing industry, and augment China’s information technology, aviation, rail, new energy vehicles, and agricultural industries. These industries constitute 40% of China’s industrial value-added manufacturing and are critical to maintain its competitiveness and growth in the 21st century. Ultimately, the goal is to change “Made in China” from being synonymous with low quality, mass produced products to be symbolic of high quality.

Although in the past the government has made an effort to ensure that markets helped drive resource allocation decisions across the economy, MIC 2025 reaffirms the role of the government in economic planning. The plan provides preferential access to capital for home-grown companies in order to promote their R&D capabilities. Subsidies are estimated to reach nearly U.S. $15 billion. Chinese banks also play an important role in MIC 2025, as they are encouraged to provide loans to spur development of indigenous brands as well as provide export credit insurance. In short, through MIC 2025, China seeks to gradually replace foreign technology with in-home technology and to prepare Chinese companies for international markets.16

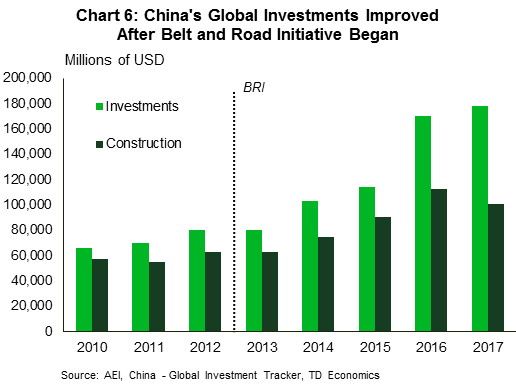

Complementing its MIC 2025 plans, China is also pushing forward with its Belt and Road initiative (BRI).17 BRI is worth nearly $4 trillion (Chart 6), and its main aim is to ease and improve trade with its neighbors and major trading partners.18 The infrastructure-focused initiative will build a network of railroads and shipping lanes with 70 countries across Central Asia, the Middle East and Europe. The “Belt” aims to recreate China’s ancient “Silk Road” in which merchants used to transport silk and other commodities. The “Road”, on the other hand, refers to the route that will connect participants of this agreement through oceans. It’s important to note that 89% of the Chinese funded projects as part of the belt and road initiatives are implemented by Chinese contractors.

China’s ascendancy in tech not guaranteed

Even though the ambitious government is putting in place the building blocks to become a dominant global force in tech, there are hurdles along the way:

- There remains a huge gap between the efficiency and the quality of production in Chinese goods. Closing the gap is not a feat that can be easily or quickly achieved. China is a state-controlled economy with very little space for markets to do their job in allocating resources efficiently. Moreover, excessive government intervention may hinder start-up growth due to the absence of good management, harder exit plans, and difficulty of attracting partners.

- Although China is aiming to open-up to the rest of the world to achieve its industrial goals, the tools used by its government continue to raise legal concerns. The Chinese government is likely to continue to run afoul of WTO rules and regulations due to its ongoing support for state owned enterprises, and distortions of the digital economy by restricting foreign investment and ownership.

- The sustainability of government funding is always in question. There are signs that it’s already slowing down compared to the funding provided during 2015/16. With authorities focused on rebalancing the economy and weaning off the addiction to credit-fueled investment, funding for the more ambitious aspects of the MIC 2025 and BRI may become scarcer in the years to come.

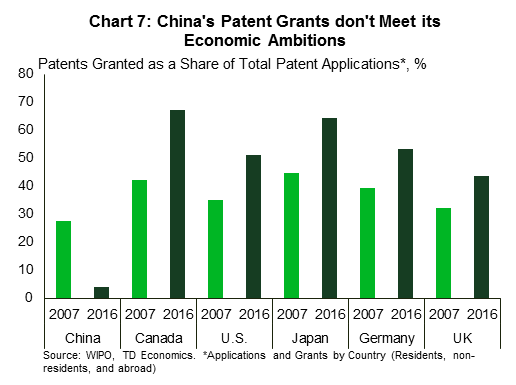

- Over the years China has built quite an unfortunate reputation amongst its trade partners, especially when it comes to intellectual property (IP) rights. According to the Commission on the Theft of American Properties, losses from intellectual property theft range from around $180 billion to $540 billion per year. China accounts for most of the reported IP theft, and has helped make it a target of tariffs by the U.S. administration (Chart 7). China’s inability to respect property rights has created shaky grounds between the ambitious communist economy and future trade partners who are now second-guessing entering trade agreements with China. In response, China has recently endeavoured to revisit its MIC 2025 plan, hoping to play down its bid to dominate manufacturing globally, and be more open to participation by foreign companies.19 If done right, they could ensure the success of their long-run innovation strategy if these changes manage to attract more foreign investment, and thereby act to accelerate China’s innovation drive.

Full economic benefits can only be realized once challenges overcome

The spread of innovation beyond traditional hubs such as Silicon Valley to newer locations, especially those in developing markets, is likely to provide a number of benefits to the global economy. Like trade in goods and services, more innovation usually results in greater social benefits. The discovery and implementation of productivity-enhancing technologies helps to boost an economy’s growth potential, in addition to improving the quality of life for the average citizen. However, also like trade, the gains may not be equally distributed. For example, rapid growth in China has widened the gap between the have and have-nots.

Both advanced and emerging market economies have a lot to gain from the movement of capital beyond Silicon Valley and to other jurisdictions. The economic benefits are almost certain. More spending on research and development means more jobs and more overall economic output. Over time, productivity enhancing technologies borne from these investments are likely to provide a strong counterweight against an aging population and associated slowdown in labor force growth. Moreover, artificial intelligence, biotechnology, and other technologies should also lead to dramatic but hard to measure improvements to our quality of life.

Technology transfers from advanced to emerging market economies are necessary to help the latter develop. But, there is also the potential for advanced economies to benefit from expanding research and development programs to emerging markets. They offer educated researchers sometimes at a cost advantage, allowing firms to expand research output without necessarily stretching their budgets. They may also be located closer to supply chains. For example, U.S. information and communications technology firms are finding it easier to undertake research and development in China given that most of the manufacturing facilities are located in Southeast Asia. This helps to shorten the time to commercialize new products.

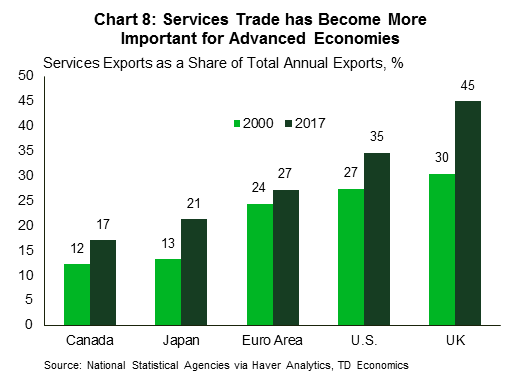

Trade agreements are facilitating the spread of intellectual property. The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) is an agreement that aims at improving intellectual property rights, and thereby helping expand services trade amongst signatory countries. This enables advanced economies to provide services that may be lacking in less developed economies, including legal, marketing, and branding. Services trade has become an increasingly important avenue for export growth in advanced economies (Chart 8).

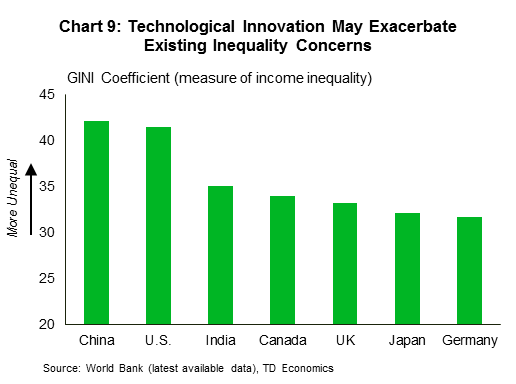

Along with growth opportunities come some challenges that will have to be overcome. The biggest challenge is devising strategies that ensure that the spread of innovation allows for fair distribution of gains and occurs in a manner that respects intellectual property rights. New technology leads to disruption in existing industries, including job losses, which may exacerbate existing income inequality (Chart 9). Therefore it’s critical that governments put in force policies that mitigate the negative impacts of the adoption of these new technologies.

China’s ascendance also provides a challenge to the current global order. The plan to accelerate their economic development and become a competitor in high value-added industries over the next decade has made it a target of the U.S. administration. The ideal outcome would be for a joint effort by the U.S. and its major trading partners to agree to exploit the innovative potential that China offers the world rather than hinder its progress. However, there will first have to be solid progress on China’s behalf to strengthen its intellectual property rights regime.

Bottom Line

Although Silicon Valley continues to be the top destination for tech talent and financing, innovation hubs in other U.S. cities and internationally are offering competitive alternatives. Investors are increasingly looking for the next big technological breakthrough, and Canada has a lot of potential given its talent pool and cost competitiveness. It is already home to a number of innovation ecosystems that excel in fintech, artificial intelligence, robotics, and manufacturing.

However, the bigger story is the rise of technology hubs in the developing world. Low cost, large talent pools, and the ability for shorter windows to the commercialization of new discoveries make cities in India, and China in particular, very attractive places for both domestic and foreign technology startups. The growth in China’s technology industry has been astounding and poses the greatest threat to unseating Silicon Valley from its throne as the global leader. However, China’s tech industry faces a number of challenges that are likely to hold future progress in check, most notably its lack of strong intellectual property laws, and failure to comply with WTO regulations.

The world has much to gain from this focus on innovation and its broadening out to new locales. New discoveries that enhance productivity and makes our lives better is viewed as unambiguously positive for future economic growth globally. But, the challenges posed by the associated labor market disruptions that typically accompanies technological progress suggests that policymakers have an important role to play in managing the process in order to reap the full benefits from new discoveries.

End Notes

- The Changing Landscape of Disruptive Technologies, KPMG, 2014-2018

- Global Tech Hubs Report, Global Metro Areas and Their Tech Companies, CB Insights: https://www.cbinsights.com/reports/CB-Insights_Global-Tech-Hubs.pdf

- Top Tech Cities in the World 2018, Focus by Expert Market: https://www.expertmarket.com/focus/research/top-tech-cities

- Silicon Valley Competitiveness and Innovation Project- 2018 Update: https://svcip.com/files/SVCIP_2018.pdf

- The Technology Sector in New York City, Office of the New York State Comptroller, September 2017: https://www.osc.state.ny.us/osdc/rpt4-2018.pdf

- Apple also announced plans to open new smaller U.S. campuses in Seattle, San Diego, and Culver City, while also expanding existing campuses in other cities including Pittsburgh, New York, and Boulder, Colorado. All told, Apple plans to hire an additional 20,000 employees by 2023. For further details see Apple’s Press Release, “Apple to build new campus in Austin and add jobs across the U.S.” from December 13, 2018. https://www.apple.com/newsroom/2018/12/apple-to-build-new-campus-in-austin-and-add-jobs-across-the-us/

- Silicon Valley Competitiveness and Innovation Project- 2018 Update: https://svcip.com/files/SVCIP_2018.pdf

- The Canadian AI Ecosystem: A 2018 Profile. Green Technology Asia Pte Ltd: https://mppga.ubc.ca/the-canadian-ai-ecosystem-a-2018-profile/

- Toronto Region Response to Amazon HQ2 RFP, October 19, 2017: https://s3.ca-central-1.amazonaws.com/torontoglobal/TorontoRegionResponsetoAmazonHQ2RFP_PD.pdf

- From Statistics Canada Census data.

- The Innovation and Competitiveness Imperative: Seizing Opportunities for Growth. Report of Canada’s Economic Strategy Tables: Digital Industries: https://www.ic.gc.ca/eic/site/098.nsf/vwapj/ISEDC_Digital_Industries.pdf/$file/ISEDC_Digital_Industries.pdf

- Ibid.

- Bengaluru: What’s Next for India’s Tech Capital, July 3, 2018: https://www.theguardian.com/business-to-business/2018/jul/03/bengaluru-whats-next-for-indias-tech-capital

- Made in China 2025, The Making of a High-Tech Super Power and Consequences for Industrial Countries, Mercator Institute for China Studies, December 2016 https://www.merics.org/sites/default/files/2017-09/MPOC_No.2_MadeinChina2025.pdf

- China to Invest Big in “Made in China 2025” Strategy, China Daily: http://www.chinadaily.com.cn/business/2017-10/12/content_33163772.htm

- Made in China 2025, The Making of a High-Tech Super Power and Consequences for Industrial Countries, Mercator Institute for China Studies, December 2016 https://www.merics.org/sites/default/files/2017-09/MPOC_No.2_MadeinChina2025.pdf

- How the Belt and Road Initiative Globalizes China’s National Security Policy, Mercator Institute for China Studies, November 15, 2016: https://www.merics.org/en/blog/how-belt-and-road-initiative-globalizes-chinas-national-security-policy

- After 15 Years in WTO, China Still Weak on Many IP Rights Rules, US Says, Intellectual Property Watch, October 1, 2017: http://www.ip-watch.org/2017/01/10/15-years-wto-china-still-weak-many-ip-rights-rules-us-says/

- China Prepares Policy to Increase Access for Foreign Companies, Wall St. Journal, December 12, 2018. https://www.wsj.com/articles/china-is-preparing-to-increase-access-for-foreign-companies-11544622331

Disclaimer

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Download

Share: